Charting Your Path: A Primer on CEO Careers in Private Equity, Venture Capital, and Startups

Oct 25, 2025

CEOs don’t need a “career primer.” You need decision rules. The choice among running a PE-backed company, partnering with a VC platform, or founding (again) is ultimately a capital-and-capability question: which platform best amplifies your operating system over the next three to five years, with a risk profile you can live with and a payout you can defend to your family and your board?

Below is a CEO-level guide—practical, not starry-eyed—on how each path actually works today, what investors will expect from you in the first 100 days, the evidence you must put on the table, and how to switch lanes without losing altitude.

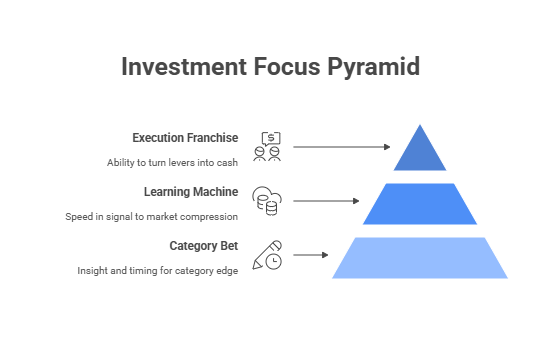

1) The CEO Lens: What Each Arena Really Buys From You

Private Equity (PE): an execution franchise.

PE sponsors buy your ability to turn controllable levers into durable EBITDA and cash. The winning pattern is simple, unfashionable, and hard to fake: price realization that sticks, cost-to-serve hygiene, inventory discipline, and a weekly cash rhythm that keeps covenants boring. The sponsor will back you on inorganic growth if, and only if, the base engine proves repeatable. PE pays for an operating system, not slogans.

Venture Capital (VC): a learning machine with speed.

VCs fund your ability to compress the distance from signal to product and from product to market. They expect auditable proof of learning (PMF evidence, retention curves, unit economics), not volume theater. The best boards behave like scientific advisors: they protect tempo, force prioritization, and stage capital against milestones. You’re paid for optionality you can convert into momentum, not for smooth forecasts.

Startups (Founder or Co-Founder): a category bet.

Founding again is a concentrated wager that your insight, network, and timing can create a category edge—often AI-enabled workflows in a real-economy niche. You control the culture and velocity, but you also own the downside. You win by building proof early and building trust faster than burn rises.

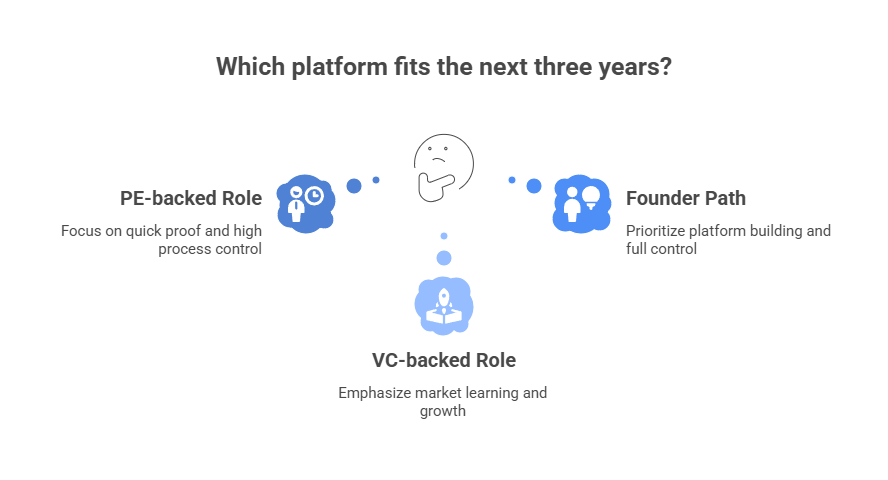

2) Decision Rules: Which Platform Fits Your Next Three Years?

Use these CEO-grade filters. If multiple ring true, choose the one where you can ship evidence soonest.

-

Time to Proof:

-

< 2 quarters: PE-backed operating role—pricing rules, CTS policies, cash discipline show up fast.

-

2–4 quarters: VC-backed growth role—PMF hardening, sales motion repeatability, agentic ops pilots.

-

> 4 quarters: Founder path—platform/product build before revenue quality is provable.

-

-

Control Surface:

-

High process control required: PE (board likes rules, not surprises).

-

High market learning required: VC (board tolerates pivots if learning velocity is real).

-

Full architecture control: Startup.

-

-

Liquidity Preference:

-

Equity with line of sight (3–5 years): PE (sweet spot with exit-back design).

-

Power-law optionality (7–10 years): VC equity and founder grants.

-

Founder economics: high variance; own the cap table, own the sleep loss.

-

-

Risk Ledger:

-

Macrorisk high, microlevers controllable → PE.

-

Tech/market risk high, burn moderate, TAM large → VC.

-

Category creation risk accepted → Startup.

-

3) What “Good” Looks Like in Your First 100 Days

If you take the PE-backed seat

-

Ship three artifacts by Day 30:

-

Price rulebook in CPQ (floors, bands, approvals, override expiry).

-

13-week cash tile reconciled weekly to bank, with variance reason codes.

-

CTS policy changes (MOQ, rush fee, returns hygiene) piloted in two segments.

-

-

Convert diligence into routines: a weekly performance room (value bridge → five deltas → decisions), a pricing council, and a lender-ready headroom view.

-

Evidence standard: before/after waterfalls, contribution by SKU family, dispute closure cycle time, inventory actions with cash effect. If a buyer couldn’t rerun your last month in 30 minutes, you don’t own it yet.

If you scale a VC-backed company

-

Cement PMF with auditable signals: cohort retention shape, payback by segment, win/loss learning loop.

-

Industrialize the go-to-market: one ICP, one repeatable motion, one price fence per segment; instrument usage → value → price.

-

Introduce agentic ops, gated: ticket routing, AR triage, fraud screens—only where accuracy and rollback are proven.

-

Evidence standard: versioned metrics, “how to rerun” notes, decision log per sprint; board packs that show what you stopped doing.

If you found (or re-found)

-

Reduce idea risk to execution risk: a dated sequence of falsifiable tests (must learn X by date Y or pivot/kill).

-

Buy down platform risk with modular choices (data layer, identity, billing) that won’t choke Series B diligence.

-

Build trust capital early: light data room with KPI lineage and scripts—even at $1M ARR it differentiates.

4) Working With Investors: Set Terms Around Operating Truth

-

Define the scoreboard up front. Align on five buyer-grade KPIs with lineage (price realization, contribution by family, OTIF/CTS, working-capital trio, forecast accuracy). Put the scripts in version control; archive monthly.

-

Write the exit at signing. Agree on the artifacts you’ll produce every month that a future buyer will require: CPQ exports, CTS outcomes, cash snapshots, access inventories, incident drills.

-

Codify exception lanes. For pricing, service credits, term deviations—every exception needs a reason code and an expiry. Investors will give you discretion if you show habit, not heroics.

5) Crossovers: How to Switch Lanes Without Losing Reputation

Public or founder CEO → PE-backed CEO

-

Translate narrative to rules: show how you’ll turn talk tracks into CPQ, retention into renewal mechanics, and dashboards into scripts.

-

Bring a “first five moves” pack: price, CTS, working capital, two-family inventory focus, and the cadence calendar. Sponsors hire certainty of process under pressure.

PE operator → VC GP/Operating Partner

-

Productize your playbooks. Convert pricing, cash, and integration routines into light frameworks a seed company can adopt. Your credibility is the velocity to PMF, not a 70-slide playbook.

-

Build a founder evaluation scorecard that predicts learning speed and quality of decisions under ambiguity.

VC-backed growth CEO → PE platform CEO

-

Reframe speed as reliability. Show how your growth tempo becomes weekly cash predictability, CTS control, and lender-grade telemetry.

-

Arrive with a bolt-on math method that is probability-weighted and cash-converted—and a PMO cadence sized for a mid-market team.

6) Capability Portfolio: What to Sharpen Now (Regardless of Path)

-

Pricing as production. Put rules in tools; coach to them; measure realization weekly.

-

Cash literacy. Make the 13-week tile your daily instrument panel; variance codes are a leadership language.

-

Cost-to-serve fluency. Allocate honestly, act surgically, and archive outcomes.

-

AI stewardship. Treat AI like electricity: useful, dangerous, audited. Gate agentic use cases with eligibility, evidence, guardrails, auditability, escalation.

-

Governance that travels. Document definitions, scripts, and decisions. When your story stands without you, multiples rise and timelines compress.

7) Conversations to Have With Your Board (Next Week)

-

Price power: “Open the CPQ export—what percent of quotes are within band, and what are the top three override reasons?”

-

Cash predictability: “Show last month’s forecast error and the variance codes closed within 24 hours.”

-

Service economics: “Which customer decile is unprofitable after CTS? What policy changed?”

-

AI risk & reward: “Which agentic decisions run at Level 2+? What’s the kill switch and who owns it?”

-

Exit-back evidence: “If a buyer arrived tomorrow, which binder would we hand them, and could they rerun a KPI in 30 minutes?”

8) Failure Patterns to Avoid (Seen Too Often)

-

Discount theater. Announcing list hikes without enforcement in CPQ; realization stalls, credibility fades.

-

Dashboard cosplay. Pretty charts with no lineage; boards nod, lenders don’t.

-

Pilot purgatory. Ten AI proofs of concept, zero decisions de-risked.

-

Integration vanity. Synergy numbers without probability, cash conversion, or TSA burn-down.

-

Archive amnesia. No immutable monthly binder; six months later the story can’t be replayed.

9) The CEO’s Edge

Your edge is not louder charisma or larger decks. It is the calm ability to show operating truth early, package it so others can verify it, and compound it with short, unglamorous routines. Choose the platform—PE, VC, or your own startup—that lets you practice that craft at full power for the next three years. Then publish the evidence, every month, so the market can price your discipline.

VCII Note and Copyright

TVC Next develops investor-operator talent by teaching the few levers that move EBITDA, cash, and multiple—and the evidence standard that convinces a buyer.

Copyright © 2025 VCII, Meritrium Corp. All rights reserved.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.