Headroom Is Strategy: Managing Lenders Before They Manage You

Oct 25, 2025

Most PE stories rise or fall on a quiet variable: confidence. Not customer confidence—lender confidence. In a high-rate cycle, your headroom is the oxygen for pricing moves, integration, and the inevitable bad week. Treat it as a system, not a quarterly slide. The firms that keep optionality long enough to win run a lender program with the same discipline they bring to customers and talent.

Make headroom visible—every day.

Operate from a single, one-tile 13-week cash view that reconciles weekly to the bank. Tie receipts to AR health (dispute codes, expected close dates), tie disbursements to an AP calendar aligned with covenants, and show borrowing-base hygiene alongside cash. When lenders ask, you don’t “explain” cash—you open the tile and walk the variances by reason code and owner.

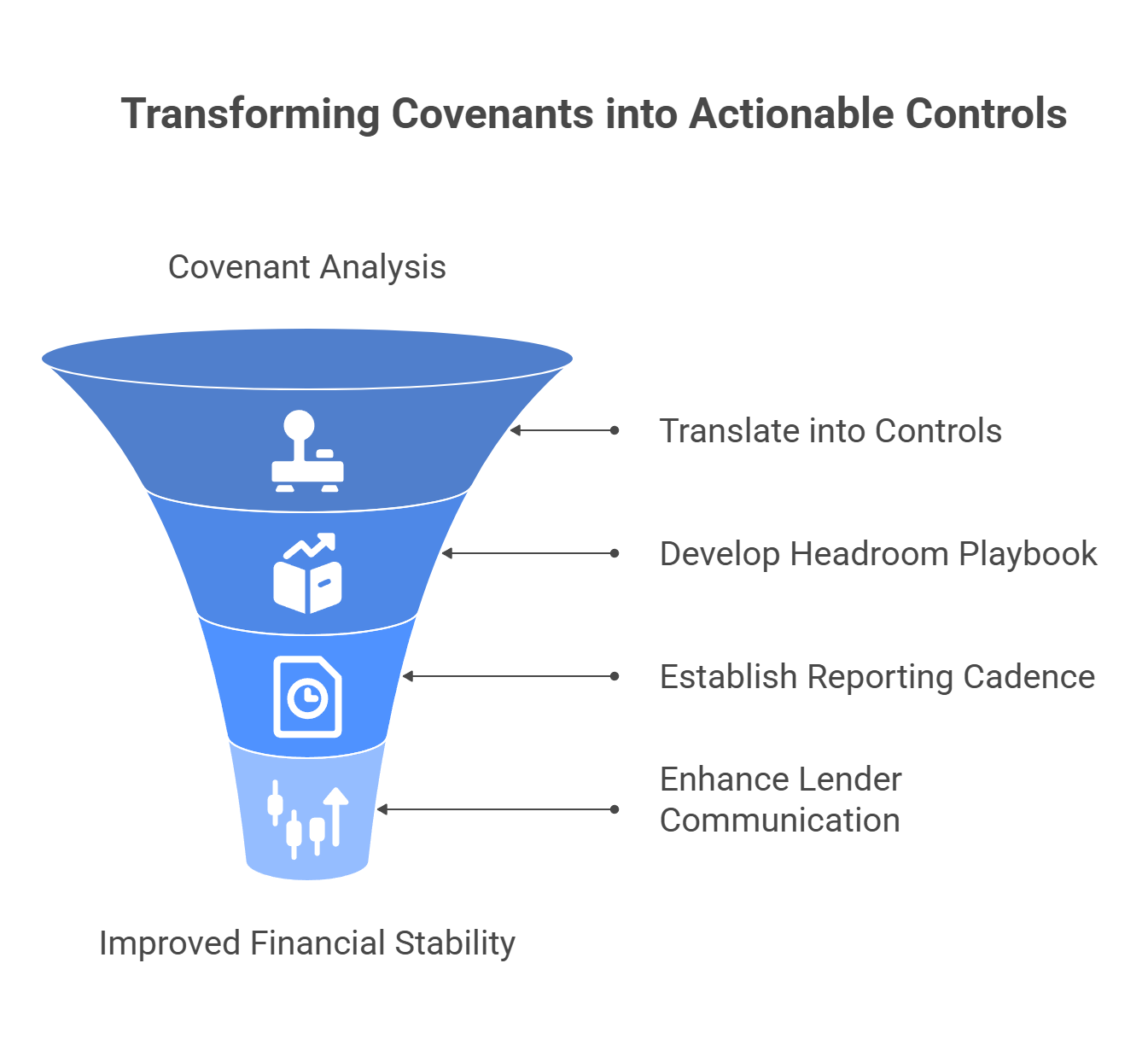

Map the covenants like operating limits, not legal text.

Translate each covenant into a living control: trigger levels, early-warning indicators, and the specific levers you’ll pull if a threshold is touched. Headroom is not a single number; it’s a playbook—pricing actions that lift margin without hurting volume, CTS policies that remove leakage, inventory levers that release cash, and term normalization that buys time without supplier drama.

Tell a lender story that writes itself.

Replace the “update call” with a cadence that publishes the same packet, on time, every time:

-

A value bridge that shows where EBITDA moved and why it will stick.

-

Working-capital bridge with disputes closed, AP batches staged, and inventory actions executed.

-

Headroom trend with “what changed” spelled out in one line per lever.

-

A short variance ledger: timing, volume, price, one-time, or error—closed or escalated.

When the packet is consistent and rerunnable, questions get shorter and spreads get kinder.

Run the borrowing base as a product.

Aging creep and documentation misses are not admin issues; they are cost of capital issues. Assign a single owner, instrument the exceptions (missing PODs, unsigned POs, stale reconciles), and resolve within 24–48 hours. Build a weekly “BB hygiene” tile: eligible AR, ineligibles by reason, advance-rate sensitivity. Lenders relax when eligibility and evidence are visibly under control.

Stage your asks before you need them.

Waivers and amendments go better when they are unsurprising. Keep a “drawer memo” up to date: covenant map, early-warning signals, lever sequencing, and the cash math under base, base-minus-20, and downside. Share the drift as soon as it appears and show the first lever already pulled. Lenders don’t need invincibility; they need to see you move before they ask.

Protect revenue lanes while you buy time.

Headroom-saving moves that spook customers are false economies. Use price bands in CPQ (with overrides that expire), harmonize service promises per segment, and retire long-tail complexity that drives rework. Communicate proactively with top decile accounts if payment terms change; pair the change with a service benefit or a clear rationale. Cash control that preserves revenue is the only sustainable kind.

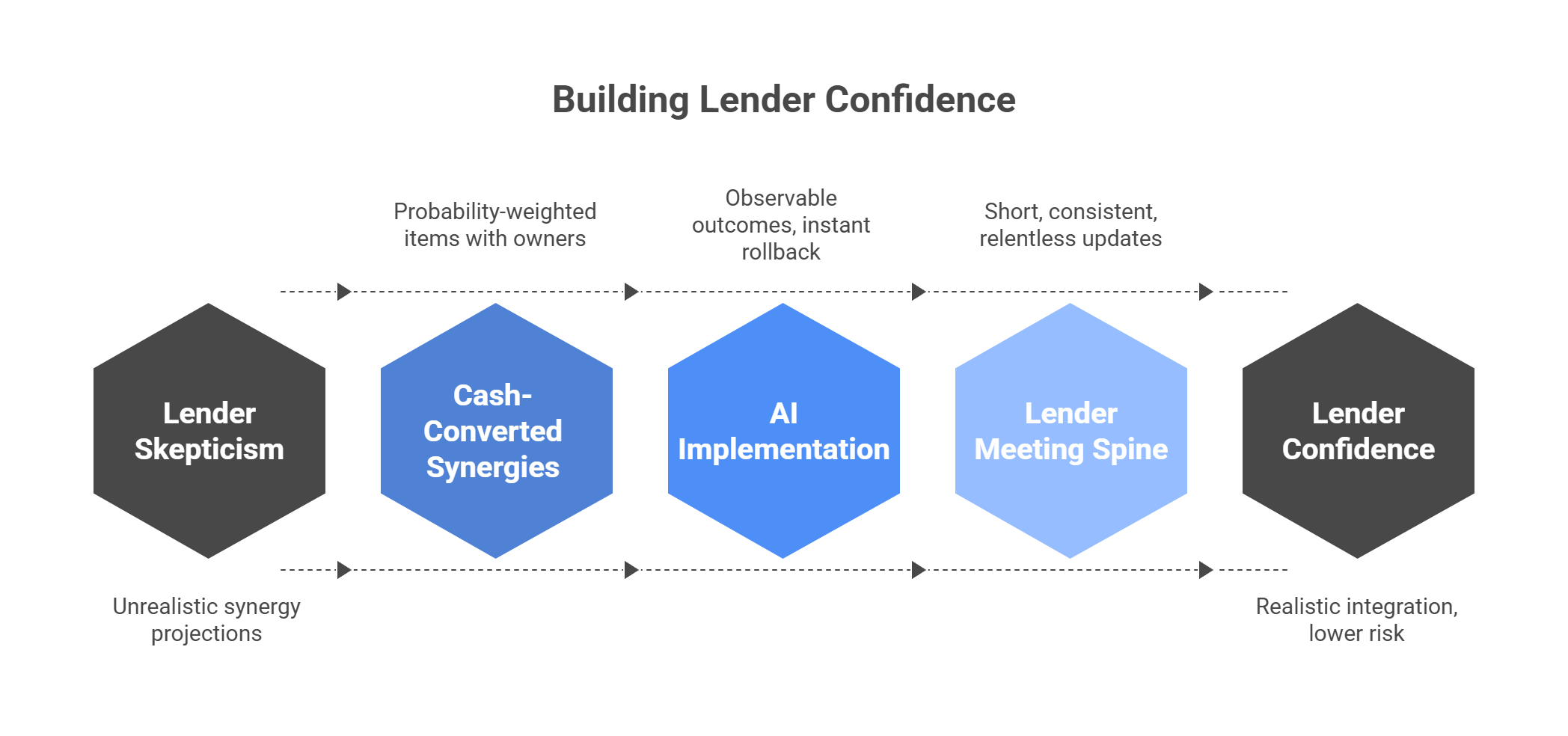

Instrument integration and synergy the lender way.

Don’t present “run-rate” synergies; present cash-converted, probability-weighted items with owners, ramps, and TSA burn-off. Tie each item to headroom impact and covenant sensitivity. Lenders price the realism of your integration rhythm more than the size of your deck.

Make AI lower risk, not raise eyebrows.

Use agentic tools only where outcomes are observable and rollback is instant: dispute triage, ticket routing, contract extraction. Gate with eligibility, evidence, guardrails, auditability, and escalation. Show your lender the audit trail and the kill switch. “We automated collections” is noise; “we cut dispute cycle time by 9 days with a logged, reversible agent” is credit.

The lender meeting spine (short, same, relentless).

-

Monthly packet (sent before the call): bridge, WC, headroom, variance ledger, borrowing-base hygiene.

-

Call (30 minutes): walk the packet; highlight decisions taken and the next lever in sequence.

-

Quarterly “rerun”: pick one KPI (e.g., price realization or DSO) and reproduce it live from stored scripts to ledger; review access inventories and incident drills in 10 minutes.

Signals you’re winning.

Conversations shift from “what’s true?” to “what sequence?”; documentation requests fall; amendment talks turn into structure, not trust; pricing and covenants improve on renewal because your cadence has become a credit feature, not a promise.

Antipatterns that quietly raise your cost of capital.

List hikes without pocket control. “Pro forma” synergies that don’t convert to cash. A 13-week model that doesn’t tie to bank balances. Borrowing-base defects treated as clerical. AI pilots that touch customer cash with no audit trail. Quarterly heroics in place of weekly hygiene.

What changes on Monday.

Publish the headroom tile. Lock the AP calendar to cash cadence. Enforce CPQ bands and override expiry. Start the weekly dispute blitz and two-family inventory focus. Archive a monthly packet to immutable storage with scripts and “as-of” stamps. When lenders can rerun your math in 30 minutes, optionality returns—and strategy breathes again.

VCII Note and Copyright

TVC Next installs headroom as an operating system—cash visibility, covenant triggers, lever sequencing, and lender-grade evidence—so CEOs keep options open while compounding value.

Copyright © 2025 VCII, Meritrium Corp. All rights reserved.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.