Private Equity's Zombie Challenge: Breaking the Exit Freeze Before It Breaks the Model

Jan 12, 2026

Private equity is increasingly burdened by “living-dead” assets: portfolio companies and aging funds that consume capital and attention without delivering growth, liquidity, or meaningful returns. The problem isn’t capital scarcity—it’s a growing inability to exit. In a tightening macro environment, this has exposed a critical fault line in the PE operating model: the reliance on liquidity assumptions that no longer hold.

I. The Zombie Phenomenon: Alive on Paper, Dead on Performance

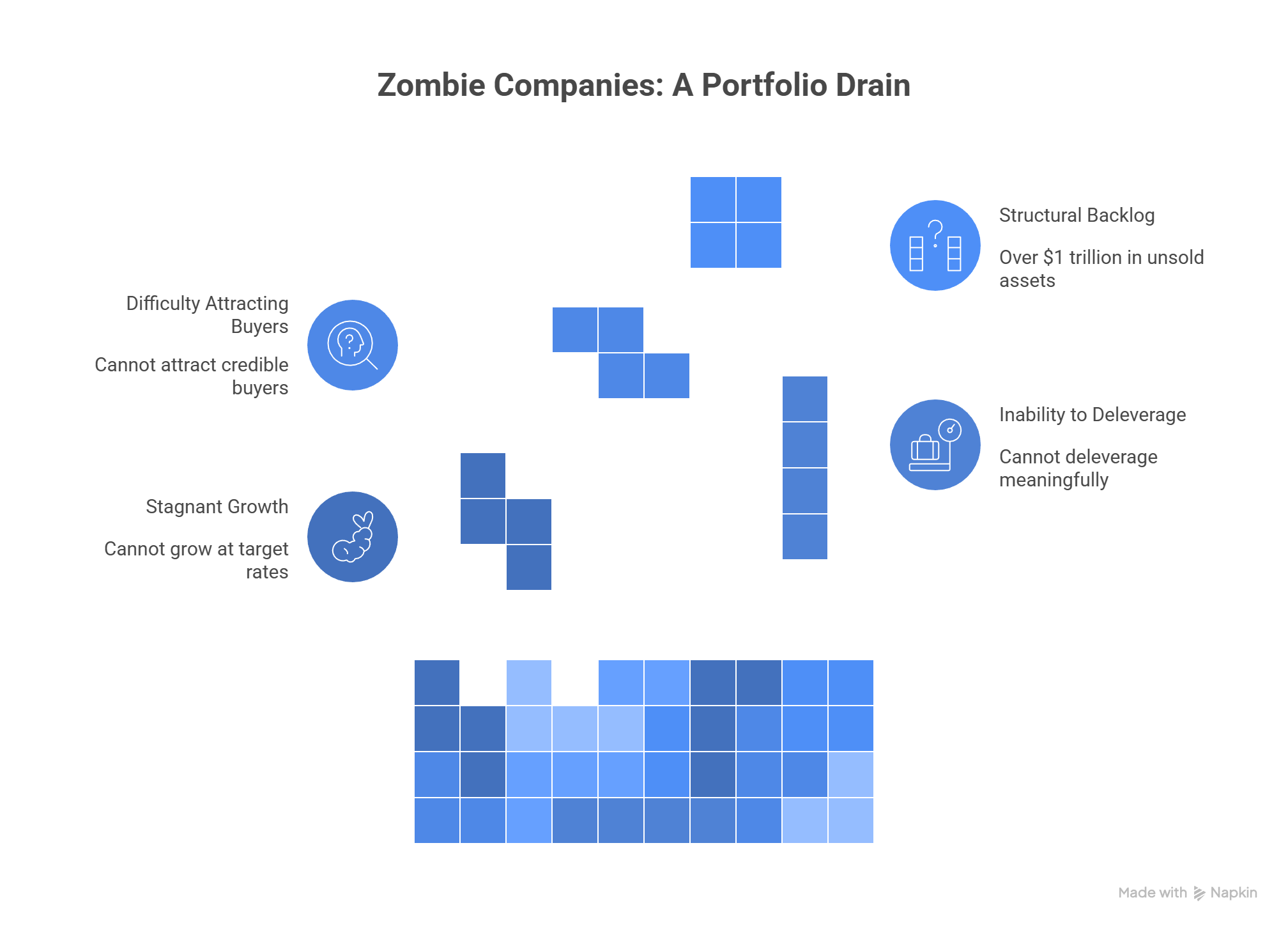

A zombie company, in the private equity context, is not bankrupt. It services debt, covers expenses, and keeps operating. But it cannot:

-

Grow at target rates

-

Deleverage meaningfully

-

Attract credible buyers at acceptable valuations

These companies linger in portfolios well beyond underwriting expectations, tying up GP bandwidth and LP capital while contributing little to fund-level performance.

By mid-2025, industry estimates suggested over $1 trillion in assets remained unsold in PE portfolios—assets that, under normal M&A cycles, would have exited and returned capital to investors. This has created a structural backlog.

II. How the Industry Got Stuck: Six Root Causes

The current zombie dynamic is not accidental. It is the compound result of six structural shifts:

| Structural Force | Effect on Exit Activity |

|---|---|

| Higher Interest Rates | Reduce buyer appetite for leveraged deals |

| Tighter Credit Markets | Limit refinancing and suppress valuations |

| Selective M&A / IPO Markets | Shrink viable exit windows |

| Valuation Anchoring | GPs avoid crystallizing losses vs 2021 prices |

| Complex Capital Structures | Increase cost of formal restructurings |

| Incentive Misalignment | Pressure to delay markdowns to protect IRRs |

The net result: Exit volumes fall, holding periods stretch, and portfolios age in place.

III. From Zombie Companies to Zombie Funds

Zombie dynamics don’t stop at the asset level. They extend to fund structures themselves.

-

Zombie funds are aged vehicles that report significant NAV but distribute little capital.

-

These funds linger beyond 12–15 years, well past intended maturity.

-

According to industry surveys, more than 40% of LPs now report exposure to at least one zombie fund.

This is a silent liquidity crisis: capital is technically “active” but functionally trapped.

IV. Why Dry Powder Isn’t the Solution

Despite headlines touting record levels of dry powder—over $2.6 trillion globally—this unspent capital is not offsetting the exit drought.

| Metric | Trend |

|---|---|

| Fundraising volumes | Declining YOY |

| Distributions to LPs | Down 30–50% from peak |

| Average hold periods | Now >5.6 years |

| IRR compression | Common for deals held >6 years |

Dry powder is only as useful as the ability to deploy and recycle. But when realizations lag, deployment stalls, and LPs hesitate to re-up.

This creates a self-reinforcing loop:

Weak exits → fewer distributions → tougher fundraising → extended holds → more zombie assets

V. Breaking the Cycle: What Leading GPs Are Doing

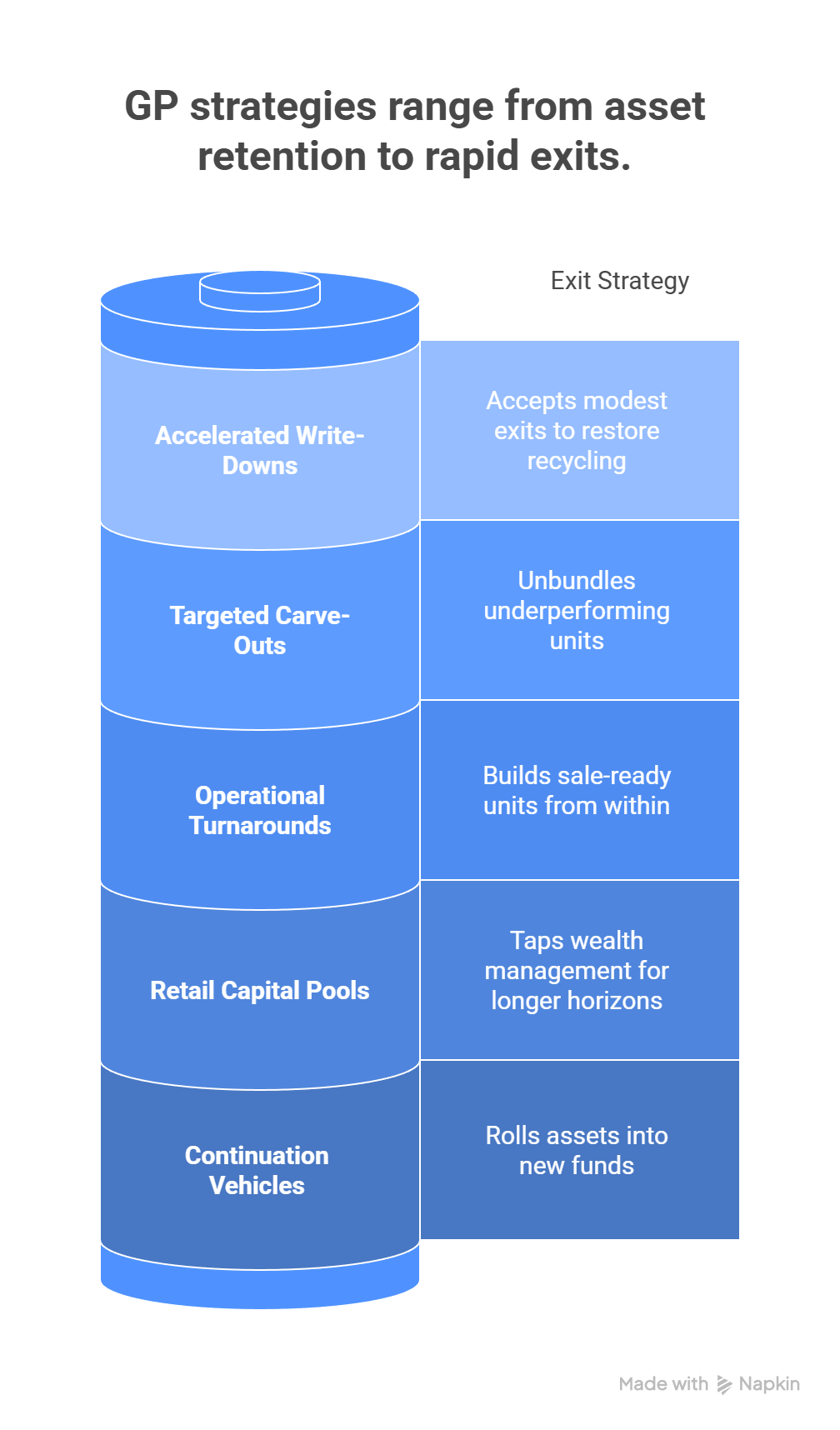

Forward-thinking managers are adapting. The most resilient are pursuing five distinct strategies:

1. Continuation Vehicles

-

Roll high-conviction assets into new funds

-

Give LPs the option to cash out or roll over

-

Now represent up to 25% of secondary volume

2. Retail and Semi-Liquid Capital Pools

-

Tap wealth management channels

-

Offer longer horizons in exchange for access

-

Smooth fundraising but don’t solve exits alone

3. Operational Turnarounds Over Financial Engineering

-

Emphasis on cost takeout, pricing, digitization

-

Less reliance on leverage or arbitrage

-

Build “sale-ready” units from within platforms

4. Targeted Carve-Outs and Separations

-

Unbundle underperforming units from healthy cores

-

Make assets more digestible to strategic buyers

5. Accelerated Write-Downs with Redeployment Focus

-

Accept modest exits to restore recycling

-

Reset incentives to reward resolution over delay

VI. The Real Mandate: Exit Readiness as a Core Capability

The past decade allowed private equity to depend on financial tailwinds—abundant leverage, expanding multiples, and liquid exit markets.

That era is over.

Now, performance must be earned through execution. The GPs who thrive in this new environment will be those who:

-

Re-underwrite aging assets with surgical discipline

-

Invest in operational improvements that rebuild exit narratives

-

Design structures that unlock—not delay—liquidity

-

Treat exit management as a core capability, not a secondary event

VCII Bottom Line

Zombie companies and funds are not just drag on returns. They are a systemic signal: the PE model must shift from passive asset holding to active, engineered value realization.

This requires more than optimism and dry powder. It demands:

-

Faster decision cycles

-

Sharper operational playbooks

-

Transparent communication with LPs

-

Willingness to accept shorter holds with modest outcomes

Because in this environment, “good exits today” often beat “perfect exits tomorrow that never come.”

VCII 2025 Copyrighted Material.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.