The CVC Reckoning: Munich Re Ventures’ Shutdown Exposes the Structural Fragility of Corporate Innovation

Nov 06, 2025

Corporate Venture Capital (CVC) has long been positioned as the strategic bridge between enterprise maturity and startup dynamism. When designed well, it identifies emerging technologies, accelerates capability-building, and shapes the future trajectory of incumbents. Yet the sudden wind‑down of Munich Re Ventures (MRV) as a $1.2 billion unit widely regarded as a benchmark for strategic venture excellence; this demonstrates how vulnerable CVC remains to internal governance cycles, regardless of performance.

This was not a failure of investment performance, strategic relevance, or portfolio construction. It was a failure of organizational design.

As Global Corporate Venturing noted, “If Munich Re Ventures can be shut down, then no CVC is structurally safe.” The message to the market is unambiguous: Without governance durability, even the most strategically aligned CVC units can be erased by leadership turnover.

A High‑Performing CVC Unit Dismantled at its Peak

Founded in 2015 under Managing Partner Jacqueline LeSage, MRV deployed approximately $1.2 billion across nearly 100 investments. Its portfolio included:

-

Next Insurance, acquired by Munich Re for $2.6 billion

-

Hippo, reshaping digital reinsurance models

-

Augury, a leader in AI‑driven industrial machine health

MRV was recognized not only for financial performance, but for sophisticated operational practices: portfolio development teams dedicated to integration, structured strategic value frameworks, and disciplined secondary market usage. These are capabilities many CVCs aspire to but rarely execute.

Despite this, the unit was formally wound down in late 2025, with remaining assets transferred to MEAG (Munich Re’s asset management arm) and only a small continuity team retained.

This decision did not stem from distressed financials. Munich Re posted a record €2.1B quarterly profit in 2025 and is on track toward €6B annualized earnings. Instead, the catalyst was changes in board leadership and strategic orientation—highlighting the misalignment of time horizons between venture investing and corporate governance.

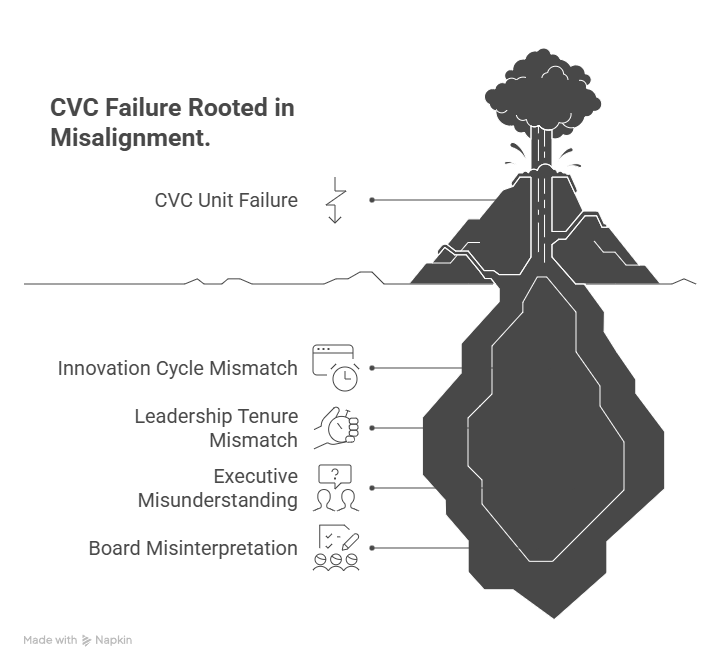

A Systemic Structural Misalignment

CVC operates on 7–12 year innovation cycles. Corporate leadership operates on 3–5 year strategic and tenure cycles.

This mismatch is the structural fault line.

Research by Stanford’s Ilya Strebulaev shows that more than 60% of executives insufficiently understand VC norms, particularly regarding failure tolerance, portfolio logic, and illiquidity. As a result, corporate boards frequently misinterpret:

-

Write‑offs as evidence of model failure

-

Strategic optionality as unquantifiable value

-

Time‑phased returns as inefficiency

GCV data suggests 40% of CVC units do not survive past their third year, regardless of return performance. The Munich Re case fits this pattern: a governance shift reclassifies strategic experimentation as expendable overhead.

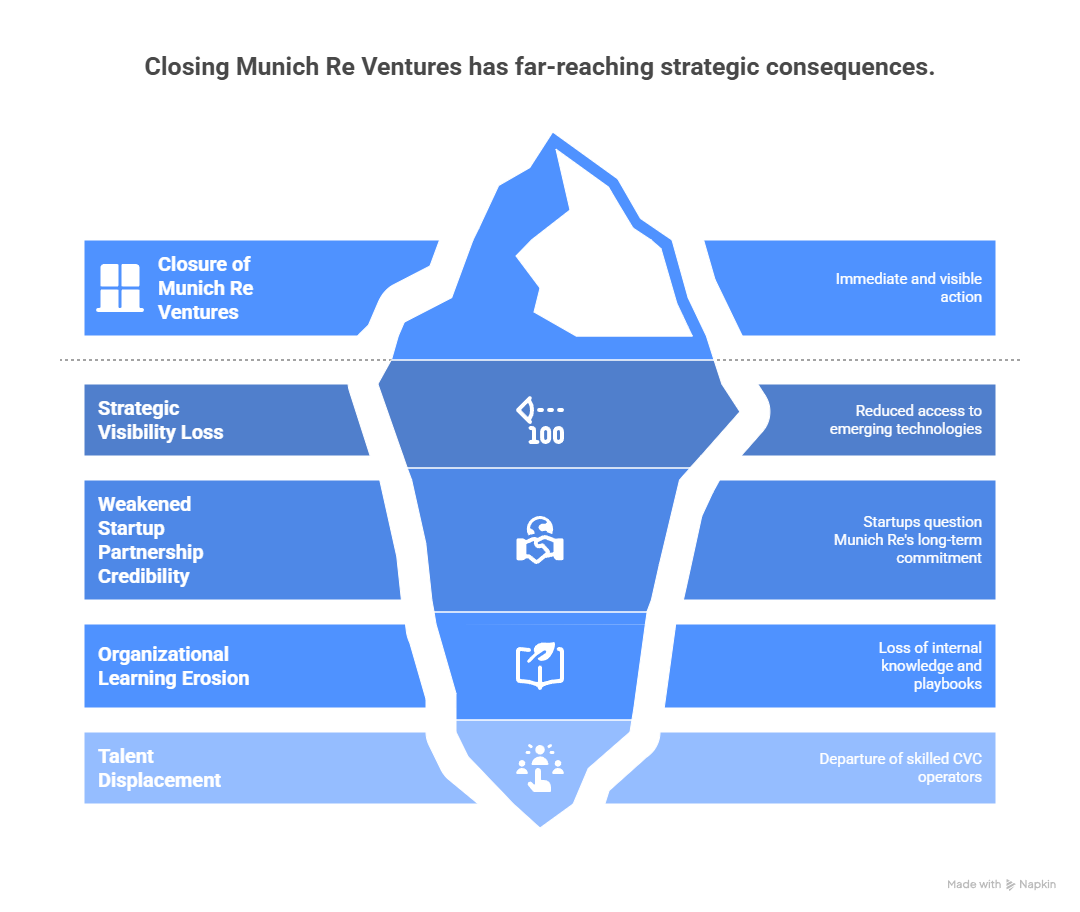

Strategic Consequences Extend Beyond One Closure

-

Strategic Visibility Loss

CVC provides early access to emerging technologies shaping insurance, underwriting automation, and digital distribution. Eliminating MRV narrows Munich Re’s external sensing capability. -

Weakened Startup Partnership Credibility

Founders and co‑investors now evaluate corporate LPs for durability risk. A CVC with unclear longevity becomes a strategic liability in competitive deals. -

Organizational Learning Erosion

MRV developed internal playbooks for integration, partnership evaluation, and pilot program governance. Without continuity mechanisms, this knowledge dissipates. -

Talent Displacement

CVC operators rarely transition effectively into core business functions. The likely outcome is a talent exodus, diminishing Munich Re’s future innovation capacity.

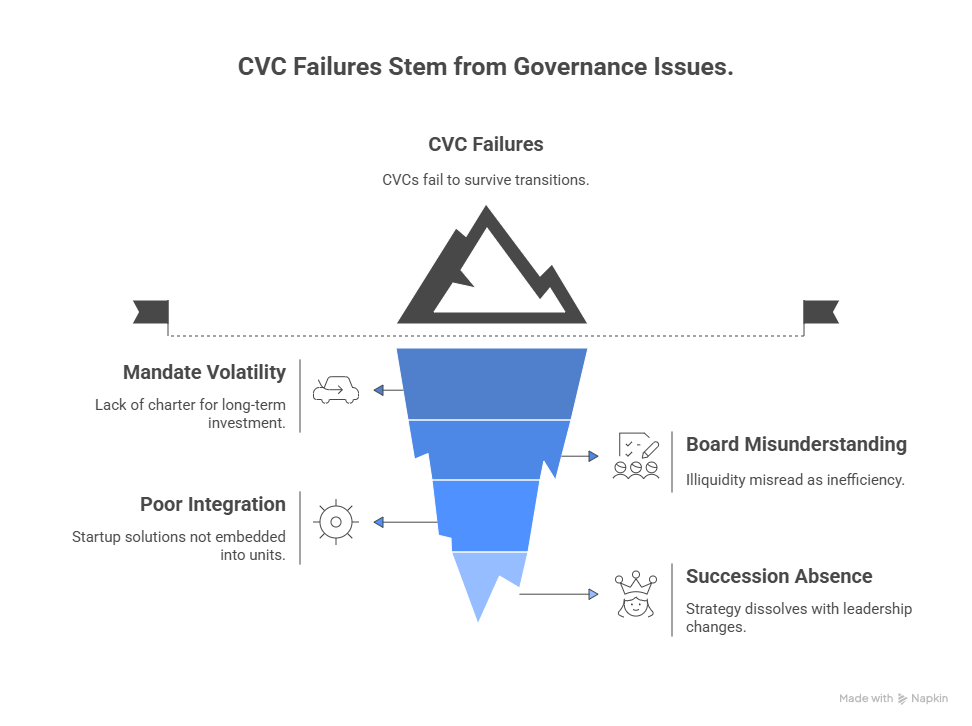

Why Most CVC Models Remain Fragile

VCII’s review of active and shuttered CVC units identifies four root-cause structural weaknesses:

| Failure Mode | Structural Cause |

|---|---|

| Mandate Volatility | No charter protecting long‑horizon investment logic |

| Board Misunderstanding | Venture illiquidity misread as inefficiency |

| Poor Integration Pathways | Startup solutions rarely embedded into P&L units |

| Absence of Succession Safeguards | Strategy dissolved when leadership changes |

CVC fails not because it does not work, but because it is rarely architected to survive governance transitions.

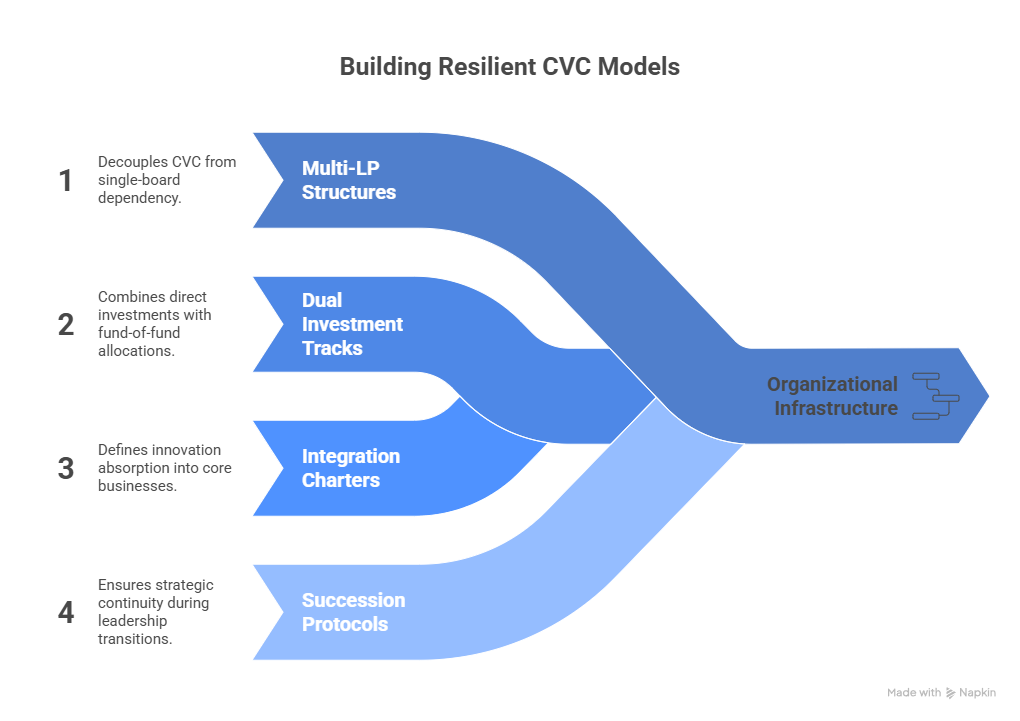

Designing CVC Models That Endure

Resilient models increasingly follow hybrid governance architectures, including:

-

Multi‑LP structures to decouple CVC from single‑board dependency

-

Dual investment tracks: direct startup investments plus fund‑of‑fund allocations

-

Integration charters defining how innovation is absorbed into core businesses

-

Succession protocols to maintain strategic continuity during leadership turnover

These models treat CVC not as a discretionary innovation program, but as organizational infrastructure.

VCII Insight

Munich Re Ventures was not shut down because it lacked capability. It was shut down because it lacked governance insulation.

That is the central lesson:

CVC must be architected to outlive the executive who launches it.

The question facing every board is no longer whether to invest in venture ecosystems, but whether their organizational structure can sustain the time horizon required for impact.

References (Non‑Social Media Sources)

-

Global Corporate Venturing (2025). “Munich Re winds down $1.2bn VC arm after decade of investing.”

-

McKinsey & Company (2024). Global Private Markets Review.

-

PwC (2025). AI Adoption and Value Creation in Portfolio Operations.

-

Strebulaev, I. (Stanford GSB). Corporate Venture Capital Strategy and Performance Studies.

-

Next Insurance Acquisition Data: Munich Re Annual Report (2025).

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.