The Synthetic US Sovereign Wealth Fund: Why America’s Decentralized System Works at Global Scale

Sep 17, 2025

The United States does not run a single, national sovereign wealth fund. It does something stranger and, in practice, bigger. Through public pensions, the federal Thrift Savings Plan, university endowments, private foundations, state permanent funds, and the vast 401(k) and IRA system, America has assembled a decentralized, multi-cellular “synthetic SWF” that rivals any sovereign pool on earth. This organism works because of deep fiduciary rules, brutal market transparency, giant and liquid capital markets, intense competition among managers, and a culture of experimentation that rewards evidence over theater.

What makes it “synthetic” and why it matters

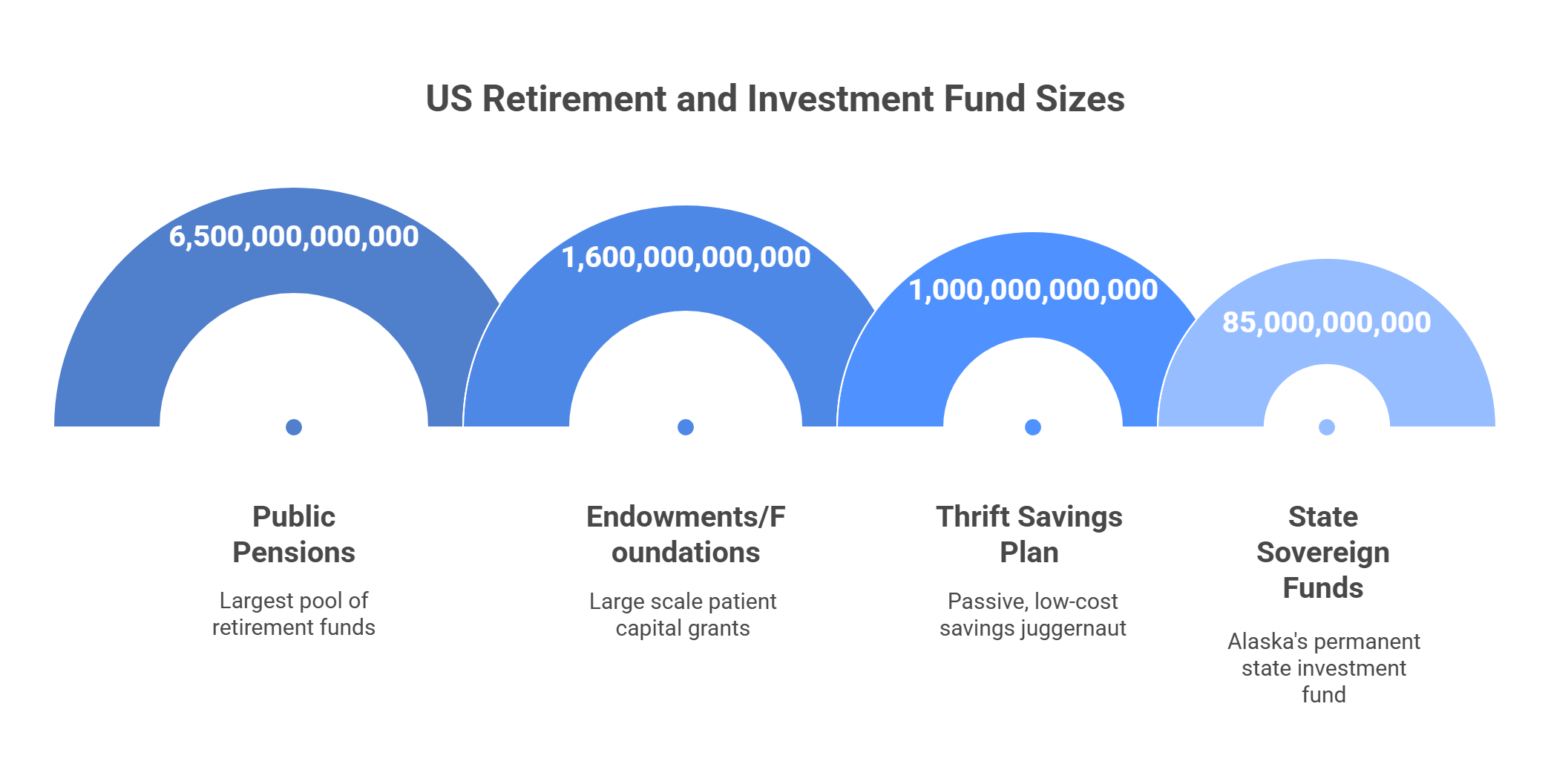

The US retirement complex alone held about 43.4 trillion dollars in Q1 2025, including 8.7 trillion in 401(k)s and 16.8 trillion in IRAs. The federal Thrift Savings Plan crossed the 1 trillion mark in mid-2025. Public pensions at the state and local level add roughly 6.0 to 6.5 trillion more in assets. University endowments contribute another ~839 billion, while private foundations stand near 1.64 trillion. Add state-level permanent funds like Alaska’s and Texas’s, and you get a distributed super-investor that deploys capital across every asset class and every style horizon.

Two structural advantages make this machine hum:

-

The world’s deepest markets to absorb it. US equities hover around 63 trillion in market value, while US fixed income outstanding sits near 48 trillion. That depth lets the synthetic SWF take risk, hedge risk, and rotate risk without breaking the plumbing.

-

Fiduciary architecture that forces discipline. ERISA’s prudence and loyalty standards, backed by the Department of Labor, created a culture where decision makers must prove they acted solely for beneficiaries, with evidence. That has compounded for five decades into processes, committees, consultants, OCIOs, and audit trails that prefer measurable results over glossy promises.

Why a decentralized model actually works

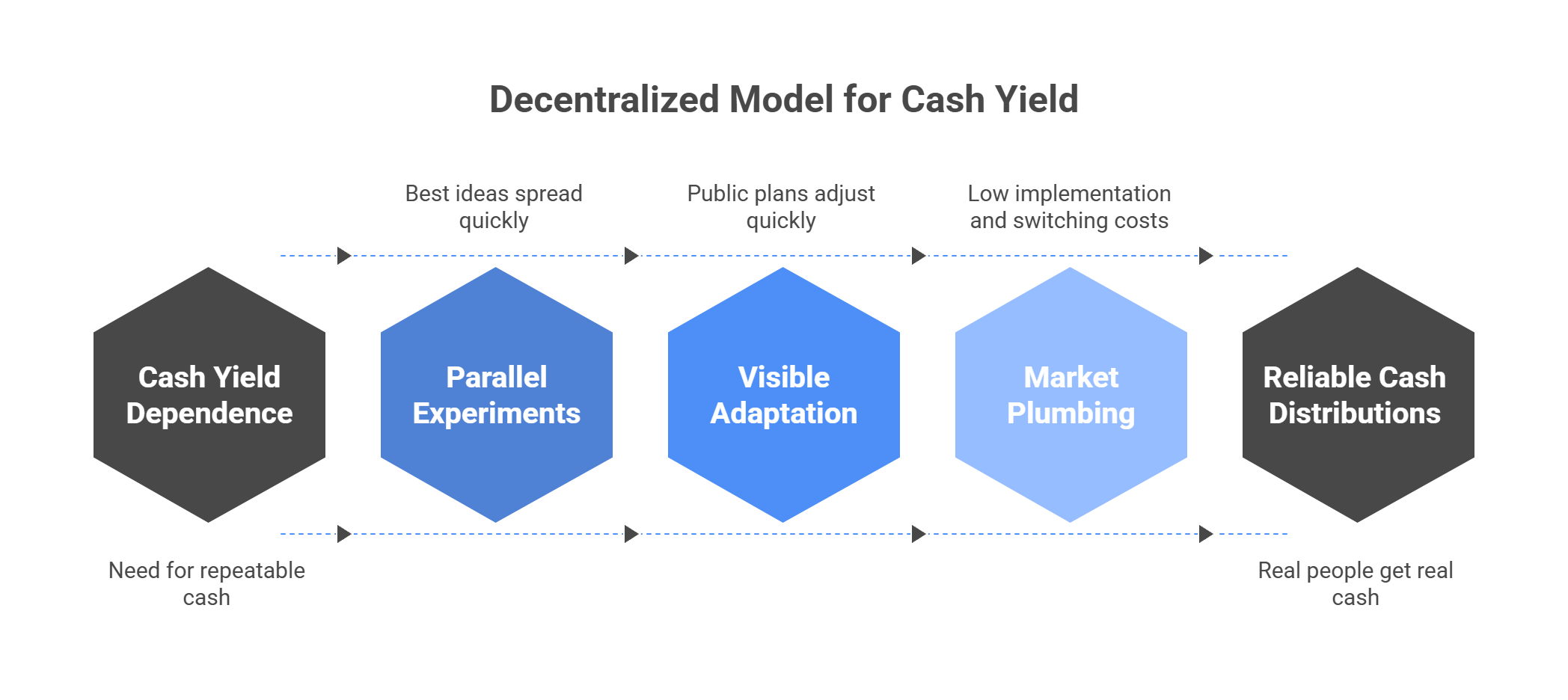

Many balance sheets, one incentive: pay real people real cash

Teachers, firefighters, nurses, federal workers, union members, university students, and grantees all depend on distributions. That relentless need for cash yield and repeatability pushes US asset owners to favor managers who can turn pro-forma into DPI, not just TVPI. It also explains why secondary markets, NAV financing, and pacing models matured quickly here: they serve a payments clock, not a press release.

Competitive federalism in finance

Because there is no single master fund, the ecosystem runs parallel experiments. The Yale endowment popularized long-horizon allocations to alternatives; others adapted or pushed back. The best ideas spread, the worst quietly die, and the scoreboard is public.

Evidence beats theater

Endowments and pensions publish performance, funding ratios, and assumptions. State treasurers, controllers, boards and LPACs ask tough questions. When markets froze and exit windows narrowed, public plans still posted funding gains or adjusted pace and mix in private credit or green infra. The point is not perfection. The point is visible adaptation.

Industrial-grade market plumbing

A national SWF needs pipelines. The US instead built exchanges, clearinghouses, custody networks, ETF and mutual fund rails, credit markets, and secondaries big enough for institutional elephants to move without flooding the room. That keeps implementation costs down and switching costs tolerable.

The building blocks of the synthetic SWF

-

Public pensions: ~6.0 to 6.5 trillion across thousands of plans, with annual benefits over 400 billion flowing to retirees. Governance varies, but funding visibility and reporting are robust and improving.

-

Defined contribution plus IRAs: The center of gravity. 401(k), 403(b), 457 and IRA assets dominate the long-term pool, with mutual funds and target-date funds as default engines.

-

Thrift Savings Plan: A passive, low-cost juggernaut at ~1 trillion, proving scale can live with simplicity.

-

Endowments and foundations: Risk labs for illiquids and mission-driven capital. Endowments refined the long-horizon model. Foundations supply patient, counter-cyclical grants and program-related investments at 1.6 trillion scale.

-

State-level sovereign funds: Alaska Permanent Fund (~85 billion preliminary mid-2025), Texas Permanent School Fund (~62.4 billion market value March 2025), New Mexico’s constellation of permanent funds (~64 billion total AUM June 2025), North Dakota’s Legacy Fund (~13 billion). These are true SWFs, but within a federal mosaic, not a federal ministry.

Why it often beats a single national SWF

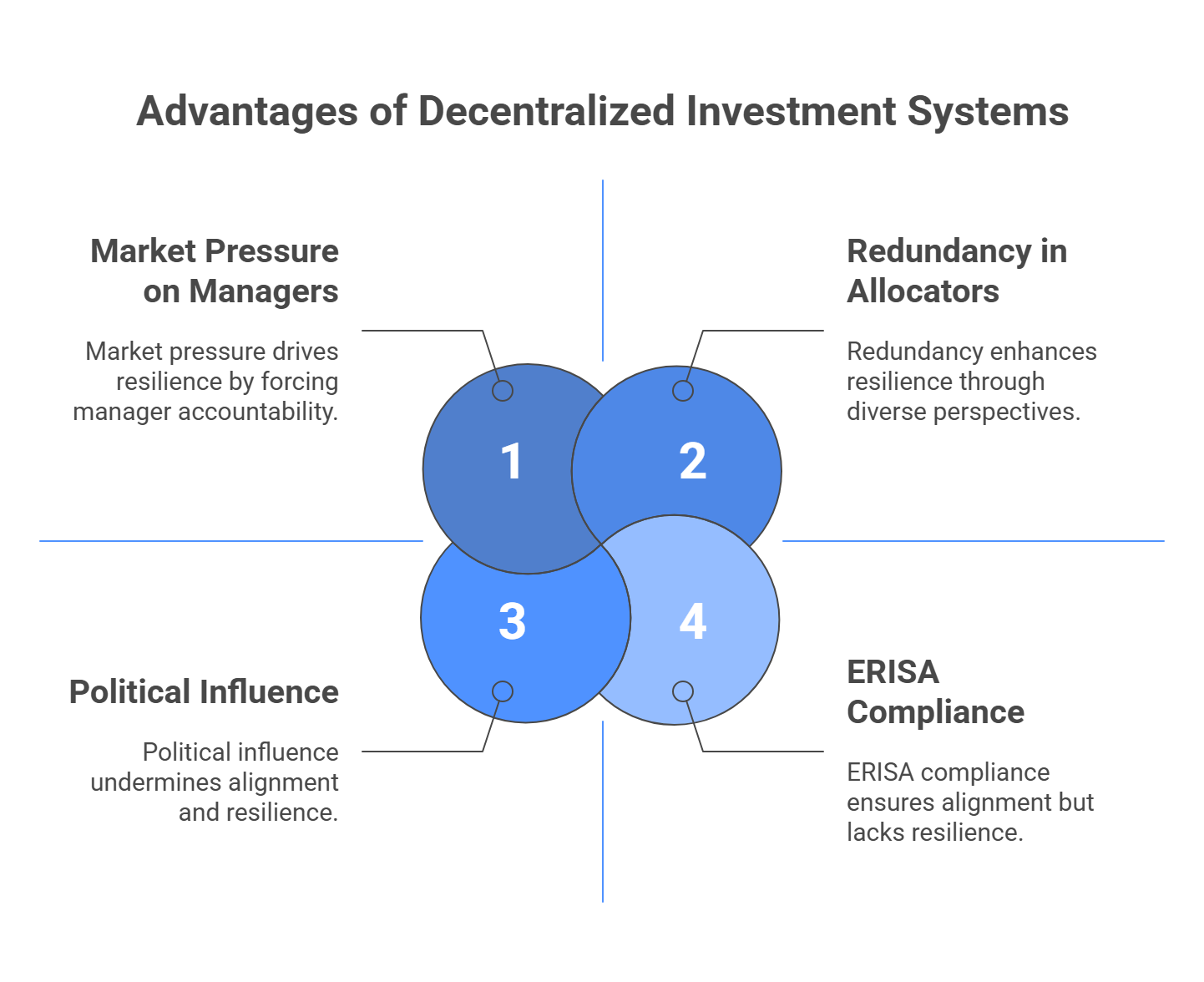

1) Alignment through law, not politics. ERISA’s prudent expert standard plus state fiduciary rules keep investment committees focused on beneficiaries, not ministers. That constrains style drift, encourages documentation, and resists headline chasing.

2) Redundancy as a feature. Many allocators looking at the same problem from different mandates create resilience. Some will be early, some late, some wrong, some right. The system learns faster than any single office can.

3) Market pressure and easy exits. Managers who underperform lose mandates, and they lose them in a market that offers substitutes. Competition is a governance technology.

4) Time-horizon layering. DC plans need daily liquidity. Pensions can take multi-year illiquidity. Endowments take decades. Foundations smooth grants. Add them up and you get a full yield curve of patient capital.

Where it underperforms a national SWF

-

Fragmentation tax. Overlapping consultants, duplicative systems, and uneven data quality create waste. Not every board is world-class. Not every plan has scale.

-

Herding and pro-cyclicality. Benchmark pressure can pull capital into the same trades at the same time. When exits slow, allocator pacing can snowball.

-

Policy whiplash. State-level politics can tug portfolios in opposing directions, as seen in headline clashes around ESG and manager selection. Reuters

These are solvable with better shared data, clearer decision rights, and evidence-first reporting.

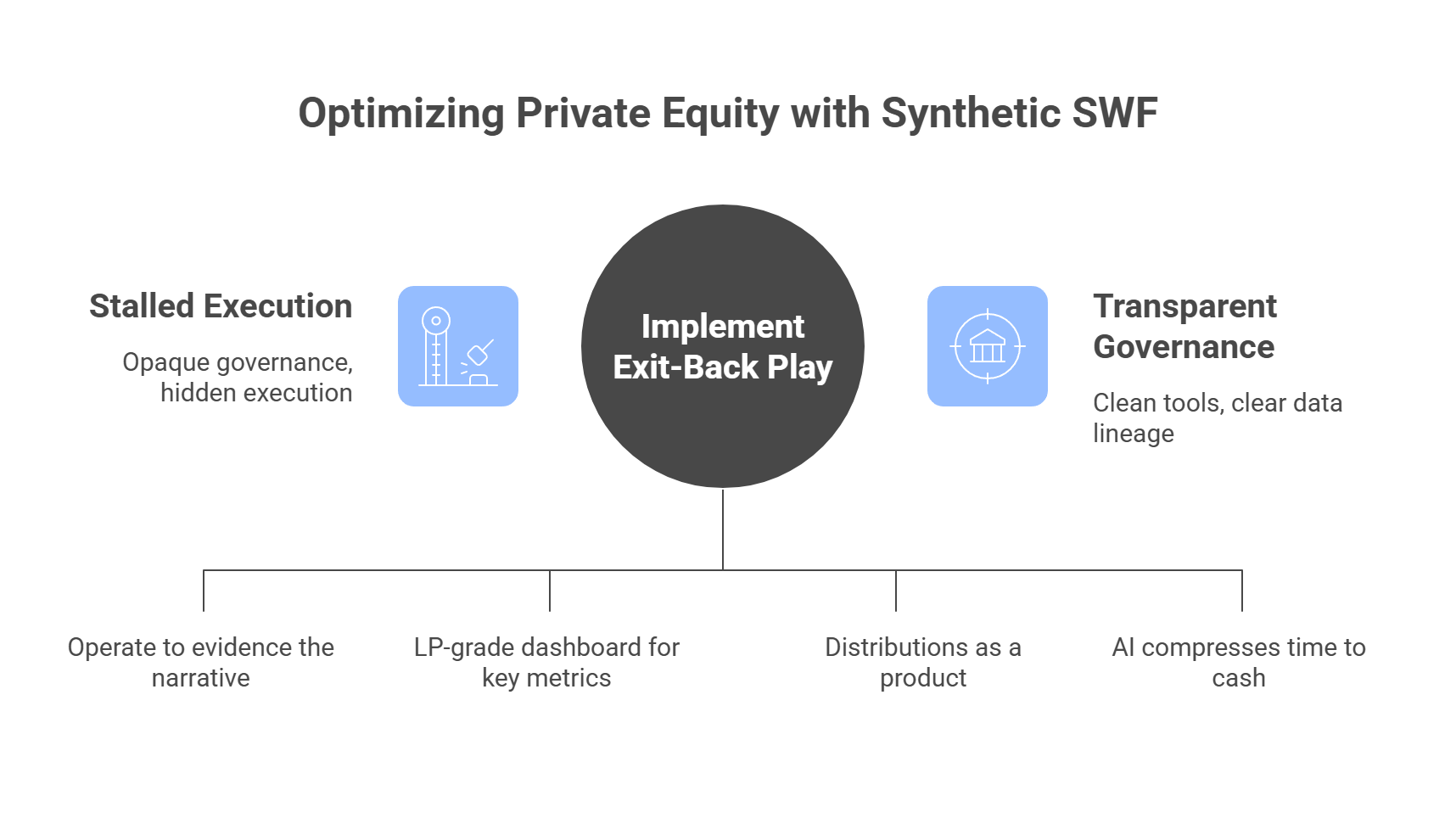

How private equity should work with the synthetic SWF

Run an Exit-Back play from Day 1. Publish the buyer narrative internally at signing and operate to evidence. Turn the CIM into a screenshot of operating reality, not a brochure.

Instrument the value chain. Give LPs an LP-grade dashboard for funnel, unit economics, cash conversion, labor productivity, customer health, and pricing realization. If you champion operational alpha, show it every week, not just in quarterly PDFs.

Prefer DPI over poetry. The US LP base pays bills. Treat distributions as a product. Use continuation vehicles and secondaries as clean tools with transparent governance, not crutches that hide stalled execution.

Prove your digital alpha. Use AI where it compresses time to cash, not to perform “transformation theater.” Install telemetry that quantifies dollars saved and dollars earned, today, with data lineage that survives diligence.

A mental model: the organism, the plumbing, the referee

-

The organism is the asset owner mosaic: DC savers, pensions, TSP, endowments, foundations, state funds.

-

The plumbing is the market stack: exchanges, bonds, secondaries, custody, OCIOs, consultants.

-

The referee is fiduciary law: prudence and loyalty, documented and enforceable.

Put them together and you get a decentralized super-fund large enough to shape private markets, yet competitive enough to avoid the complacency of monopoly capital. That is why the United States can lack a national SWF and still behave like it has the largest sovereign investor on earth.

Citations

Retirement assets, 401(k) and IRA totals, TSP detail: Investment Company Institute, “Retirement Assets Total 43.4 Trillion in Q1 2025,” and TSP component. ici.org

TSP crosses 1 trillion: Federal News Network, June 2025. federalnewsnetwork.com

Public pension assets and Census confirmation: NASRA and US Census 2025 release. nasra.org+1

Endowment and foundation scale: Financial Times on the Yale model and total endowments, FoundationMark on foundation assets. Financial Times+1

US market depth: Siblis Research on equity market value, SIFMA on fixed income outstanding. Siblis Research+1

ERISA fiduciary standards: DOL booklet and DOL fact sheet on prudence and loyalty. DOL+1

State SWF examples: Alaska Permanent Fund Corporation, Texas PSF, New Mexico SIC, North Dakota Legacy Fund. Retirement Investment Office+3LinkedIn+3Texas Permanent School Fund Corporation+3

Policy whiplash example: Reuters coverage of Texas PSF and BlackRock. Reuters

Copyright VCI Institute 2025

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.