The Working Capital Trap

Sep 17, 2025

A seller’s playbook to defend headline price with a clean peg, tight definitions, and audit-ready evidence

Founders celebrate the LOI and then discover the real battle happens in the purchase price adjustment. The most common haircut arrives through the net working capital true up. If the peg is set on a lazy average or the definition is fuzzy, a great headline turns into a smaller wire. Treat working capital like a mini deal inside the deal.

What buyers mean when they say “working capital”

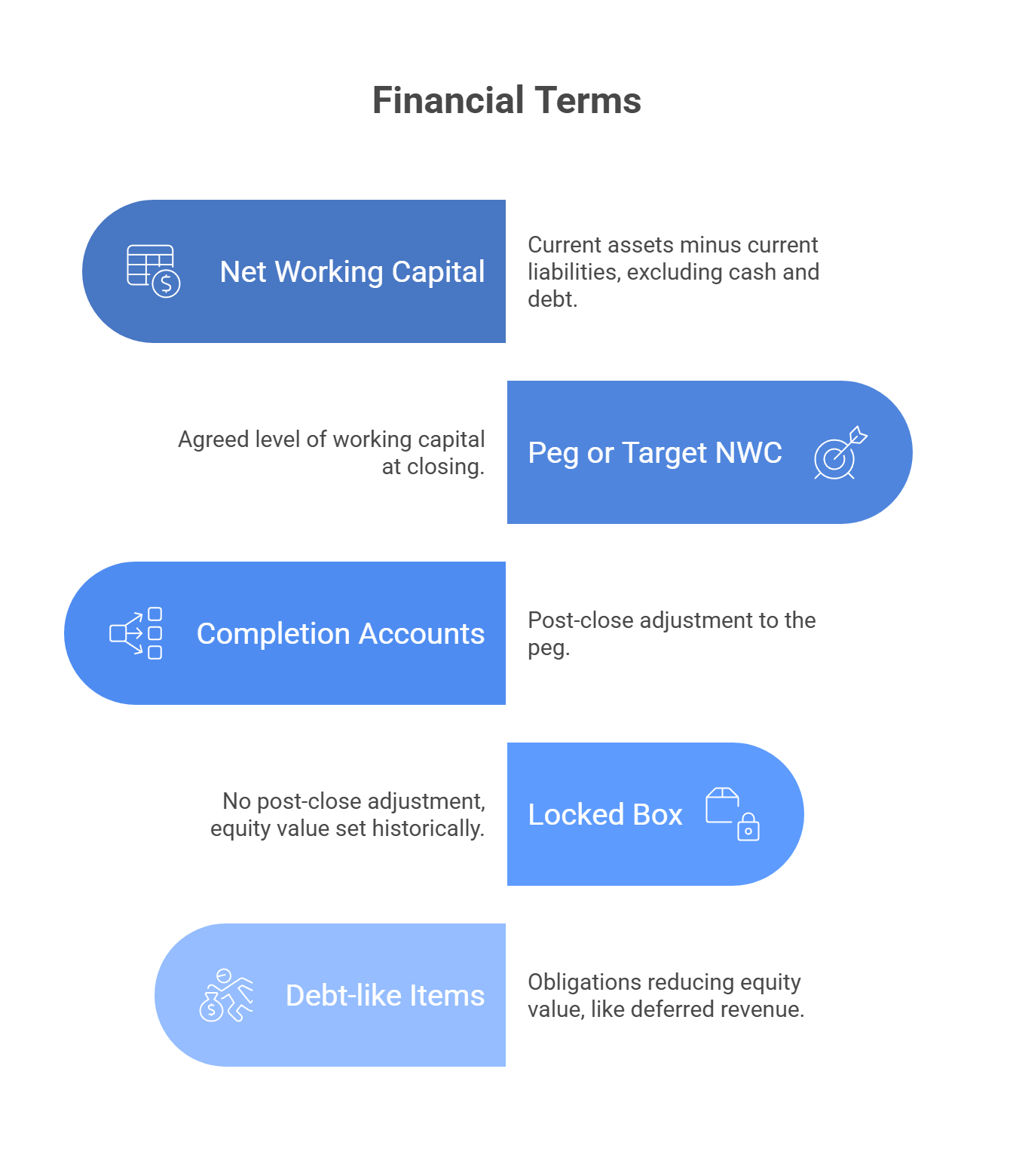

Net Working Capital (NWC): current assets minus current liabilities, typically excluding cash and debt items.

Peg or target NWC: the level you agree the business should deliver at closing.

Completion Accounts: post close true up to the peg.

Locked Box: no post close true up. Equity value set off a historical date with leakage protections.

Debt-like items: obligations that behave like debt and reduce equity value, for example deferred revenue in many software deals, accrued payroll taxes, or customer deposits.

Keep these five terms in your pocket. They show up in every SPA and they decide money.

How value leaks without you noticing

-

A straight 12-month average ignores seasonality and growth.

-

Off system discounts and credit memos spike AR dilution after closing.

-

Inventory reserves are optimistic, so a count later reveals a shortfall.

-

Deferred revenue is suddenly labeled debt-like after you shook hands on price.

-

Cut off rules change at the last minute and move invoices across the line.

Each is small on paper. Together they move millions.

A simple numbers picture

List price 250. Peg proposed on a 12-month average equals 20. But the business doubled in the last four quarters and customers now pay slower during a platform migration. True run rate NWC is closer to 23. If you accept 20, and deliver 22.5 at close, the purchase price adjusts down 2.5. If you agree the peg at 23 with a narrow collar, the same close is within band and no cash moves. The data decides which story wins.

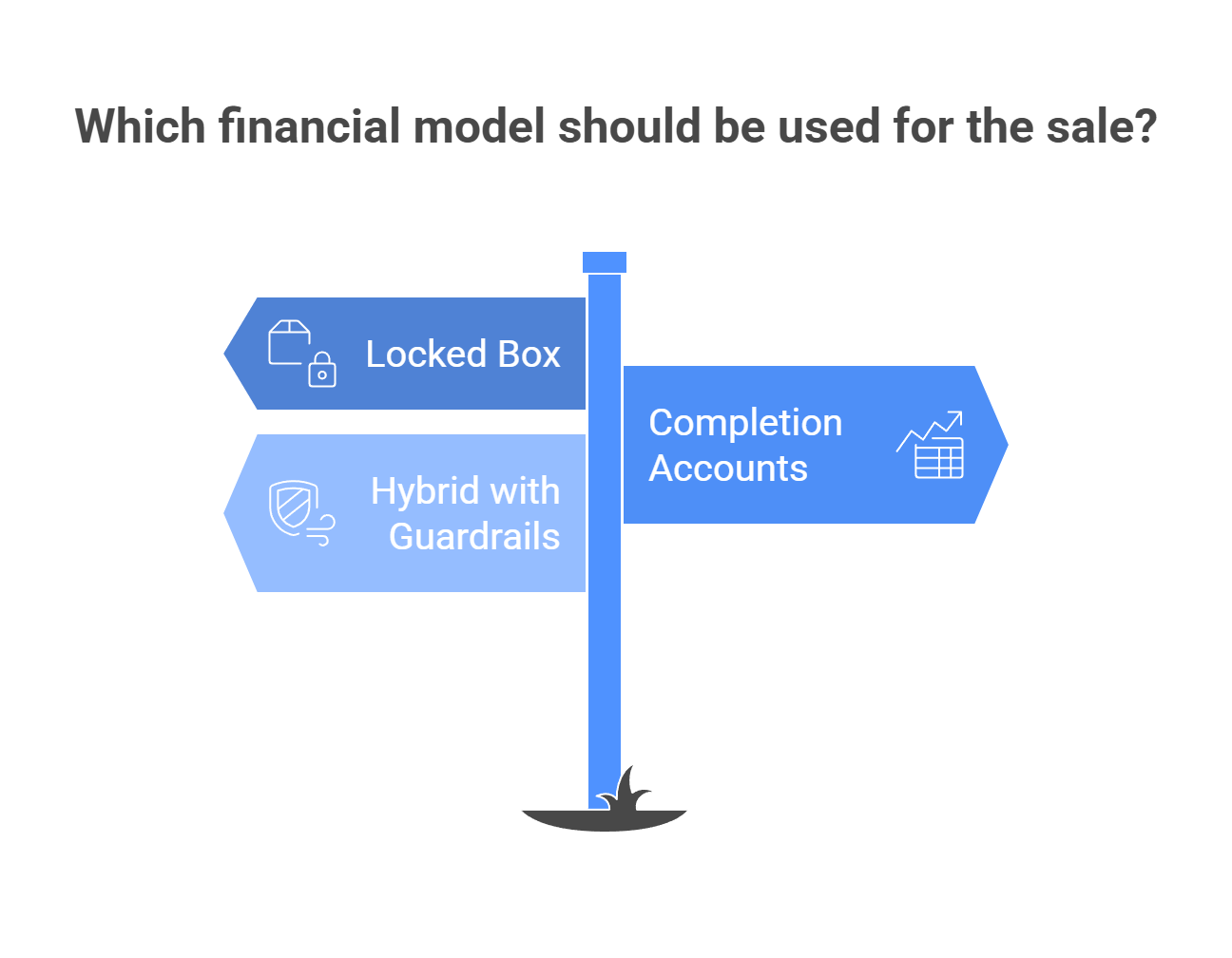

Three models sellers should know

Locked Box when books are clean and leakage is controllable

-

No NWC true up. Interest style “ticking fee” optional.

-

Demands tight leakage list and covenants on value leakage between the box date and close.

-

Good fit for predictable businesses with steady seasonality.

Completion Accounts when volatility is real but trending up

-

You want a forward looking peg, not a backward average.

-

Add collars so small swings do not trigger cash movement.

-

Pre agree debt-like schedules and cut off tests.

Hybrid with guardrails

-

Completion Accounts plus narrow band collar and pre signed policy memo.

-

Independent accountant to arbitrate quickly on defined policies only.

The price defense map

Think in three lanes. Definition. Evidence. Mechanics.

1) Definition: write the rules before the game starts

-

Define current assets and current liabilities precisely.

-

List debt-like items on a schedule so they cannot double count later.

-

State that Completion Accounts follow the same policies and materiality as the last audited set.

-

Carve out one time items such as a safety stock build or a temporary vendor prepay.

2) Evidence: show your work so the peg is obvious

-

Provide a 13 month NWC bridge with seasonality callouts and growth annotations.

-

Disclose AR aging with credits and deduction trends and a dispute log for the top twenty customers.

-

Show inventory roll-forward by family with excess and obsolete policy and write down history.

-

Map deferred revenue to delivery obligations and support with cohort retention.

3) Mechanics: reduce drama with small, clear rules

-

Collar: agree a neutral band, for example plus or minus 2 to 3 percent of enterprise value, where no cash changes hands.

-

Cut off tests: lock revenue recognition, unbilled rules, and credit memo timing.

-

No double dip: if an item lowered EBITDA in QoE it cannot also change NWC for the purchase price adjustment.

-

Dispute path: independent accountant resolves within 30 days using the agreed policy memo only.

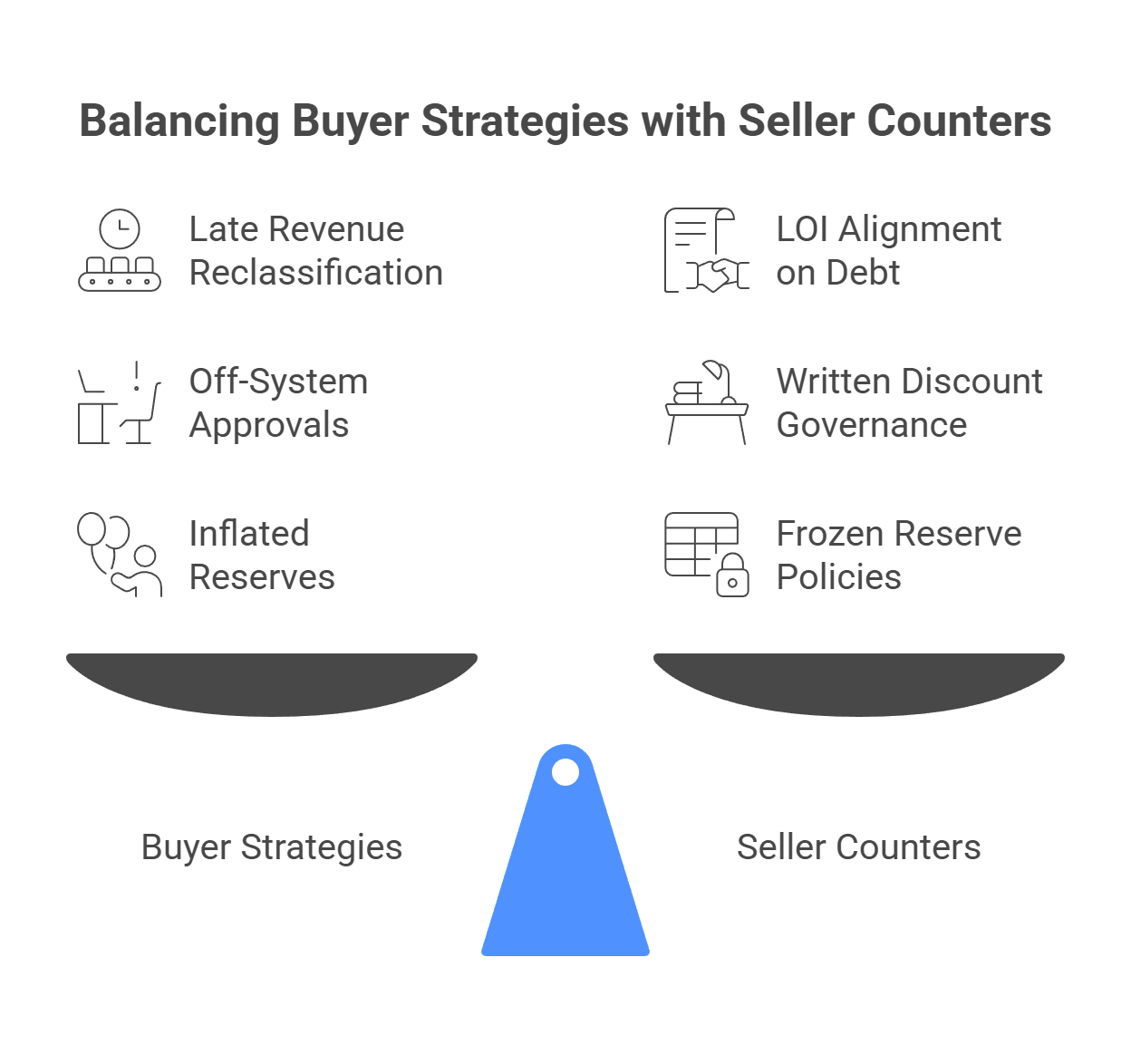

Buyer plays and seller counters

Play: Average peg on the last twelve months.

Counter: Forward peg using last quarter annualized, adjusted for current customer terms and mix, with a 13 month support file.

Play: Late reclassification of deferred revenue as debt-like.

Counter: Align treatment in the LOI. If treated as debt-like, negotiate offsets for prepayment benefit, low CAC payback, or implementation liabilities already delivered.

Play: Off system approvals create post close credit memo spikes.

Counter: Put discount governance in writing and export approvals from the quoting tool. Share dilution trend lines.

Play: Stretch AP to flatter cash while the peg is set.

Counter: Provide vendor aging and service level risks. Align on an AP cap relative to historical DPO.

Play: Inflate reserves just before close to pull down NWC.

Counter: Freeze policies and materiality thresholds to the last audited period. Document counts and reserve math.

The data room that sells for you

Organize evidence so a fair peg is undeniable.

Structure

01 Financial statements and NWC bridges

02 Accounting policy and materiality memo

03 AR aging, credits and deductions, dispute log

04 Inventory roll-forward, counts, E and O policy, write down history

05 AP aging, vendor terms, critical vendor list

06 Deferred revenue waterfall and delivery schedule

07 Contracts with billing and acceptance language

08 KPI dictionary for DSO, DPO, turns, reserves, dilutions

Naming

Use YYYY-MM prefixes and consistent labels so buyers can trace lineage without hunting.

Industry lenses

Software and subscription

-

Deferred revenue treatment is the pivot. Clarify in LOI.

-

Cohorts, renewal cash timing, and support obligations drive the peg.

Distribution and product

-

Multi location cycle counts and credible E and O policy matter more than a deck.

-

Mix and seasonality drive inventory and should shape the peg window.

Services and projects

-

Work in progress rules and change order governance decide unbilled receivables.

-

Milestone acceptance language in customer contracts becomes an accounting rule at close.

Ten clauses founders ask for in plain language

-

NWC equals current assets minus current liabilities, excluding cash, debt, and the debt-like list in Schedule X.

-

Completion Accounts prepared using the same policies and materiality thresholds as the latest audited financials.

-

Peg set at Q2 run rate NWC adjusted for customer term changes since Q1, supported by the 13 month bridge.

-

Collar of plus or minus 2.5 percent of enterprise value.

-

No double dip between QoE EBITDA normalizations and NWC adjustments.

-

Deferred revenue treatment specified and offset mechanics documented.

-

Unbilled receivables recognized only for signed, enforceable milestones.

-

Credit memos post close must follow historical policy and cannot reprice pre close shipments.

-

Independent accountant to resolve disputes within 30 days.

-

Seller right to observe inventory counts and AR collections cut off.

Work with counsel to tailor jurisdictional language, but hold the concepts.

Founder FAQ

Can I avoid the true up entirely

Yes, with a Locked Box and strict leakage protections, if your books are clean and seasonality is low.

What if my business is growing fast and needs more NWC

Use a forward peg and show why. Growth consumes working capital. Buyers accept this when the file is clear.

What is realistic on a collar

Enough to remove noise, small enough to prevent sloppy behavior. Often 2 to 3 percent of enterprise value.

Who should own this fight inside my company

The CFO for numbers and policy, the controller for cut offs, sales ops for discount governance, supply chain for inventory rules, and your QoE provider to tie it all together.

Bottom line

Headline price is a promise. The peg decides the wire. Define working capital early, prove the run rate with clean files, and engineer simple mechanics that keep emotions out of the math. Do that and you turn a common trap into found money.

Copyright © 2025 VCI Institute. All rights reserved.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.