Where PE and SWFs Diverge, and Where They Quietly Converge

Sep 17, 2025

What separates private equity GPs from sovereign wealth funds, and how each creates value

Private equity general partners and sovereign wealth funds increasingly meet in the same deals, often on the same side of the cap table. Yet they are built for different jobs. GPs are product manufacturers raising finite-life funds, paid to turn committed capital into DPI on a timetable. SWFs are asset owners with permanent or very long-dated capital, balancing financial returns with national and strategic objectives under public scrutiny. Those design choices ripple through sourcing, underwriting, ownership style, governance, and exits.

Below is a practical comparison that founders, co-investors, and boards can use to anticipate how each party will behave and where value creation levers differ.

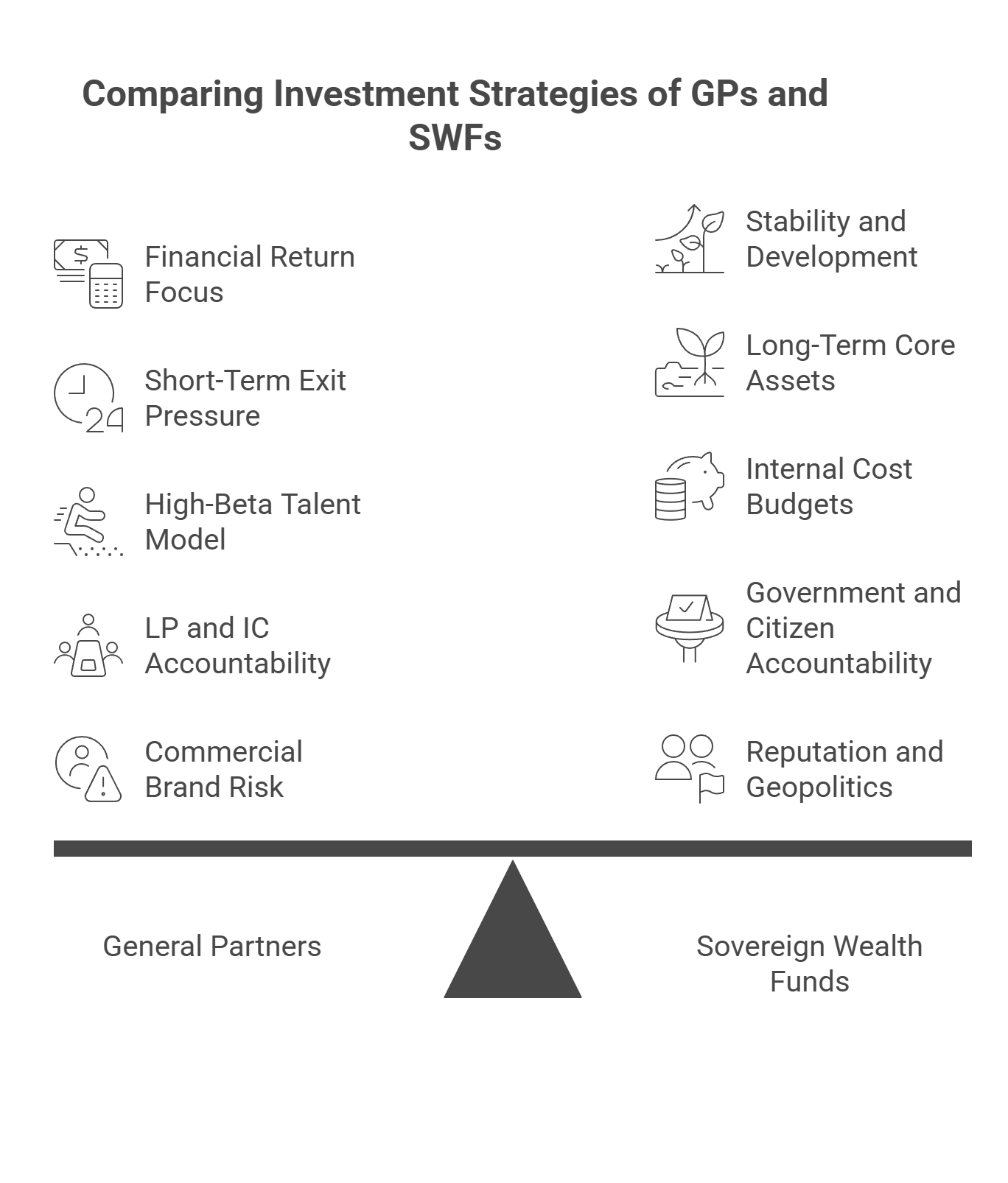

Core design differences

Mandate and objective

-

GPs: Financial return, fund life driven, DPI on a schedule.

-

SWFs: Financial return plus stability, diversification, and often development or strategic aims such as jobs, technology transfer, or domestic infrastructure. The Santiago Principles codify governance and transparency expectations for SWFs, which shapes how they invest and disclose.

Capital and time horizon

-

GPs: Closed-end funds, vintage pacing, exit pressure when the fund ages.

-

SWFs: Permanent or very long-term pools that can hold core assets, tolerate lower liquidity, and lean into long-lived themes such as clean energy or national digital infrastructure.

Cost and incentives

-

GPs: Management fees and carry, high-beta talent model that rewards speed and realized gains.

-

SWFs: Internal cost budgets and salary-bonus structures with smaller carry pools or none. Many SWFs internalize capabilities to save on fees and gain control over pacing and portfolio design.

Governance and accountability

-

GPs: Answer to LPs and ICs, audited valuations, frequent reporting.

-

SWFs: Answer to government frameworks and citizens, often publish policy statements aligned to the Santiago Principles to demonstrate independence and prudence.

Public profile and headline risk

-

GPs: Commercial brand risk.

-

SWFs: Reputation and geopolitics matter more, so sector, geography, and partner selection often reflect foreign-policy and domestic-policy constraints in addition to returns.

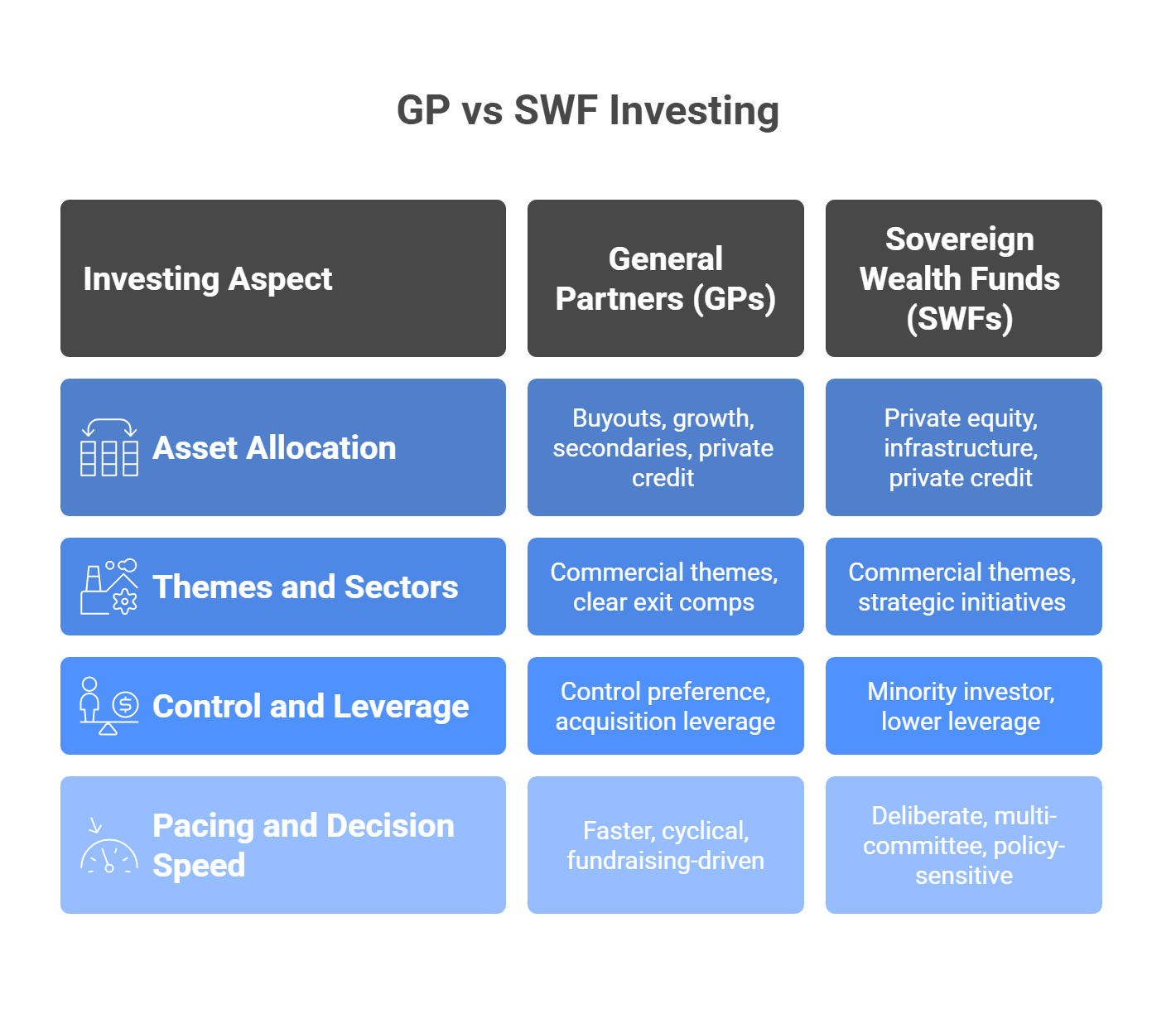

Where they invest and how they own

Asset mix

-

GPs: Buyouts, growth, secondaries, and increasingly private credit.

-

SWFs: Broad multi-asset owners. Alternatives have risen as a share of AUM, with meaningful allocations to private equity, infrastructure, and private credit, varying by region and fund design.

Themes and sectors

-

GPs: Commercial themes with clear exit comps.

-

SWFs: Similar commercial themes plus strategic ones. Recent examples include heavy emphasis on AI, digital infrastructure, renewables, and domestic industrial platforms that advance national capability.

Control and leverage

-

GPs: Prefer control or strong influence, use acquisition leverage sized to the exit plan.

-

SWFs: Comfortable as minority or anchor investors, often prefer lower leverage, and may co-sponsor with GPs or consortiums for scale and knowledge transfer.

Pacing and decision speed

-

GPs: Faster, cyclical, fundraising-driven.

-

SWFs: Can be deliberate, multi-committee, and sensitive to public policy calendars. The upside is patience. Norway’s fund publicly advocates for practices that foster long-term thinking in markets.

Value creation levers, side-by-side

| Lever | How GPs typically use it | How SWFs typically use it |

|---|---|---|

| Operational alpha | Pricing, mix, throughput, working capital, professionalize management, roll-ups | Similar toolset, often via operating partners or GP partnerships, with tolerance for longer build periods in infrastructure and industrial platforms |

| Capital structure | Optimize leverage, refinancing windows, continuation vehicles for hold-period flexibility | Lower leverage bias, use of patient capital and club structures, selective use of secondaries for liquidity at the portfolio level |

| Technology and data | Commercial growth, price realization, go-to-market engines, AI for conversion and cost | Enterprise-grade data governance, national digital priorities, AI adoption across portfolios with a focus on security and resiliency |

| ESG and policy alignment | LP-driven disclosure and risk management | Policy-driven, often a core mandate. Climate and domestic development targets can be explicit investment criteria. static.ie.edu |

| Exit engineering | Timing to buyer cohorts, evidence-rich CIMs, continuation options | Flexible horizons, strategic sales and public-market placements sized to liquidity needs and policy optics |

Where they increasingly converge

-

Internalization of capabilities

SWFs have grown private-markets teams, co-invest more often, and partner directly with leading GPs to reduce fees and gain influence. Many are building in-house value creation skill sets that look PE-like. -

Bigger role across private markets

Both are leaning into private credit, infrastructure, and digital assets that offer durable cash flows, inflation linkage, or secular growth, aided by abundant dry powder and a gradual recovery in deal activity. -

Data-first underwriting and monitoring

Leading GPs and SWFs now underwrite with richer operating telemetry and expect evidence that stands up in diligence. This is a shared language across the table, not a gimmick.

Partnership playbook: how to work together without friction

For GPs partnering with SWFs

-

Offer operating proof, not theater. Publish the playbook, the cadence, and the ROI math for tech and operating programs. SWFs reward evidence and policy stability.

-

Engineer optionality. Club deals, minority protections, and routes to staged liquidity respect SWF pacing while preserving GP exit paths.

-

De-risk headlines. Pre-bake governance, ESG disclosures, and cybersecurity representations. Many SWFs carry higher headline sensitivity.

For SWFs partnering with GPs

-

Request a buyer-grade operating pack. Cohorts, contribution dollars, price realization, and cash conversion, with data lineage. This aligns with your longer horizon and reduces valuation drift later.

-

Insist on alignment beyond fees. Co-design earnout-like value milestones for GP operating teams on co-sponsored platforms.

-

Codify policy stability. Freeze accounting and performance definitions for key metrics so goalposts do not move through political cycles.

What to expect by region and strategy

-

Gulf and East Asia SWFs: Rising allocations to private equity, private credit, and AI-adjacent themes, with visible co-sponsorship and GP stakes activity.

-

Emerging national funds: Dual mandates are common. Domestic infrastructure, digital independence, and industrial platforms receive priority alongside returns.

-

OECD-style reserve funds: Emphasize governance, diversification, and market standards, often as universal owners with strong stewardship preferences.

The takeaway for company leaders and sellers

If your buyer group includes both a GP and an SWF, you are negotiating with two clocks. The GP’s clock measures DPI and fund life. The SWF’s clock measures total system value and public accountability. Build a plan that feeds both: near-term operational gains that produce cash and buyer-grade evidence for the GP, and a resilient, policy-proof platform with clean governance for the SWF. When you do, the check is larger and the relationship is calmer.

Copyright © 2025 VCI Institute. All rights reserved.

Selected sources

-

McKinsey Global Private Markets Report 2025 on the private-markets recovery and LP dynamics. McKinsey & Company

-

Bain Global Private Equity reports on dry powder and the growing role of SWFs as capital providers and co-investors. Bain

-

IFSWF Santiago Principles on SWF governance and transparency standards. IFSWF

-

Invesco Global Sovereign Asset Management Study 2025 on SWF allocations to alternatives and portfolio construction trends. Invesco

-

FT on Mubadala’s strategy tilt to PE, AI, and private credit, illustrating active SWF direct investing. Financial Times

-

Reuters on Norway’s long-term stewardship stance and Reuters on INA’s domestic development focus, highlighting strategic objectives beyond pure financial return. Reuters+1

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.