The Carry Parity Question: When Operating Partners Stop Being Treated as Service Functions

May 13, 2026

The clearest signal of where a private equity firm sits on the operating partner question is not on the website. It is in the carry distribution. Firms that allocate carry to operating partners on par with deal partners at equivalent seniority levels have made a structural commitment to operations as a core driver of value creation. Firms that allocate carry to operating partners at meaningfully lower levels, regardless of what the website says, have made a different commitment. The discount communicates that operations is, in the firm's actual economics, a service function rather than a partnership function.

This signal is read by candidates in the operating partner market, by LPs evaluating sponsor capability, and by the operating partners already inside the firm. It is read accurately. The firms that have closed the gap are recruiting differently than the firms that have not. The difference, over time, produces a self-reinforcing dynamic that compounds in favor of the parity firms.

What the Compensation Gap Has Looked Like

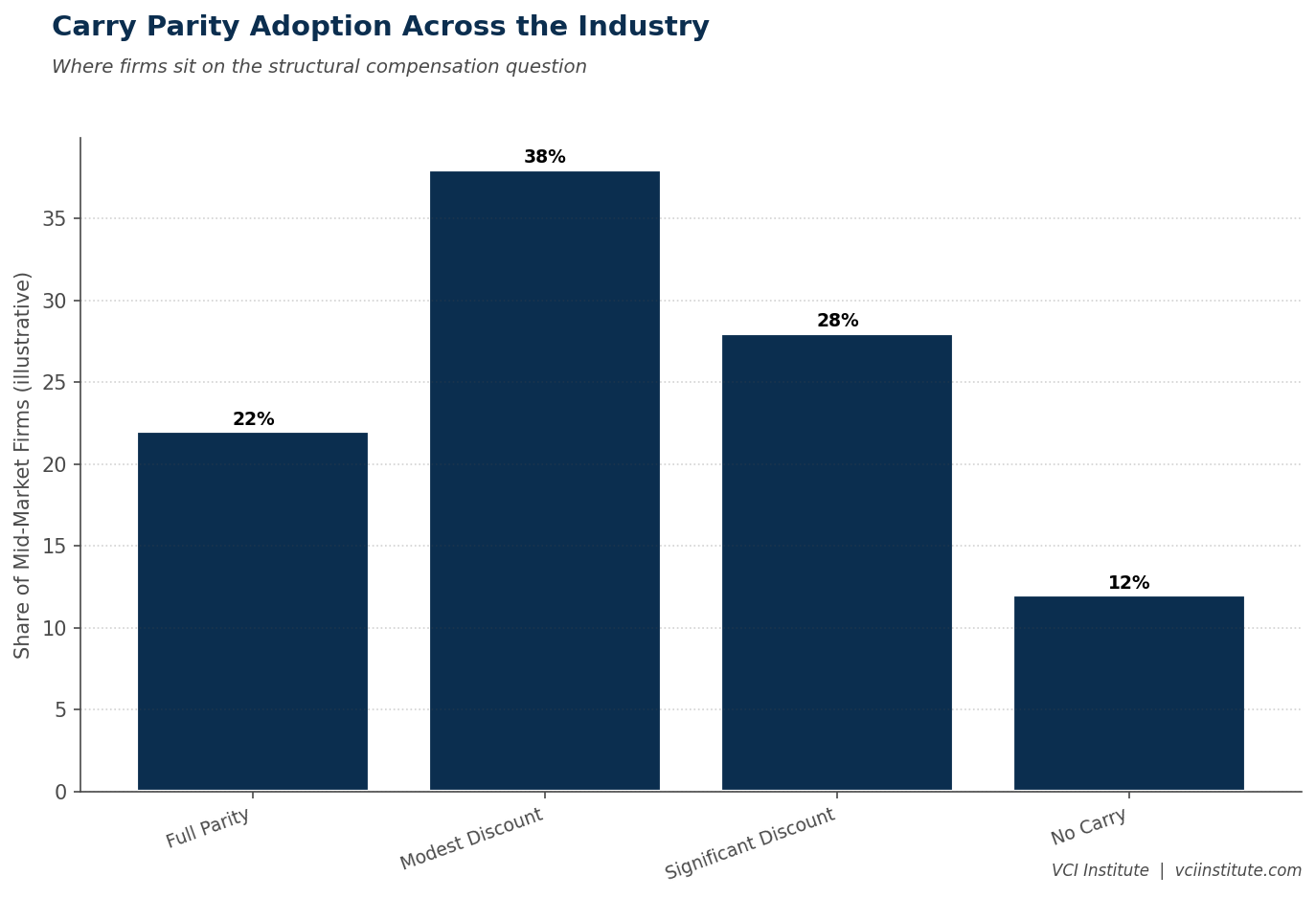

For most of the modern private equity era, operating partners have received carry allocations meaningfully below those of deal partners at equivalent levels. The discount has varied. Some firms have applied a small discount of fifteen to twenty percent. Others have applied larger discounts of forty to sixty percent. Some firms have not provided carry to operating partners at all, treating them as compensated through cash and bonus structures alone.

The justifications for the discount have been varied. Operating partners do not source deals. Operating partners are not on the investment committee. Operating partners do not put capital at risk in the same way deal partners do. Operating partners are operating, not investing. Each justification has the surface logic of describing how things have been done. None of them holds up well against what operating partners actually contribute to fund returns.

The data from the firms that have done this honestly tells a different story. Operating partner contribution to value creation outcomes is, in well-functioning firms, comparable to deal team contribution. The deal team selects the deals. The operating team executes the value creation plans that produce returns above the underwriting case. Both are necessary. Neither alone is sufficient. The compensation discount that treated one as primary and the other as supportive was a historical artifact, not an economic truth.

The Shift Underway

Over the past five years, this artifact has begun to dissolve. Several leading firms have explicitly closed the carry gap, moving operating partners to parity with deal partners at equivalent seniority levels. The shift is not universal but it is meaningful. The firms that have made the change report that the recruiting market has responded immediately. The candidates they used to lose to other firms are now winnable. The candidates they used to settle for are now upgradable. The pipeline of senior operating talent willing to engage with their firm has deepened.

The firms that have not made the change are seeing the inverse pattern. Their operating partner recruiting has become harder. The candidates they need are increasingly aware of which firms offer parity and which do not. The discount that used to be invisible has become visible, and visibility produces consequences in a tight talent market.

This is not a fad. It is a structural realignment. The firms that have made the move are signaling that operations is a partnership function. The firms that have not are signaling that operations remains a service function, regardless of how the firm describes itself externally.

What Carry Parity Actually Signals

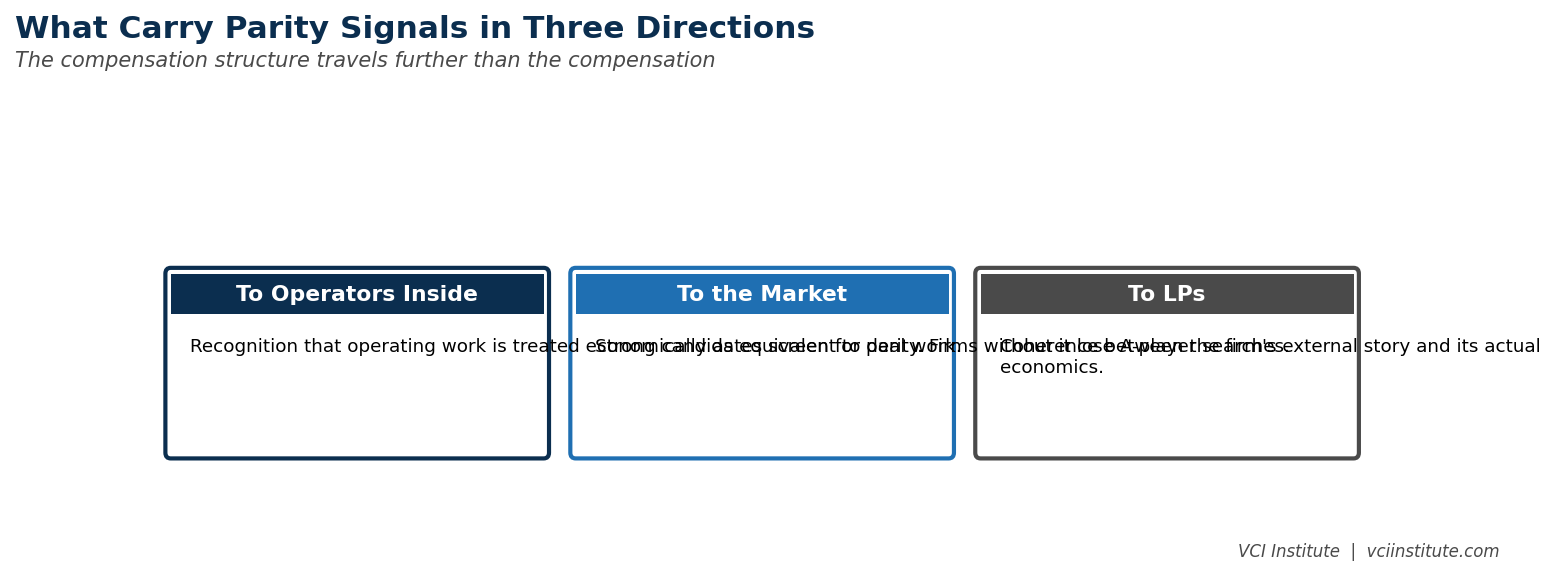

Carry parity is a compensation structure, but its real value is in what it signals about the firm's commitment to operations. The signal travels in three directions.

The first direction is internal. Operating partners inside the firm experience carry parity as recognition that their work is treated economically as equivalent to the deal team's work. This produces a cultural shift that goes beyond compensation. Operating partners speak with more authority in portfolio company governance. They engage more actively in deal selection. They behave more like partners and less like supportive functions, because the firm has signaled that they are partners. The behavioral change compounds the economic value over time.

The second direction is to candidates. Senior operating talent in the market has become sophisticated about the carry parity question. Candidates ask about it explicitly in interviews, often in the first meeting. The firms that have parity recruit easily. The firms that have a discount have to explain the discount. The explanations rarely persuade strong candidates, who treat the discount as a signal that the firm has not actually decided what it wants operations to be. The recruiting cost of the discount, over a five year period, is substantial.

The third direction is to LPs. Sophisticated LPs evaluating sponsor capability ask about how the firm structures its operating partner economics. Firms with parity structures present a coherent story about the seriousness of their operations function. Firms with discount structures present a story that does not match the firm's external positioning. LPs read this incoherence as a signal about institutional discipline. Over a fund cycle, the read affects allocation decisions.

What Parity Costs

Closing the carry gap is not free. The economics of the firm have to absorb the difference. There are three places the absorption typically happens.

The first place is in deal team carry allocations. If operating partners receive parity, the total carry pool either grows or is reallocated. In firms where the pool is fixed, deal partner allocations are reduced to make room. This produces internal politics that have to be managed. Deal partners who have historically received the larger share of carry do not enjoy the change. Firms that have made the move successfully have done so through careful internal engagement, with senior leadership making the case that the firm's overall economics improve when the operating partner function is properly resourced and motivated.

The second place is in fund economics. Some firms have absorbed the carry parity shift by accepting modestly lower management fees or by accepting higher operating costs that come out of management fees. The economics still work because the value creation outcomes the parity structure unlocks more than offset the cost. The math has to be done deliberately. It has to hold under realistic assumptions about how parity actually changes outcomes.

The third place is in slower hiring. A firm that has committed to carry parity for operating partners has to be more selective in hiring, because each hire now consumes more economic capacity. This is not necessarily a bad thing. It produces tighter operating partner teams with stronger senior people, rather than larger teams with weaker average quality. The discipline of hiring under the parity constraint sometimes improves the quality of the operating partner function over time.

The Implementation Path

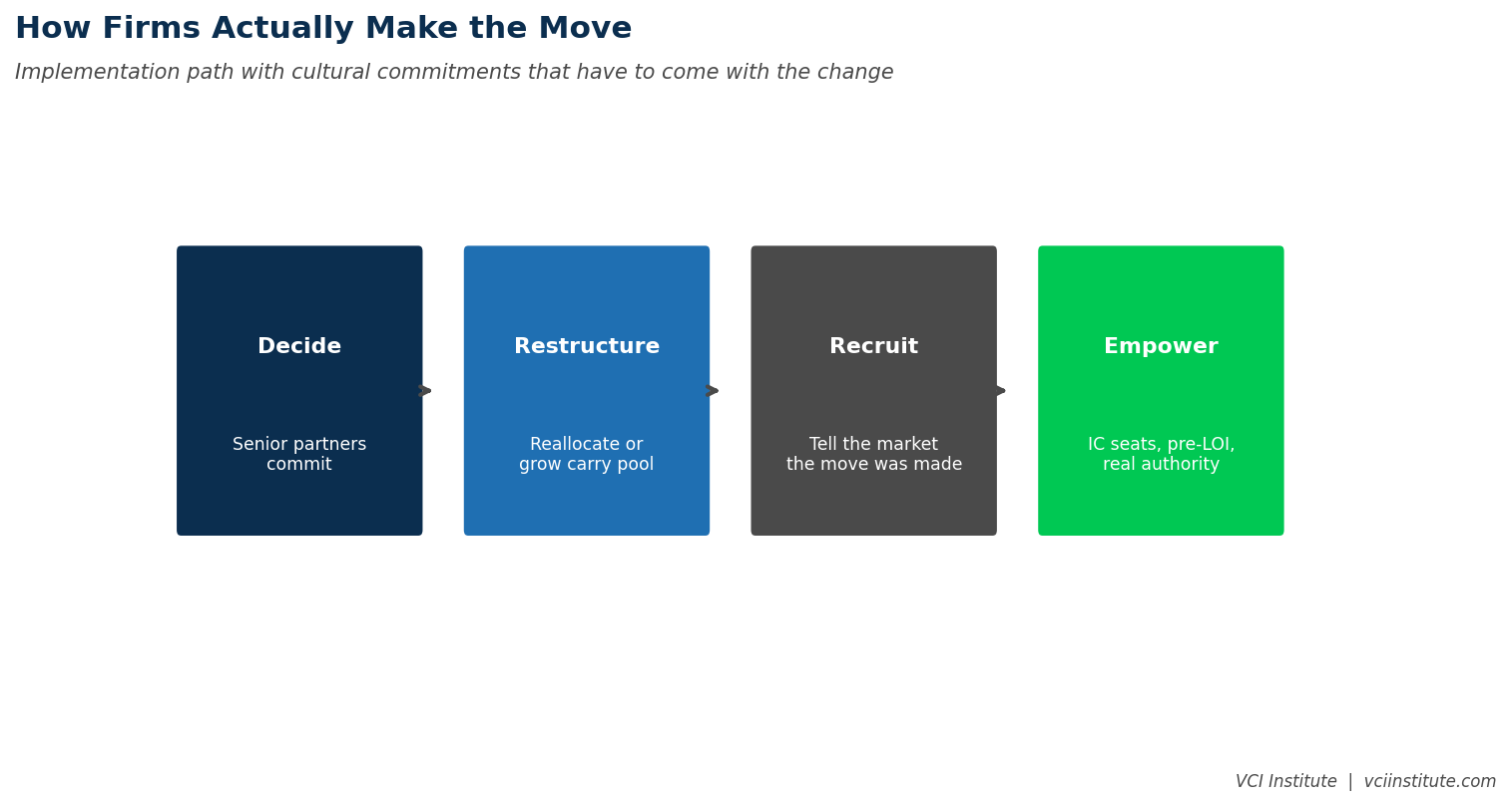

Firms considering the move to carry parity face an implementation question. The transition has to be managed carefully, both internally with existing team members and externally with the recruiting market.

The internal transition is the harder one. Existing operating partners who have been on discounted carry structures need to be moved to parity, ideally for new vintages of carry rather than retroactively, but with the change communicated clearly enough that the operating partners feel the firm has acknowledged the shift. Existing deal partners need to engage with what the change means for the firm's economics, and senior leadership needs to make the case that the change is good for the firm rather than a transfer from deal teams to operations.

The external transition is the easier one. Once the firm has made the move, it can communicate clearly to the recruiting market that operating partners receive carry on par with deal partners at equivalent levels. The recruiting market responds immediately. The firms that have made the move have reported a meaningful improvement in their candidate pipelines within the first hiring cycle.

The cultural transition is the longest one. Carry parity is a compensation structure, but for the structure to produce the value creation outcomes that justify it, the firm has to actually treat operations as a partnership function. This means investment committee participation. Pre-LOI involvement. Operating partner authority on management decisions. Operating partner voice in major value creation choices. Without these structural commitments, carry parity by itself produces frustrated operating partners who have parity compensation but service function authority. With these commitments, carry parity produces the kind of operating partner function that is genuinely competitive with the deal team in shaping outcomes.

The Cost of Standing Still

Firms that choose not to close the carry gap face costs that are growing. The recruiting market is shifting against them. Candidates increasingly screen for carry parity in their first conversations. Strong candidates who would have accepted discounted compensation five years ago now turn down opportunities that include the discount. The firms that maintain the gap are recruiting from a thinner candidate pool every year.

The internal costs are also growing. Operating partners who become aware that other firms have moved to parity look at their own compensation structure with increasing dissatisfaction. The discount that was invisible in 2020 is highly visible in 2026. Operating partners who feel structurally underpaid relative to peers at parity firms are recruitable. Some leave. Others stay but disengage. Either pattern hurts the firm.

The external positioning costs are subtler but real. LPs are increasingly aware of which firms have made the move and which have not. The narrative about operations as a core driver of value creation is harder to sustain when the firm's economics treat operations as a discount function. LPs read the gap. The reading affects allocation decisions over time.

The Question Worth Asking

The most useful question a firm can ask itself on this issue is not whether to move to parity. The question is what the carry structure currently signals about the firm's commitment to operations, and whether that signal is the one the firm wants to be sending. If the answer is yes, the firm is consistent. If the answer is no, the firm has a structural incoherence that will compound in costs over the next five years.

The firms that get this right will be the firms that treat operations as a partnership function in compensation structure as well as in marketing materials. The firms that get this wrong will continue to wonder why their operating partner function does not produce the outcomes the website implies it should produce. The compensation structure is upstream of the outcomes. Until the structure changes, the outcomes will not change. The signal is the substance, in this case. The candidates know it. The LPs know it. The operating partners inside the firm know it. The only people who sometimes do not yet know it are the senior leaders who have not yet decided to send a different signal.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.