The Knowledge Engineer: Private Equity's Most Important Hire That No Firm Has Made Yet

Apr 29, 2026

Walk into a typical mid-market private equity firm in 2026 and you will find a team that includes investment professionals, operating partners, finance and accounting staff, investor relations, and an increasing number of technology and data analysts. You will not find a knowledge engineer. The role does not exist on the org chart of more than a handful of firms in the industry. Most senior partners cannot define what one would do.

This is a problem, and it is a tractable one. The knowledge engineer is the role that translates the firm's accumulated reasoning, almost all of which currently lives in the heads of senior people, into structured form that junior team members and AI systems can use. Without this role, the firm's institutional knowledge does not actually exist as a firm asset. It exists as the personal property of whoever happens to currently be employed there.

Every senior departure is a partial brain drain. Every junior hire reinvents pattern recognition that has already been earned. Every AI investment runs on a substrate of documents that contain what was decided but not why. The cost of not having a knowledge engineer is invisible in any single quarter and substantial across a fund cycle.

Figure: 34a role definition

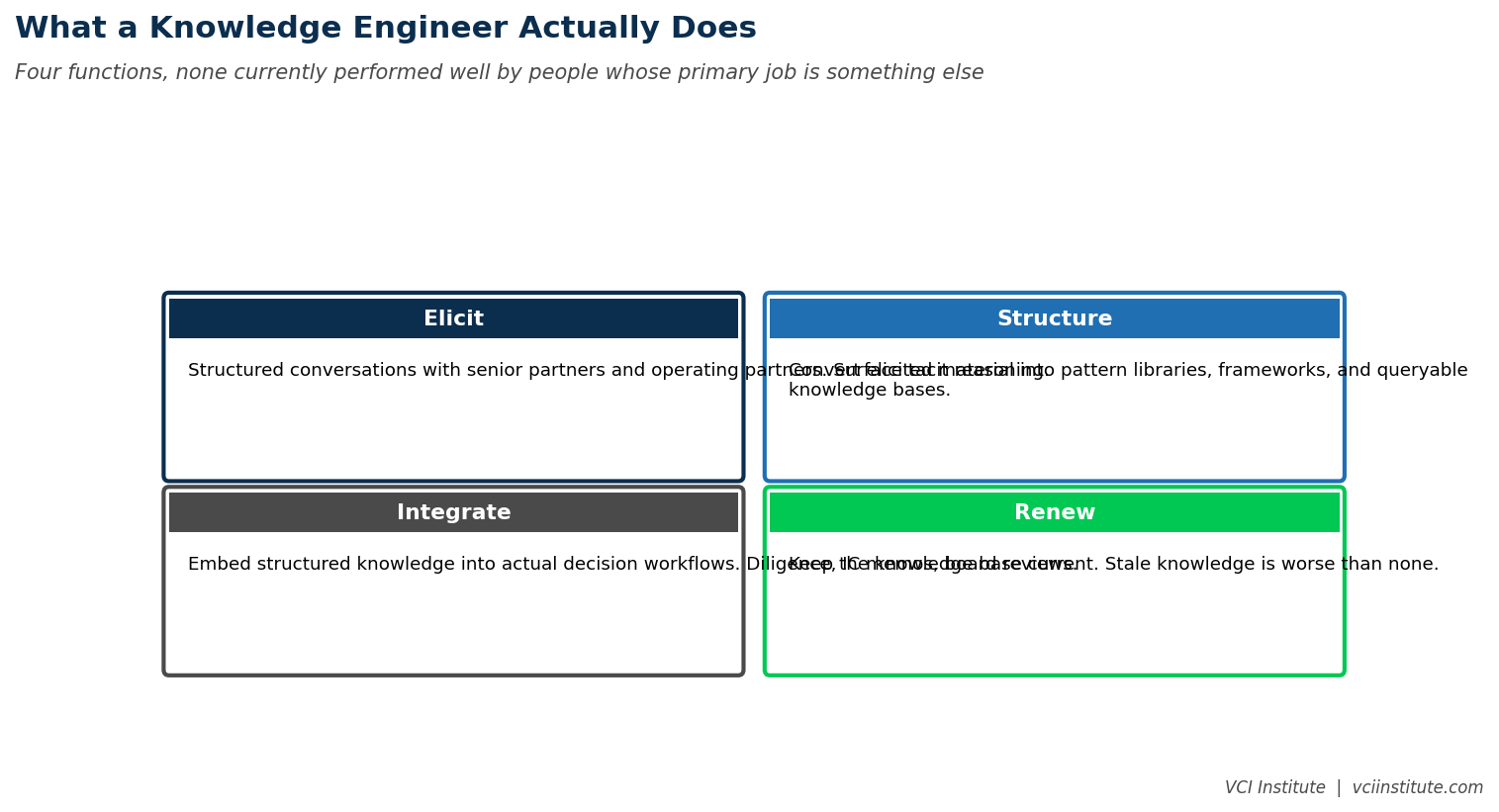

What the Role Actually Does

A knowledge engineer in a private equity context performs four functions, each of which is currently either not done at all or done badly by people whose primary job is something else.

The first function is elicitation. Sitting with senior partners and operating partners in structured conversations, asking the kinds of questions that surface tacit reasoning. How did you decide whether the management team in deal X could execute. What were the three things you noticed that pointed in the right direction or the wrong direction. When you say a deal felt right, what specifically were you reading. When you walked away from a deal that looked good on paper, what were you seeing that the model did not capture. This is interview work. It requires patience and craft. The output is the raw material from which everything else is built.

The second function is structuring. Converting the elicited material into forms that can be queried, retrieved, and reused. Pattern libraries. Decision frameworks. Diagnostic checklists. Annotated case studies. This is not transcription. It is the editorial work of distilling what a senior partner said into a form that a junior team member can use without having to ask the senior partner the same question every time. It also produces the substrate that AI retrieval systems can work against.

The third function is integration. Embedding the structured knowledge into the actual workflows where decisions are made. Diligence checklists in the deal management platform that surface relevant historical patterns at the right moments. Operating reviews that pull in past similar situations as context. Investment committee memos that include the firm's accumulated view on the specific industry pattern, not just the deal team's analysis of the specific company. Without integration, the structured knowledge sits unused.

The fourth function is renewal. Keeping the knowledge base current as the firm learns new things, retires outdated patterns, and accumulates fresh experience. This is the function that most firms underestimate. Knowledge bases that are not actively maintained become stale, and stale knowledge bases are worse than no knowledge bases, because they produce confident but wrong outputs.

These four functions together describe a real job that requires real skill. It is not a junior role. It requires someone who can hold conversations with senior partners productively, who can write clearly, who has enough investment experience to recognize what matters, and who has enough technical fluency to work effectively with the AI and data infrastructure the firm is building.

What the Role Is Not

The knowledge engineer is not a librarian organizing documents. The work of organizing documents matters and is necessary, but it does not require the elicitation skills that define the role. A document organizer can be hired more easily and at a lower level. A knowledge engineer is doing something different and more demanding.

The knowledge engineer is not a data scientist building models. Data science is a separate function. The knowledge engineer's output is structured human reasoning, not predictive models. The two functions complement each other but are not interchangeable.

The knowledge engineer is not a consultant brought in for a specific project. The role is permanent because the work is continuous. Knowledge engineering done as a one-time project produces a deliverable that ages out within twelve months and never gets refreshed. The role has to be inside the firm to do its job.

The knowledge engineer is not a junior support role for the senior partners. The work involves enough authority and enough judgment that it has to be staffed at a level where the senior partners actually engage seriously with the elicitation work. A knowledge engineer who is treated as administrative support produces administrative output.

Figure: 34b what it extracts

What the Role Extracts

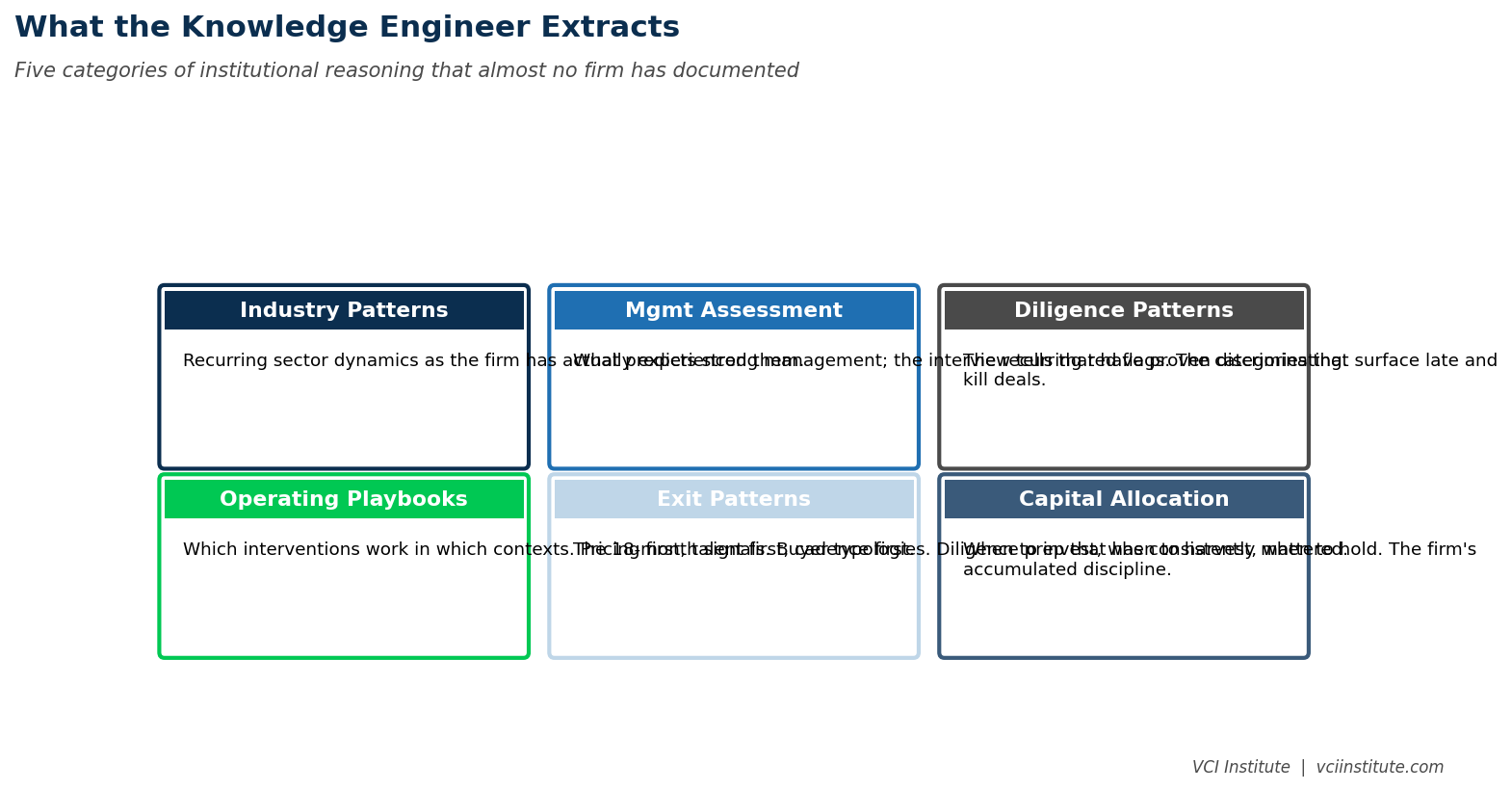

The specific knowledge a knowledge engineer extracts varies by firm, but five categories appear in almost every PE context.

Industry pattern libraries. The recurring dynamics of specific sectors as the firm has experienced them. What goes wrong in food service consolidations. What goes right in specialty distribution roll-ups. The patterns that distinguish a sustainable platform from a roll-up that will unwind. These patterns exist in the heads of partners who have done multiple deals in the sector. They rarely exist on paper.

Management assessment frameworks. The firm's accumulated view of what predicts strong management performance and what predicts weakness. The interview questions that have proven discriminating. The reference patterns that have proven reliable. The trial period observations that have predicted longer term success. This is the institutional learning that prevents the same hiring mistake from recurring every three years.

Diligence pattern recognition. The recurring red flags the firm has learned to look for. The categories of issue that surface late in diligence and have caused deals to die or to be repriced. The specific clauses, customer behaviors, or operating tells that have predicted post-close surprises. This material is the difference between a junior diligence team that runs the standard checklist and a junior team that actually reads the business.

Operating playbook calibration. The firm's view on which value creation interventions work in which contexts. When pricing transformation is the right first move. When talent upgrade should come before operating cadence change. Which industries respond to buy-and-build and which do not. This material distinguishes operating partners with institutional backing from operating partners who are essentially running personal playbooks.

Exit pattern recognition. The firm's accumulated view on what makes exits succeed or drag. The eighteen month signals. The buyer typologies. The diligence preparation that has consistently mattered versus the preparation that did not. The valuation calibration patterns that have proven accurate.

These five categories together represent a substantial corpus of institutional knowledge. Most firms have none of them documented. The knowledge engineer is the person who builds them and keeps them current.

The First Year

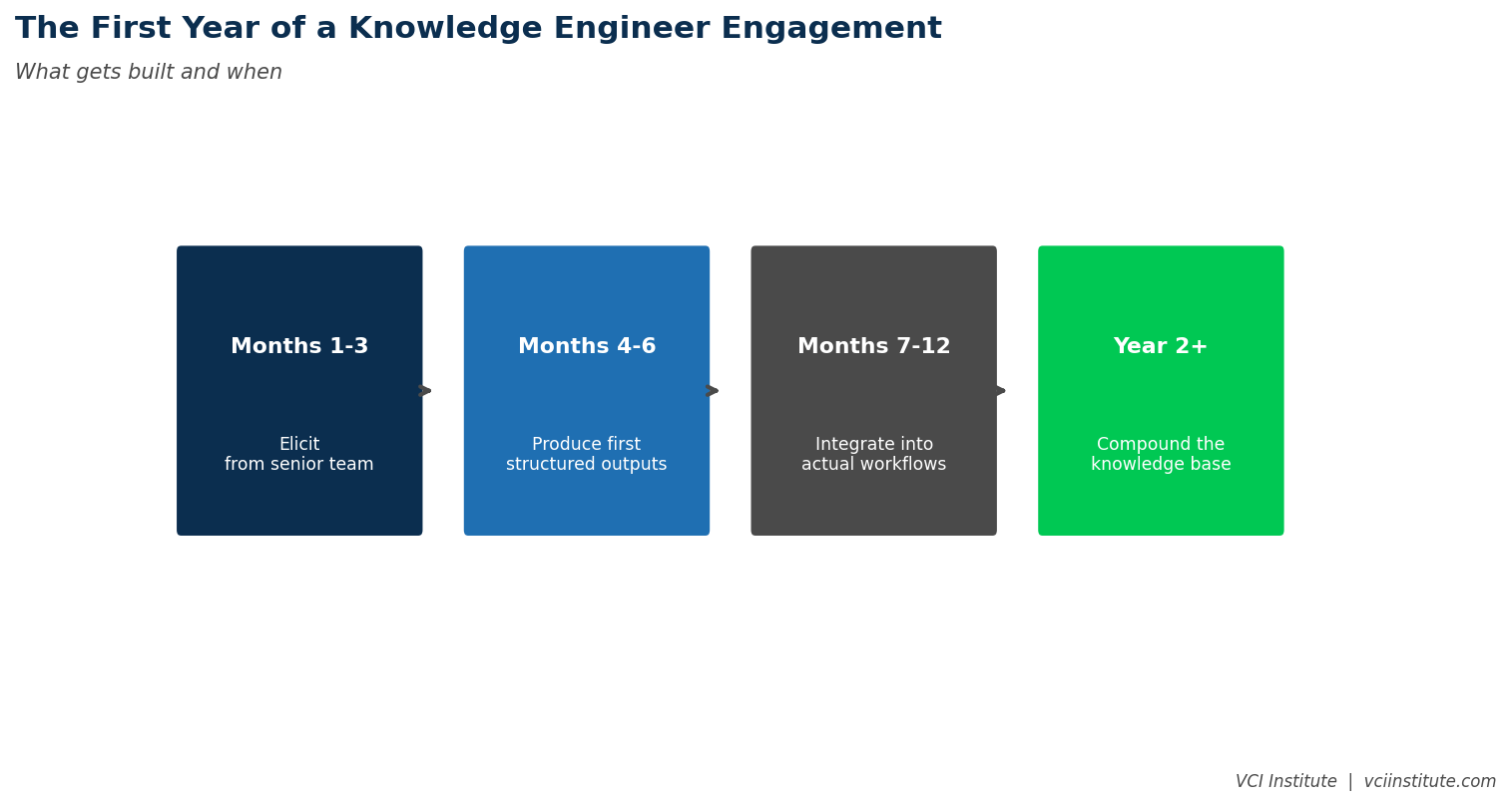

A knowledge engineer in the first year of a serious engagement will produce a recognizable foundation. The work is not glamorous and the output is not theatrical. The compounding starts in year two.

Months one through three. Sit with each senior partner and senior operating partner for structured conversations. Build relationships. Understand the firm's recent deals. Identify the natural starting point for elicitation, which is usually a recent deal or a recurring industry pattern that the partners are willing to discuss in detail.

Months four through six. Produce the first wave of structured outputs. A diligence pattern library for the firm's most common industry. A management assessment framework that captures what the firm has actually learned. A debrief protocol that the firm will use for future deals. These early outputs are imperfect and the senior partners will revise them. The revision is part of the process. The output exists now in a form the firm can work with.

Months seven through twelve. Integrate the structured outputs into actual workflows. Update the diligence checklist. Revise the IC memo template to include institutional pattern context. Build the debrief into the post-close cadence. By the end of the first year, the firm has begun to use its own institutional reasoning in a way it could not before. The compounding is starting.

Years two through five. The knowledge base deepens. New deals add new patterns. Old patterns get refined or retired as conditions change. The junior team members benefit from accumulated reasoning that the senior team would have had to deliver in person each time. The AI infrastructure has structured material to work against. The senior partners notice that they are not being asked the same questions over and over again, because the answers have been captured and made available.

Figure: 34c first year plan

Why Most Firms Have Not Hired the Role

The knowledge engineer is not a new idea. Gartner has identified it as an emerging role. Several Fortune 500 companies have hired versions of it. Consulting firms have made related investments. The pattern is recognizable. Yet almost no PE firm has hired it.

Three reasons explain the gap.

The first reason is that the value of the role is invisible in any single quarter. Senior partners do not feel the absence of the knowledge engineer because their tacit reasoning has always been their personal property. The cost of not having the role is paid by junior team members and by the next generation, not by the people who would approve the hire.

The second reason is that the role is unfamiliar. Senior partners who have not seen one work do not know what it should look like, who to hire, or how to integrate the role with their existing team. The unfamiliarity produces deferral. The deferral becomes the status quo.

The third reason is that the firms that have made the hire have done so quietly. There is no industry conference panel on the role. No prominent firm has been celebrated for hiring a knowledge engineer. The reputational return for being early is, for now, mostly internal. The firms that get this right will not be widely recognized for it. They will simply, three years from now, have institutional capability that their competitors lack.

The Strategic Position

The knowledge engineer is the role that translates the firm's most valuable asset, the accumulated reasoning of its senior people, into something the firm actually owns rather than something its senior people happen to carry around. Without the role, the asset cannot scale. With the role, the asset compounds.

For sponsors building or refining their firms over the next five years, hiring a knowledge engineer is one of the highest leverage moves available. The cost is modest. The visible output is unglamorous. The compounding advantage is real. The role does not require advanced AI investments to be valuable. It is, in fact, the prerequisite for AI investments to be valuable, because it produces the substrate that AI can amplify.

The first firms to make this hire seriously will, by the end of the decade, have built institutional knowledge bases that no competitor can replicate without doing the same work. The work takes years. Starting now produces a five year head start. Waiting another two years produces a five year deficit.

The job description is not yet standard. The hiring market is thin. The integration with existing teams takes care. None of these are reasons not to do it. They are reasons to do it before the rest of the industry recognizes what has been done.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.