The Shared Conviction Problem: Why Deal Theses and Value Creation Plans Drift Apart by Month Six

Apr 29, 2026

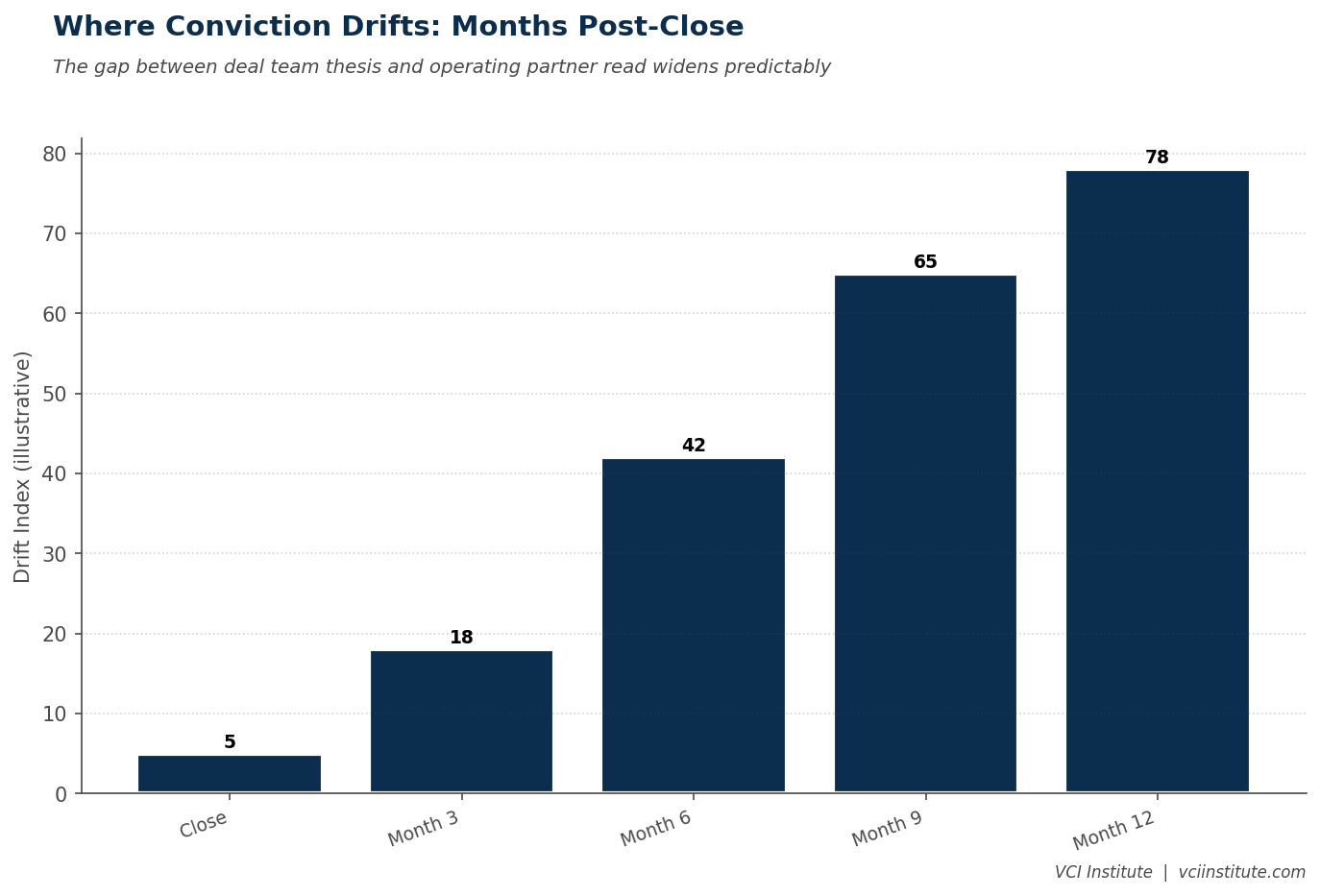

The diagnostic shows up the same way across deals. Six months after close, the operating partner and the deal team are working off subtly different plans. The deal team is still anchored to the thesis that cleared the investment committee. The operating partner has, through ninety days inside the business, developed a different read on what the actual value creation work has to be. Neither has formally said this. Both are working hard. The drift is real and growing.

By month nine, the difference has hardened into two parallel narratives about the same deal. The deal team's narrative tracks against the original thesis and emphasizes the levers the model assumed. The operating partner's narrative tracks against operational reality and emphasizes the levers the business actually requires. The board pack reflects whichever narrative dominates the room, with the management team caught between two senior groups who appear to be in alignment but are actually managing slightly different deals.

This is the shared conviction problem, and it is one of the most underdiscussed sources of value creation underperformance in private equity. The fix is structural, not interpersonal. Firms that have figured it out have built specific institutional practices that prevent the drift. Firms that have not figured it out continue to produce the drift across deals and explain the resulting underperformance through other lenses.

Figure: 36a drift pattern

Where the Drift Starts

The drift does not start at close. It starts before close, in the gap between when the deal team builds the thesis and when the operating partner has the chance to engage with the business in depth.

A typical deal cycle has the deal team in serious engagement with the target for eight to twelve weeks of intensive diligence. The thesis is built, refined, and approved during this window. The operating partner is, in many firms, brought in late, sometimes after the LOI is signed, sometimes only at the IC stage, and sometimes only after close. The thesis is presented to the operating partner as completed work. Her engagement with the underlying business begins after the document has been finalized.

This produces an asymmetric situation. The deal team has confidence in the thesis because they built it. The operating partner does not yet have grounds for confidence in the thesis because she has not yet engaged with the reality the thesis describes. She has two options at this stage. She can defer to the deal team's confidence and proceed with the plan as written, hoping the thesis is sound. Or she can express skepticism without yet having the operational depth to make the skepticism specific. Most operating partners choose the first option, because the second produces conflict with deal partners whose authority has approved the deal.

The deferral is the first crack in shared conviction. The operating partner does not actually share the deal team's confidence. She has chosen, for good political reasons, not to challenge it. The thesis goes forward with the appearance of alignment but without the substance.

What Closes the Gap and What Widens It

The first ninety days after close are when the operating partner finally has the chance to engage with the business at the depth the thesis was built on. What she finds shapes the trajectory of shared conviction for the rest of the hold.

When the thesis turns out to be substantially right, the operating partner's confidence catches up with the deal team's. Shared conviction emerges retroactively. The plan executes against an aligned view, and value creation proceeds as intended.

When the thesis turns out to be substantially wrong, the operating partner faces a difficult choice. She can renegotiate the plan with the deal team, which requires acknowledging that the IC-approved thesis was not entirely accurate. The deal partners do not enjoy this conversation. Or she can quietly execute against a modified plan that she believes will work, while letting the deal team and the board continue to report against the original thesis. The first option produces friction. The second option produces drift.

Most operating partners choose the second option, again for good political reasons. The friction of the first option is high. The drift of the second option is invisible at first. By the time the drift becomes visible, six to nine months have passed, and the cost of correcting the original plan has compounded.

The pattern is not the operating partner's fault. It is the structural consequence of bringing the operating partner in too late, with the thesis already approved, and without an explicit license to revise the plan based on post-close discovery.

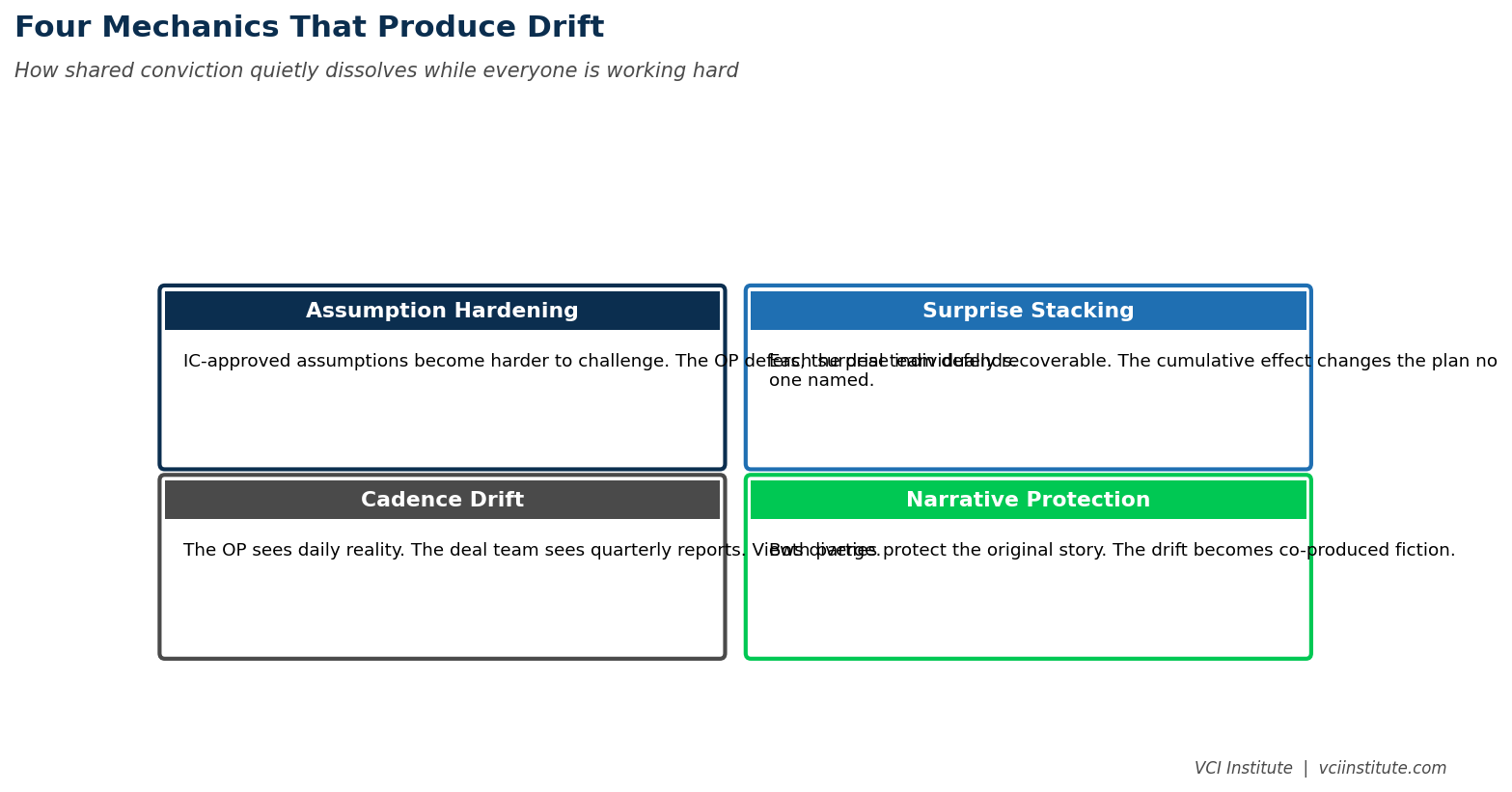

Figure: 36b drift mechanics

The Mechanics of Drift

The drift, once it starts, has predictable mechanics that recur across deals.

The first mechanic is the assumption hardening. The IC-approved thesis contains assumptions that, once approved, become harder to challenge. The cross-sell synergy that the model required. The pricing power the deal team underwrote. The talent depth the diligence assessed. Each of these is now part of the official narrative. Challenging any of them requires walking back something the IC approved. The deal team has reputational stakes in not walking it back. The operating partner has political stakes in not initiating the challenge.

The second mechanic is the surprise stacking. As the operating partner engages with the business, she encounters surprises. Each surprise individually is recoverable. The cumulative effect is a growing list of small adjustments that, taken together, materially change the plan. Because each surprise was small, none of them triggered a formal replan conversation. The unspoken plan has shifted. The official plan has not.

The third mechanic is the cadence drift. The deal team's engagement is intermittent and event-driven. Quarterly board meetings, capital calls, exit planning. The operating partner's engagement is continuous. The continuous engagement produces a more current and granular view than the intermittent engagement. The two views diverge gradually. The board pack becomes a translation exercise where the operating partner edits her continuous view down to fit the deal team's intermittent expectations. The translation loses fidelity.

The fourth mechanic is the narrative protection. As the divergence grows, both parties have incentives to avoid surfacing it. The deal team does not want to acknowledge that the original thesis was incomplete. The operating partner does not want to be seen as the bearer of bad news. Both parties present whatever can be presented as success. The narrative diverges further from the operational reality. The drift becomes, by month nine, a co-produced fiction that neither party can easily exit.

What Actually Closes the Drift

Firms that have figured out shared conviction have institutionalized three practices. None of them are revolutionary. All of them are unfamiliar enough that most firms have not implemented them.

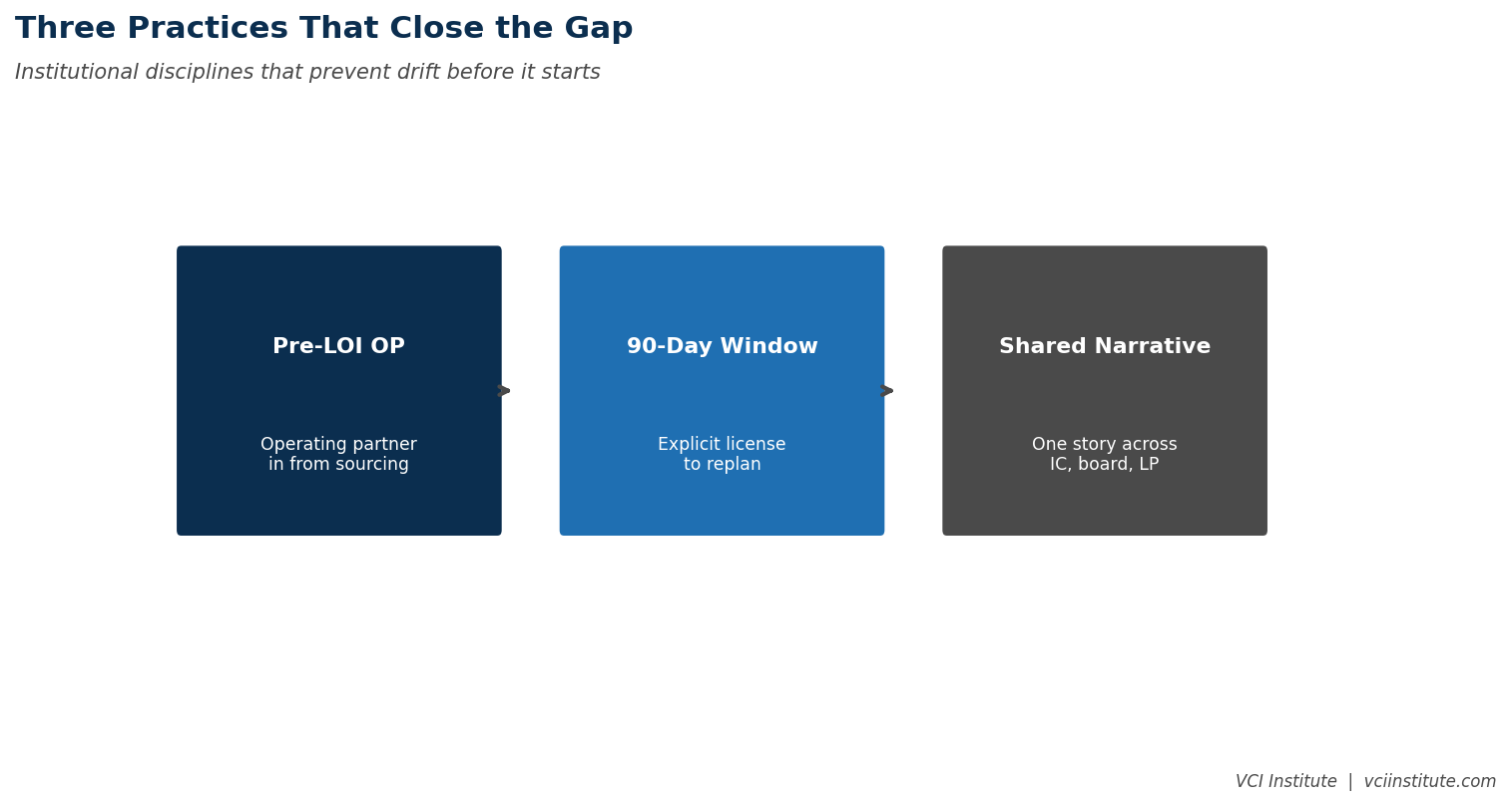

The first practice is pre-LOI operating partner engagement. The operating partner is part of the deal team from initial diligence forward, not brought in at the end. She has the chance to engage with the business while the thesis is being built rather than after it is finalized. Her concerns shape the thesis rather than challenging it later. Her confidence in the thesis is real because she contributed to it. Shared conviction starts before close because both parties built the same plan together.

This practice is harder than it sounds. It requires the deal team to give up some of the autonomy they have historically held over the thesis. It requires the operating partner to commit time to deals that may not close. It requires the firm to accept that diligence becomes longer and more demanding because the operating perspective is being integrated rather than added at the end. Firms that have made this commitment report better outcomes. Firms that have not have continued to produce the drift pattern.

The second practice is the post-close replan window. The first ninety days after close are explicitly designated as a period where the plan can be revised based on what the operating partner discovers in depth engagement with the business. The IC-approved thesis is treated as the starting hypothesis, not the final plan. The replan, when it happens, is approved through a defined process that allows for honest acknowledgment of what was not visible at close. The operating partner has explicit license to revise. The deal team has explicit obligation to engage with the revisions seriously rather than defending the original.

This practice requires cultural commitments that most firms have not made. Deal partners have to accept that the thesis they built may not survive contact with the business in detail. The IC has to be willing to receive replan presentations as part of normal portfolio governance rather than as confessions of error. Operating partners have to be willing to do the work of producing a credible replan rather than executing against a plan they privately doubt.

The third practice is the explicit shared narrative. The board pack, the LP report, and the internal portfolio reviews all reflect a single narrative that both the deal team and the operating partner have signed off on. When the narrative changes, both teams change it together. There are not two narratives running in parallel.

This practice requires governance discipline. The temptation to allow the deal team and the operating partner to each present their own version of the deal to their respective audiences is real. The cost of allowing it is the ongoing drift. Firms that insist on a single shared narrative produce alignment that lasts. Firms that allow parallel narratives produce drift that compounds.

Figure: 36c alignment practice

The Mid-Month-Six Conversation

Even with the three practices in place, individual deals will sometimes drift. The institutional practice that catches drift early is the structured mid-month-six conversation between the deal team and the operating partner, separate from the board meeting and separate from the management team.

The conversation has one job. It surfaces, honestly, where the deal team's view and the operating partner's view of the deal have diverged in the past sixty days. Each side names what they have come to believe that may differ from what they believed at close. The differences are documented. The implications for the plan are discussed. If a replan is warranted, it is initiated through the formal process. If the differences are reconcilable through clarification, they are clarified.

This conversation takes about ninety minutes. It is uncomfortable. It produces honest engagement with the drift before the drift becomes the deal's defining feature. Firms that have built this conversation into their cadence find that the drift becomes manageable. Firms that have not find that the drift becomes the deal.

The Compounding Cost

The cost of the shared conviction problem compounds across the portfolio in ways that are not captured in any single deal's analysis. Every deal that drifts produces a small underperformance attributable to the drift. The underperformance is rarely large enough to be a disaster. It is large enough, in aggregate across the fund, to be visible in performance metrics.

LPs evaluating sponsor performance increasingly recognize this pattern, even when they cannot articulate it in the language used here. They notice that some firms produce consistent execution against thesis and others produce a pattern of stories about why the original thesis turned out to be more nuanced than expected. The first kind of firm builds a track record that supports the next fundraise. The second kind of firm builds a track record that requires explanation.

The fix is not new diligence frameworks or better models. The fix is structural alignment between the two trades that have to work together to make value creation actually happen. Firms that have built the alignment have an advantage. Firms that have not have a problem they have not yet named, which is the kind of problem that compounds quietly and shows up at fundraise time as a pattern that LPs find harder to commit to. The shared conviction problem is solvable. The solution is institutional discipline, not individual heroics. The sponsors that build the discipline early will be operating with shared conviction in three years, while their competitors are still drifting through deals and wondering why the plans they presented at IC are not the plans they ended up executing.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.