The Wrong CEO Hire: Why Sponsors Make the Same Mistake Every Three Years

May 31, 2026

___

Talk to any operating partner who has been in private equity for more than ten years and ask about CEO hires. The conversation will produce a list of mistakes. Almost every senior practitioner has hired the wrong CEO at least once, often more than once. The mistakes are not random. They cluster around a small set of recurring patterns that practitioners can name in retrospect but rarely seem able to avoid prospectively.

This is the strange feature of the CEO hiring process in private equity. The mistakes are knowable. They are documented in the after-action reviews that rarely happen and in the casual conversations between practitioners that happen all the time. The patterns repeat across firms, across sectors, and across vintages. And yet, the same firms that learned what to avoid two CEO searches ago somehow find themselves making variations of the same mistake again.

The recurrence is not a competence problem. It is a structural problem. The pressures and incentives in a typical CEO search push sponsors toward the predictable failure patterns even when the senior team knows the patterns well. Understanding the structural pressures is the first step toward making better decisions, not by being smarter, but by acknowledging the conditions under which smart people make recurring mistakes.

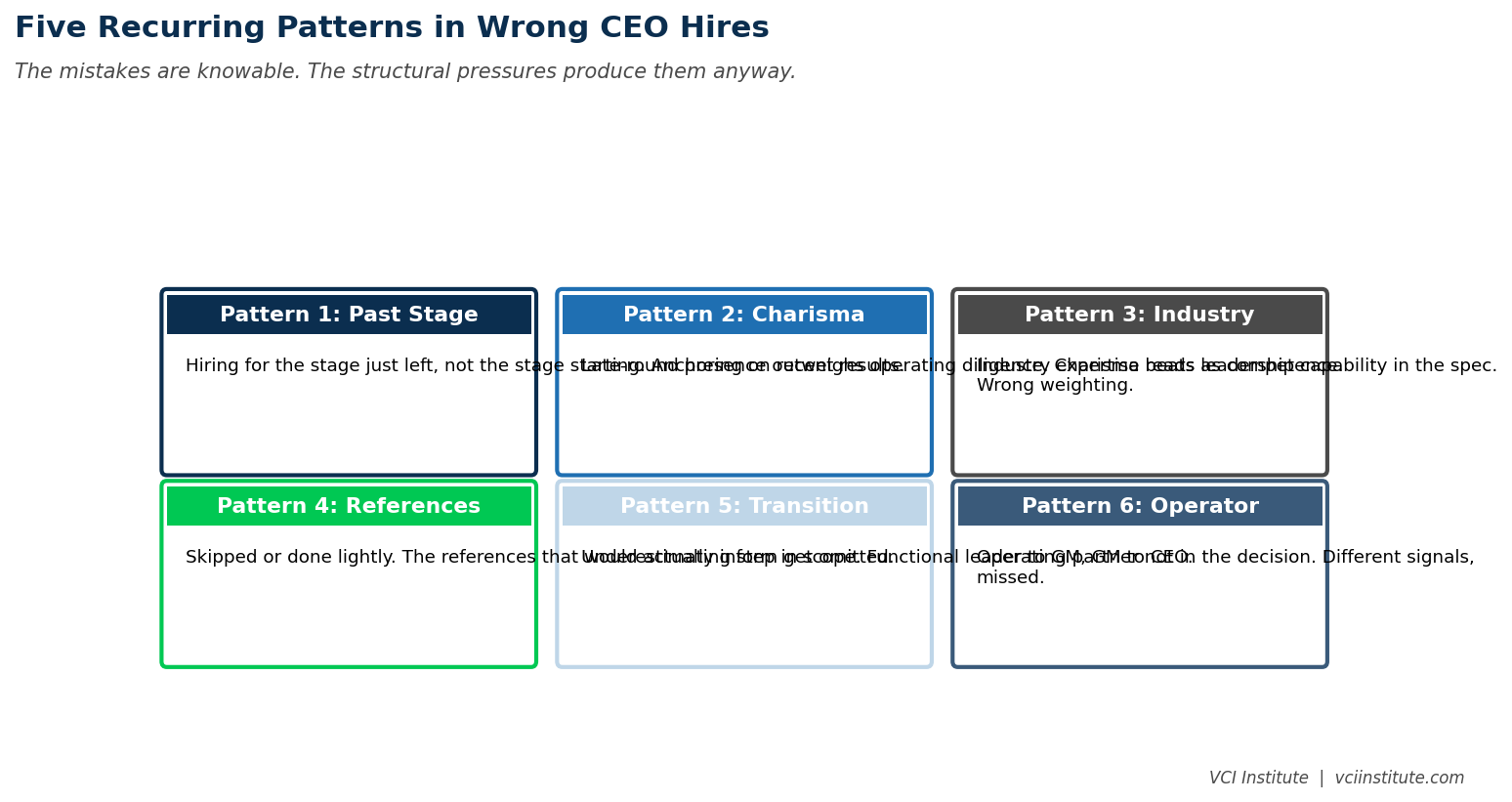

Pattern One: Hiring for the Stage You Just Left

The most common pattern is hiring a CEO who would have been right for the stage of the business that just ended, rather than the stage that is starting. The fifty million revenue business that has scaled to one hundred and fifty million needs a different CEO than the founder who built it from twenty to fifty. The CEO who took the business from one hundred to two hundred fifty may not be the right CEO to take it from two hundred fifty to five hundred. The skills that produced success at one stage are not the skills that produce success at the next.

The structural pressure here is that the search process anchors on the immediate past. The board reads recent results. The reference checks emphasize what was just delivered. The interview process surfaces stories from the most recent successful chapter. The candidate who fits the immediate past most cleanly is the candidate who feels most credible. The candidate who fits the next chapter, which has not happened yet, is harder to evaluate because the evidence does not yet exist.

The fix is to be explicit about which stage the business is entering rather than which stage it just left, and to weight the evaluation toward fit with the future stage. This requires the search committee to articulate, in writing, what the next eighteen to thirty-six months will require of the CEO. The articulation is uncomfortable because it forces specificity. The discipline of producing it is what prevents the default toward hiring for the past.

Pattern Two: Falling for Charisma in the Final Round

The second pattern is the late-stage charisma trap. The search has narrowed to two or three finalists. The board has met them all. One of them has more presence in the room than the others. The discussion shifts subtly. The candidate who was strongest on the operating fundamentals has weaker stage presence. The candidate with stronger presence has gaps in the operating profile. The decision tilts toward the charismatic candidate. The board members who participated convince themselves that the charisma will translate into operational results. It often does not.

The structural pressure is that final-round selection happens in rooms where charisma reads as competence. The senior partners are pattern-matching to the question of whether they would be comfortable putting this person in front of customers, employees, and lenders. The answer is mostly about presence. The actual question of whether the person can run the business at scale is harder to evaluate in the same room. The room rewards the easier evaluation.

The fix is to do the operating diligence on finalists with rigor that exceeds what is comfortable. Reference calls that go deep on specific situations the candidate handled. Working sessions that test how the candidate thinks through actual operational problems. Time spent with the candidate's former direct reports, who know what it was actually like to work for the person beyond the public version. This work is uncomfortable to push for in a competitive search, where candidates have other options. It is also what distinguishes the searches that produce strong outcomes from those that produce charismatic disappointments.

Pattern Three: The Industry Expert Who Cannot Lead

The third pattern is over-weighting industry expertise relative to leadership capability. The thinking is reasonable on its face. The business is in a specific industry. A CEO who knows the industry will move faster, avoid rookie mistakes, and bring relationships that accelerate execution. The logic is real. It is also incomplete.

What the industry expertise framing misses is that running a business is, mostly, leadership work. Building and managing a team. Setting and communicating priorities. Making consequential decisions under uncertainty. Holding people accountable. Driving change. Industry expertise is helpful, sometimes substantially helpful, but it is not the binding constraint in most CEO situations. The binding constraint is leadership capability.

When firms over-weight industry expertise, they end up with CEOs who know the industry well but cannot build a team, cannot drive accountability, and cannot make difficult decisions cleanly. The industry knowledge does not compensate for the leadership gap. The business operates with strong industry context and weak operational tempo, which is not a winning combination at scale.

The fix is to weight leadership capability above industry expertise in most situations, with industry expertise as a tiebreaker among candidates who clear the leadership bar rather than as the primary criterion. Most industries can be learned by a strong leader within twelve to eighteen months. Leadership cannot be learned in the same window by someone who has not built it. The fix is uncomfortable because it requires evaluating leadership at a level of depth that most search processes do not produce.

Pattern Four: Skipping the Reference Calls

The fourth pattern is the most embarrassing because it is the easiest to fix and the most consistently neglected. Reference calls done well, with people who actually worked for or with the candidate, in situations that matter, produce information that nothing else in the search process produces. Reference calls done badly, or skipped, allow candidates to be evaluated mostly on their own self-presentation.

The structural pressure is that reference calls are time consuming. They require effort to schedule, candor to extract, and patience to assess. In competitive searches with timeline pressure, the temptation is to do reference calls late, lightly, and with insufficient depth. The references that get done are often the ones the candidate suggested, who are pre-selected to be supportive. The references that would actually inform the decision are the ones that require the searcher to develop independently, which takes work.

The fix is to do reference calls early, broadly, and beyond the candidate's suggested list. To go deep on specific situations rather than asking general questions. To ask former direct reports, not just former bosses. To probe for what the candidate did when things went wrong, not just what they did when things went right. The reference work that produces real information is the reference work that gets done. Most searches do not do enough of it.

Pattern Five: Underestimating the Transition

The fifth pattern is underestimating what it takes to transition from functional leader to general manager, or from general manager to CEO. The capable CFO who is being elevated to CEO. The strong divisional president becoming the parent company CEO. The successful operator at one company being recruited to lead a different one. Each of these transitions involves a real step in scope, in accountability, and in the kinds of decisions that have to be made.

Many candidates who clear the transition do so with substantial difficulty. Many candidates who do not clear it have not signaled the limits of their range during the search process. The structural pressure here is that the transition itself is hard to assess in advance. The candidate has not done this exact role before. The reference checks describe what the candidate has done. The interviews probe how the candidate would handle the new role, but the candidate's answers are necessarily speculative.

The fix is to give weight to candidates who have made similar transitions before, even if at smaller scale, and to weight against candidates whose entire career has been within a single scope. A candidate who has run a fifty-person organization and grown it to two hundred has demonstrated the capacity to scale. A candidate who has only run a stable two-hundred-person organization has not. The distinction matters, even when both candidates look similar on paper.

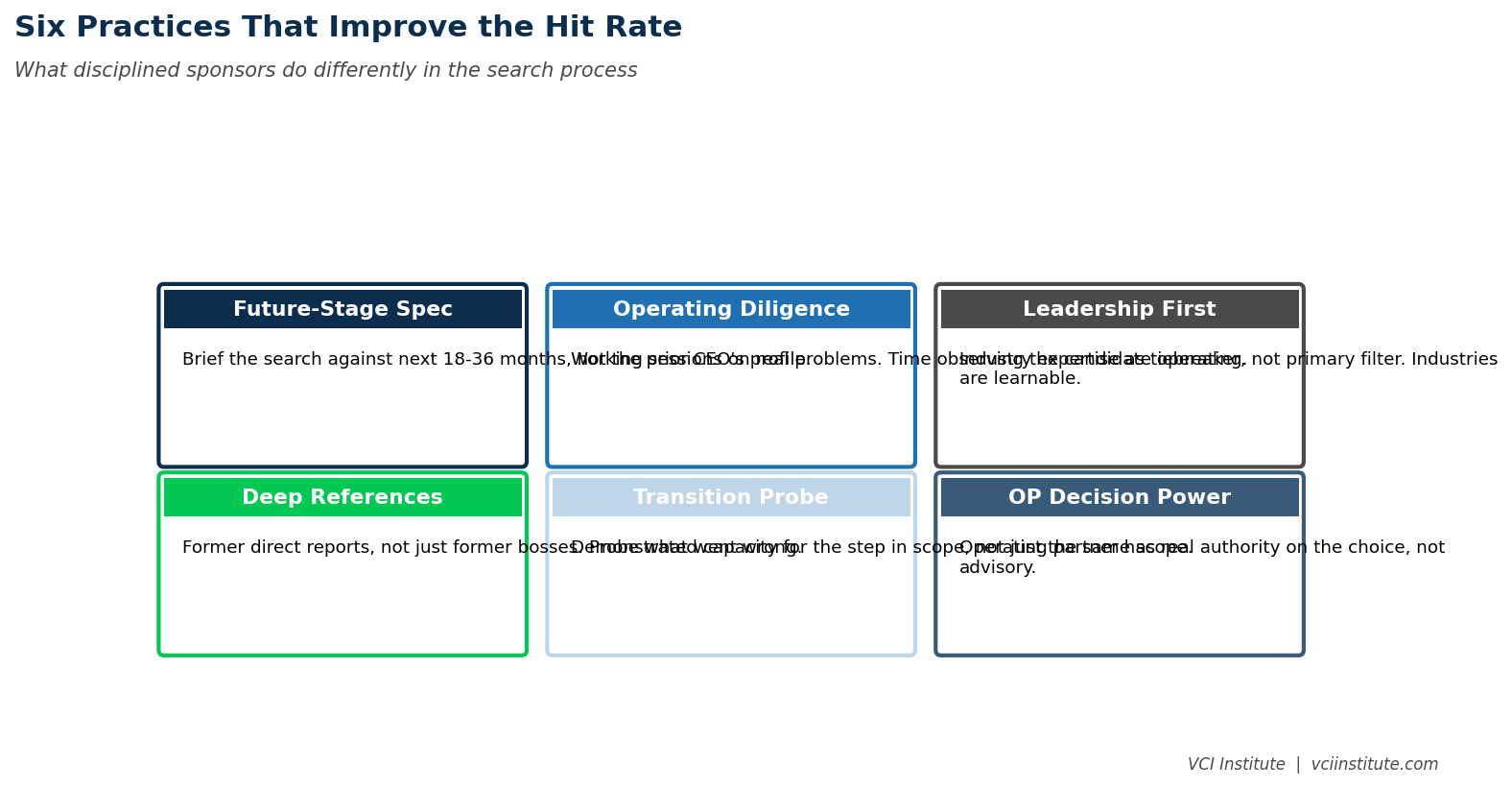

What Disciplined Sponsors Do Differently

The sponsors that make better CEO hires more consistently share recognizable practices that address the structural pressures rather than relying on individual judgment alone.

They write the spec for the next stage, not the past one. The brief for the search is explicit about what the business needs over the next eighteen to thirty-six months. Candidates are evaluated against the brief, not against the prior CEO's profile.

They do operating diligence with rigor on finalists. Working sessions on actual business problems. Deep reference calls with former direct reports. Time observing the candidate in operating situations rather than only in interview settings.

They weight leadership above industry expertise as a default. Industry expertise is a plus, not the primary filter. The candidate who can build a team, drive accountability, and make hard decisions is the candidate who runs the business well. Industry context is learnable. Leadership is not.

They build reference calls into the search early and broadly. The reference work is started before final-round interviews, not after. The references include former direct reports, peers, and people who saw the candidate during difficult periods, not just supportive bosses.

They probe the transition explicitly. The interview process tests whether the candidate has demonstrated the capacity for the step in scope that the role requires. The candidates who have made similar transitions before are weighted favorably. The candidates whose careers have been within a single scope are evaluated more cautiously.

They include the operating partner in the decision. The operating partner who will work with the CEO has a real say in the choice, not just an advisory role. The operating partner has different signals than the deal team and a different stake in the outcome. Including her view changes the decision.

These practices do not guarantee good outcomes. They produce a higher hit rate than the default process. The hit rate matters because the cost of a wrong CEO hire is roughly two years of value creation work, plus the disruption of replacing the person, plus the management team's loss of confidence in the sponsor's hiring discipline.

The Honest Test

The most useful exercise a sponsor can run on its CEO hiring process is to look back at the last five CEO hires across the portfolio and ask, honestly, which of the five recurring patterns each one fell into. The exercise is uncomfortable because the answers usually include hires that did not work out. The discomfort is the value. The patterns that show up are the patterns that will show up in the next search if the institutional discipline does not change.

The CEO hire is the single most consequential talent decision sponsors make in any given portfolio company. Getting it right at a higher rate is one of the highest leverage capabilities a firm can develop. The firms that have built the discipline produce hire rates that compound in their favor over fund cycles. The firms that have not produce a recurring tax on their portfolios that nobody quite measures but that LPs eventually feel in performance dispersion.

The patterns are knowable. The pressures that produce them are recognizable. The discipline to operate against them is buildable. The first step is being honest about how often the firm has fallen into them in the past. The second step is changing the process so that the next search does not produce the same outcomes. The choice is available. The cost of not making it is, every three years or so, another CEO hire that the firm wishes it had handled differently.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.