Designing the AI System a Mid-Market PE Firm Actually Needs

Apr 29, 2026

The most expensive sentence in private equity right now is, what is your AI strategy. Not because the question is wrong, but because the answer almost always describes a stack of vendor tools rather than a system. A copilot for the deal team. A document summarizer for diligence. A dashboard layer for portfolio monitoring. A pricing engine for one of the portfolio companies. Each tool has a contract, a project plan, and a sponsor inside the firm who owns it. None of them connect.

Six months later, the firm has spent meaningfully more on AI than it did the year before, and the senior partners cannot point to a single decision they made differently because of any of it. The tools are running. The decisions are not informed by them. The system, which was supposed to be the point, was never actually built.

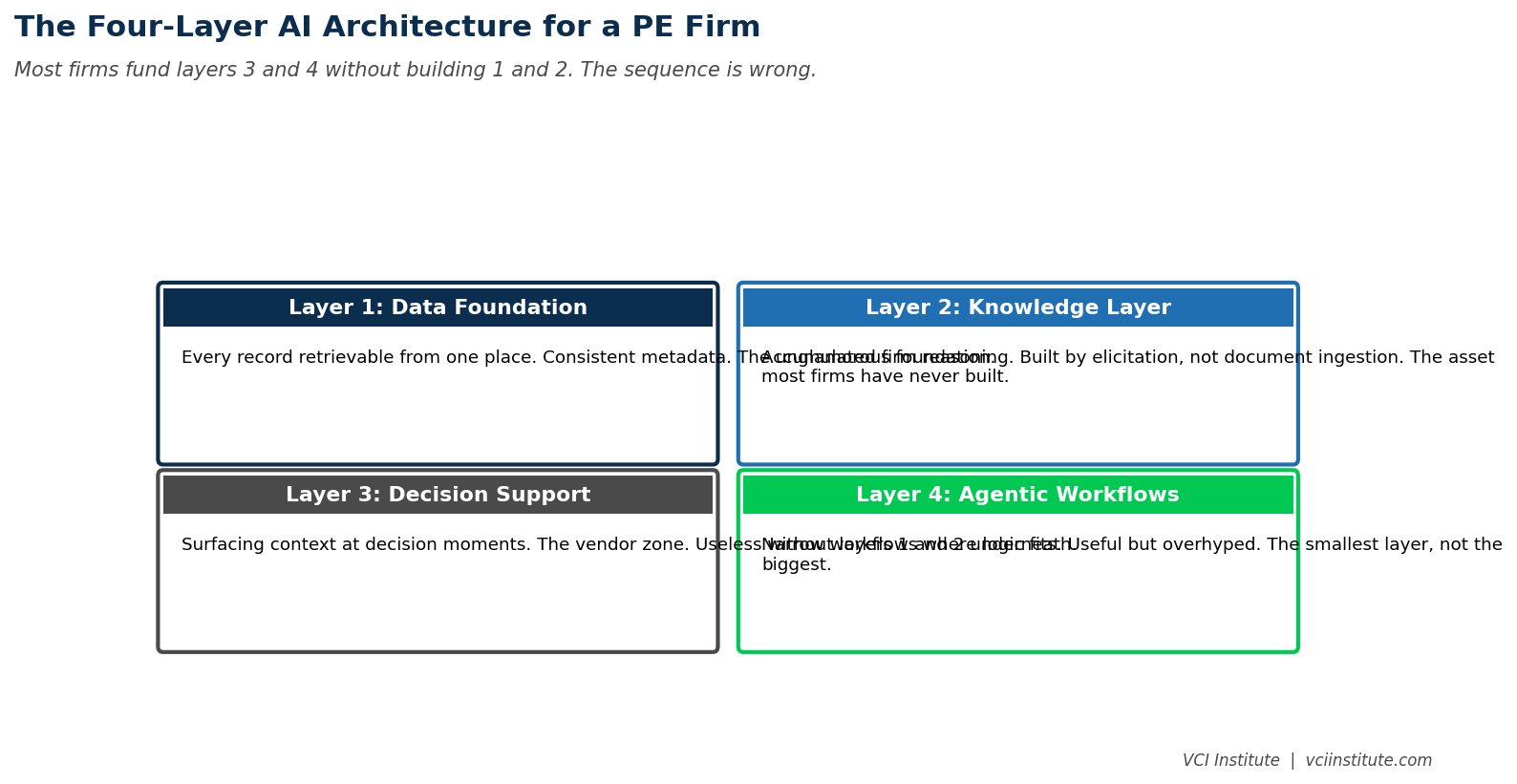

This is the pattern in 2026, and it is fixable. What it requires is to stop thinking about AI as a procurement question and start thinking about it as an architecture question. The architecture is not complicated. It has four layers. Most firms have funded layers two and three without building layer one, which is why nothing connects.

Figure: 31a four layer stack

The Four Layers

The first layer is the data foundation. Everything the firm knows. Deal pipeline records. Diligence files. Portfolio company financials. Board materials. LP correspondence. Operating partner notes. Investment committee memos. Most of this exists in a sprawl of email, SharePoint, deal management platforms, and individual hard drives. The first job is to get it into one place, with consistent metadata, accessible to a retrieval layer that can find what is in it. This is unglamorous work. It is also the work without which nothing else functions.

The second layer is the knowledge layer. The accumulated reasoning of the firm. How senior partners have evaluated specific industries, specific deal patterns, specific management teams over the past decade. What the firm has learned from its successes and its failures. The patterns that recur across portfolios. This layer cannot be built by ingesting documents alone. It requires deliberate elicitation from the people who hold the knowledge, structured into a form a system can use, and refreshed as the firm learns more. This is the layer almost no firm has built seriously yet.

The third layer is the decision support layer. The interfaces that surface the right data and the right reasoning at the moment of decision. Pre-LOI screens that pull comparable deal patterns from the knowledge layer. Diligence dashboards that synthesize findings against historical pattern. Portfolio monitoring that flags drift before it becomes visible to management. Exit readiness scoring that integrates operational and financial signals. This is where vendors mostly play, and where most firms have spent their AI budget.

The fourth layer is the agentic layer. Workflows that take actions, not just provide information. Drafting initial diligence requests. Maintaining CRM hygiene. Producing first drafts of board materials. Routing investor inquiries. The agentic layer is real but its productive scope is narrower than the marketing suggests. It works inside structured workflows where the human review point is preserved. Outside those conditions, it produces problems faster than it solves them.

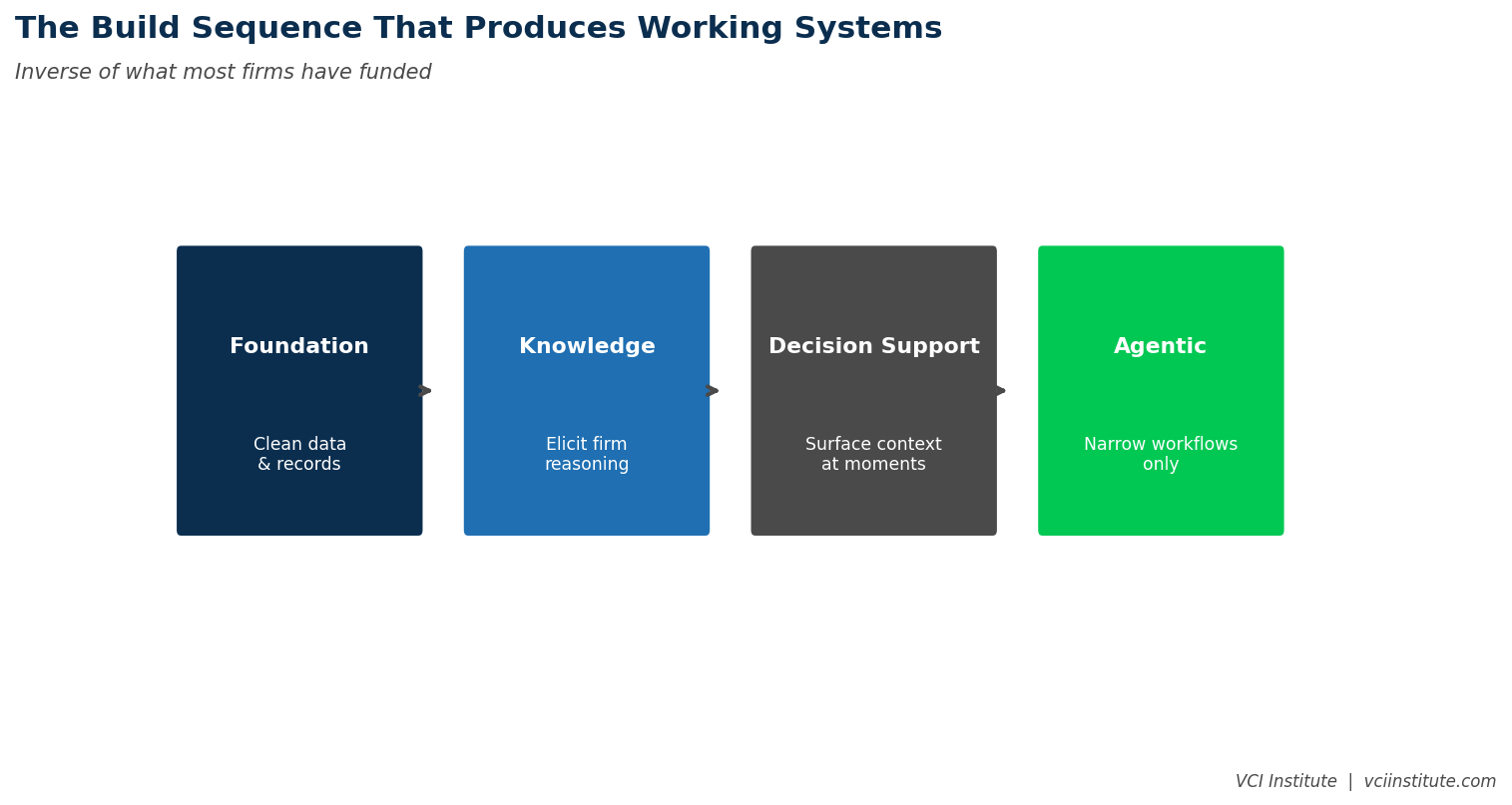

Figure: 31b sequencing roadmap

Why the Sequence Matters

Most firms have funded layers three and four without building layers one and two. The result is decision support running on incomplete data and agentic workflows running on undocumented rules. The tools are powerful. The foundation is missing. The output looks confident because the interfaces are clean. The output is unreliable because the underlying inputs are patchy.

The sequence that produces working systems is the inverse of the sequence most firms have followed. Build layer one first. Make every important document, record, and metric retrievable from a single source, with consistent definitions and clear ownership. Build layer two second, by structured elicitation from the partners and operating leaders who hold the firm's accumulated reasoning. Only then build layer three, the decision support, against a foundation that can actually support it. Reserve layer four for narrowly defined workflows where the agentic logic genuinely fits.

Firms that follow this sequence find that their decision support tools work the first time. Firms that follow the inverse sequence, which most do, find that their decision support tools have to be redesigned every time the underlying data foundation shifts, and that adoption is structurally weak because the outputs do not survive scrutiny.

The Specific System a Mid-Market Firm Should Build

The architecture in the abstract is too generic to act on. Translated to a mid-market PE firm, the system has six concrete components.

A unified deal repository. Every deal the firm has looked at, with structured metadata on industry, size, owner, valuation, outcome, and the reason it was passed or pursued. Pulled from the deal management platform, enriched with notes from the deal team, and refreshed continuously. This is the institutional memory that lets the firm see patterns across years rather than relying on whoever happens to remember.

A diligence pattern library. The recurring questions, findings, and red flags that have shown up in the firm's diligence work, organized by industry and deal type. Built from past diligence files, structured by knowledge engineers in collaboration with senior partners, accessible to junior team members during live diligence. This compresses the gap between the experienced partner's pattern recognition and the analyst's first pass.

A portfolio operating dashboard. Standard operating metrics across portfolio companies, defined consistently, refreshed weekly, surfaced to the operating partner team before each portfolio company review. This is the speed-to-insight layer that the typical monthly board cycle does not provide.

A management team assessment archive. Every senior leader the firm has worked with, structured by what worked, what did not, and what the assessment turned out to predict. This is the basis for not making the same hiring mistake every three years.

An exit pattern engine. The firm's accumulated experience with exits, structured by what worked, what dragged, and what the leading indicators were eighteen months out. This is the basis for exit readiness work that starts at the right time rather than the urgent one.

An LP communication layer. Investor inquiries, recurring questions, and the firm's own evolving narrative. This is the basis for fundraising and ongoing LP relationships running on consistent rather than reinvented messaging.

These six components together constitute the system a mid-market firm needs. None of them require AI vendors that did not exist three years ago. All of them require institutional discipline that most firms have not yet put in place.

Figure: 31c build vs buy

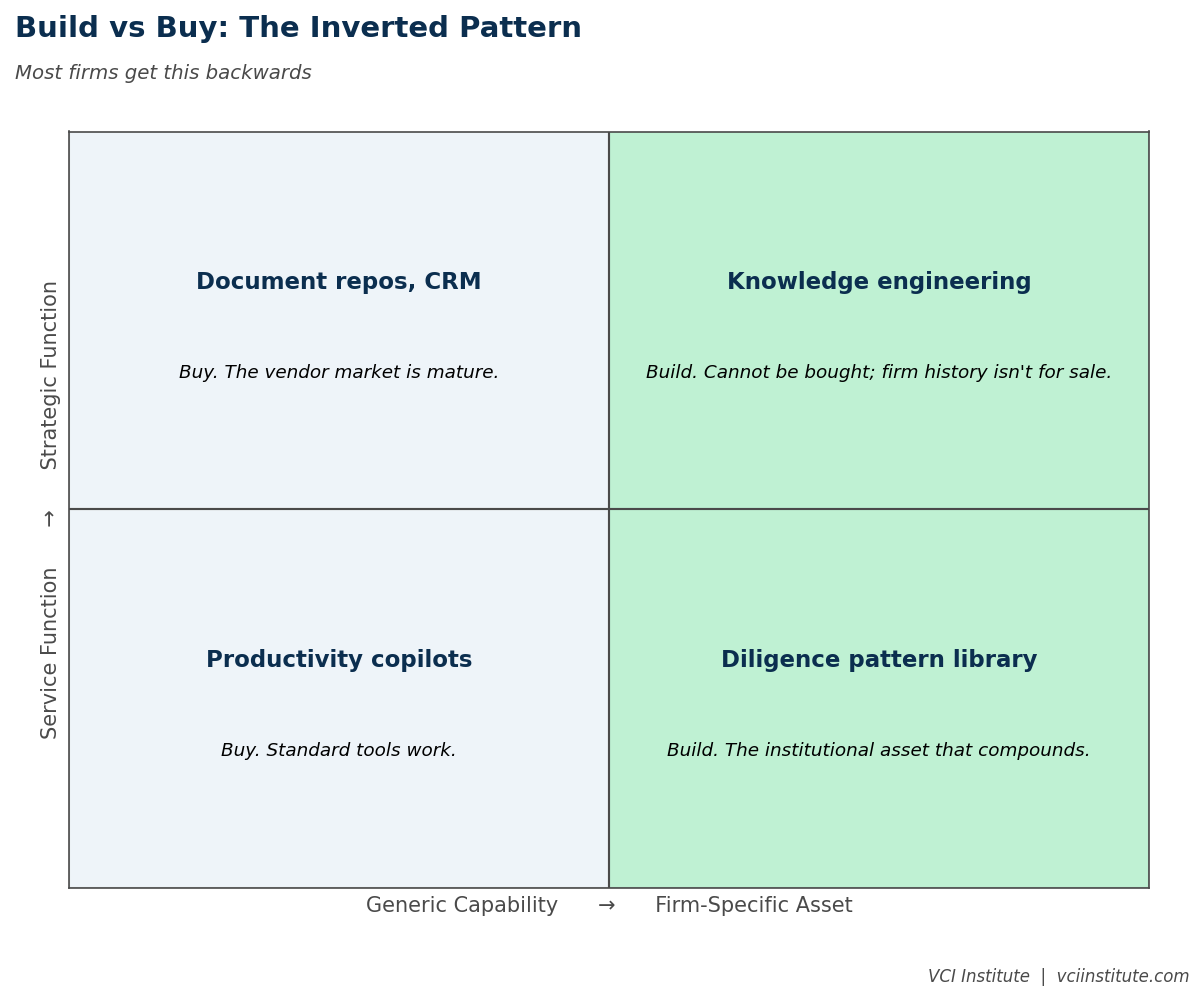

Build Versus Buy

The build versus buy question is genuine and the answer is mixed. Some components are better bought, because the vendor market has produced credible products and the firm's specific data does not require custom infrastructure. Document repositories. Standard CRM functionality. Generic copilot tools for productivity work.

Other components are better built, because the value comes from the firm's specific accumulated reasoning rather than from generic capability. The diligence pattern library, the management team assessment archive, the exit pattern engine. These cannot be bought because the asset that makes them valuable, the firm's history, is not for sale.

Most firms get this backwards. They build their own document repositories because that feels customizable, while buying their decision support layers from vendors who do not have access to the firm's institutional reasoning. The result is generic decision support running on bespoke infrastructure. The right pattern is the inverse. Buy the infrastructure, build the institutional asset.

What Operating Partners Should Press For

Operating partners are usually well positioned to influence the AI architecture conversation, because they sit at the intersection of fund operations and portfolio company operations. Three asks are worth pressing for in any firm that is investing seriously in AI.

The first ask is to build layer one before funding layer three. Make the foundational data and document infrastructure work before adding decision support tools that depend on it. This is unglamorous and unpopular. It is also the only way the rest of the stack pays back.

The second ask is to identify a knowledge engineer or knowledge management lead, even if part time at first. Someone whose explicit job is to extract the firm's tacit reasoning into structured form. Without this person, layer two never gets built and the rest of the system runs on whatever happens to be in documents.

The third ask is to define what success looks like in operating terms, not in tool deployment terms. The success metric is not how many AI tools are running. The success metric is what decisions the firm now makes differently because of the system. If the senior partners cannot name the decisions, the system is not yet working, regardless of how much has been spent.

The Compounding Edge

Firms that build layer one and layer two will, in three to five years, have a system that compounds. New deals get evaluated against a richer pattern library every quarter. Diligence becomes faster and more thorough as the pattern library deepens. Portfolio monitoring becomes more predictive as more cycles of data accumulate. Exit timing becomes more disciplined as exit pattern recognition matures. The system gets better with use.

Firms that fund layer three and layer four without the foundation will, in the same three to five years, have spent comparable amounts and produced a stack of tools that are individually useful and collectively disconnected. Their senior partners will still be operating from personal pattern recognition, augmented by occasional reports from the AI tools. The institutional memory will still live in the heads of the people who happen to have it.

The difference at year five is not subtle. It is the difference between a firm that has built genuine institutional capability and a firm that has paid for software. Both have invested. One has compounded. One has not.

The blueprint is not exotic. The discipline to follow it, in the right order, against the cultural pull of vendor-driven roadmaps, is the part that most firms still get wrong. The firms that get it right will, by the end of this decade, be operating at a level their competitors will find difficult to match. The architecture is the asset. The tools are the surface.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.