NAV Lending Reconsidered: A Tool That Solves One Problem and Creates Another

Jul 16, 2026

NAV lending has moved from niche financial product to standard liquidity infrastructure inside private equity in less than five years. Most established sponsors now have at least one NAV facility on their books. Many have several. The product is being marketed aggressively by specialty lenders, supported quietly by the GPs that use it, and discussed cautiously by the LPs that have to evaluate what it means for their exposure.

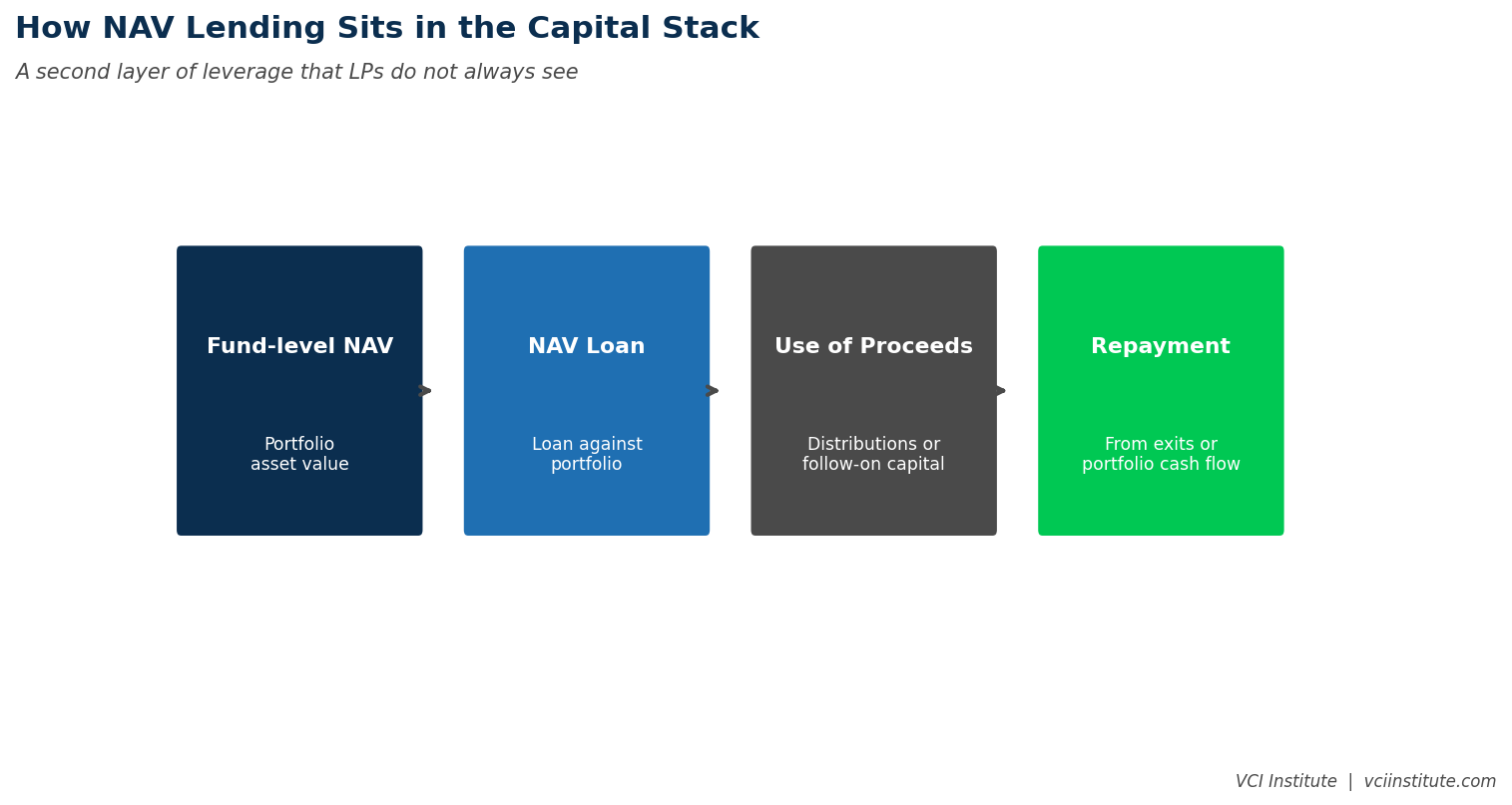

The basic structure is straightforward. A fund borrows against the aggregate net asset value of its portfolio. The borrowing is collateralized by the equity stakes the fund holds. The proceeds are used to make distributions to LPs, fund follow-on investments in existing portfolio companies, or finance bolt-on acquisitions. The interest is paid from portfolio company distributions or, more commonly, from eventual exit proceeds.

The product solves a real problem. Exit windows have lengthened. DPI has weakened. LPs are demanding distributions, sometimes urgently. Sponsors with high quality portfolios that are not yet ready for sale need a way to return capital without selling at a discount. NAV lending fills this gap.

It also creates a problem. The borrowing layers leverage on top of leverage. The portfolio companies are already leveraged at the operating company level. The fund now adds leverage at the fund level, secured against the same assets. The aggregate exposure to a downturn or an operational disappointment is materially larger than the operating leverage alone would suggest. And the LPs whose distributions are funded by this borrowing are, in some cases, not fully aware of what is being layered onto their economic exposure.

What NAV Lending Is Solving

The honest case for NAV lending is rooted in a real shift in the private equity market. Hold periods have stretched well beyond the traditional five to seven year window. The 2020 to 2022 vintage funds are now eighteen to forty-eight months past the point where their predecessors would have been distributing meaningful capital, and DPI metrics across the industry are weak. LPs that planned their portfolios around predictable distribution patterns have found themselves capital starved at exactly the moment they need to fund commitments to other funds.

In this environment, sponsors that hold high quality assets but cannot sell them at attractive prices face a real dilemma. Selling now means accepting valuations that do not reflect what the assets are worth. Waiting means continuing to disappoint LPs on the distribution metric. NAV lending offers a third option. Borrow against the asset value, return capital to LPs, and wait for the exit market to recover before selling.

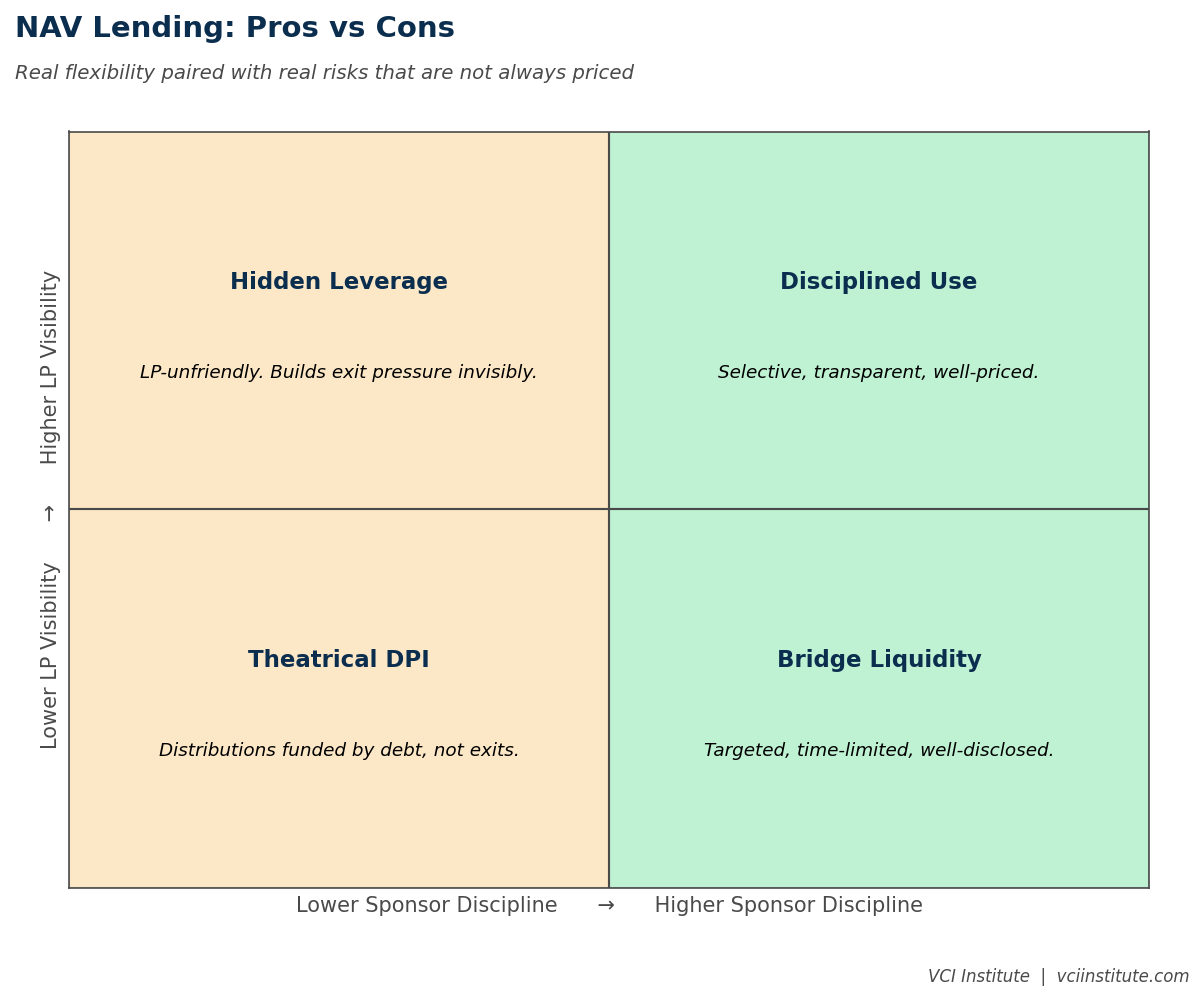

When used judiciously, the product can be defended. A fund with five strong portfolio companies, a clear path to exits within two to three years, and modest fund level borrowing that augments interim distributions is using NAV lending in a way that creates LP value rather than destroying it. The interest cost is modest relative to the eventual exit proceeds. The LP receives capital sooner. The sponsor gets to wait for the right exit timing.

This is the case the lenders make in their pitches and the case some GPs make to their LP advisory committees. It is a real case in some situations.

What NAV Lending Is Hiding

The harder case is what NAV lending is hiding when it is used less judiciously. Three patterns are showing up across portfolios in 2026 that LPs should be paying attention to.

The first pattern is the use of NAV lending to manufacture DPI in funds that are not actually performing. A fund with several underperforming portfolio companies, a weak exit pipeline, and pressure from LPs to demonstrate distributions can use NAV lending to produce DPI numbers that look acceptable for the next fundraise. The LPs receive cash. The headline DPI metric improves. The underlying portfolio quality has not changed. The borrowing has been added on top of operating leverage that is already stretched. When the eventual exits happen, the lender gets paid first, and the LPs find that their economic share of the portfolio's value is meaningfully smaller than they understood.

The second pattern is the use of NAV lending to fund follow-on investments in struggling portfolio companies. The borrowing covers the cost of additional capital injections that the fund should not be making in the first place but cannot avoid making to protect its investment. The follow-on capital is essentially financed by leverage layered on top of the existing leverage in the portfolio company. If the company recovers, the eventual exit pays back both. If the company does not recover, the fund's eventual loss is amplified, and the LPs absorb a larger negative outcome than the operating leverage alone would have produced.

The third pattern is the use of NAV lending to finance bolt-on acquisitions late in the hold period of a platform investment. The acquisition would be sensible if it could be funded from operating cash flow or from a fresh equity round. It is being financed instead by NAV borrowing because the timing pressure to demonstrate growth before exit makes other financing unattractive. The acquisition adds visible scale and revenue to the platform but adds leverage that the eventual buyer will see clearly. Exit proceeds are pressured by the additional debt. The platform that looked larger at exit produces less LP value than a smaller, less leveraged version would have produced.

The Disclosure Question

The deepest question about NAV lending is not whether it is a good product. It is whether the LPs whose capital is the ultimate exposure understand the leverage structure, the cost, and the implications for their economic outcome.

The honest assessment is that disclosure varies widely. Some sponsors have been transparent about NAV facility usage with their LP advisory committees, including the size, the cost, the use of proceeds, and the structural impact on LP economics. Others have provided summary disclosure that did not give LPs enough information to evaluate the implications. A meaningful subset have made the borrowing visible only in financial statements that arrive months after the borrowing has occurred, with limited contextual explanation.

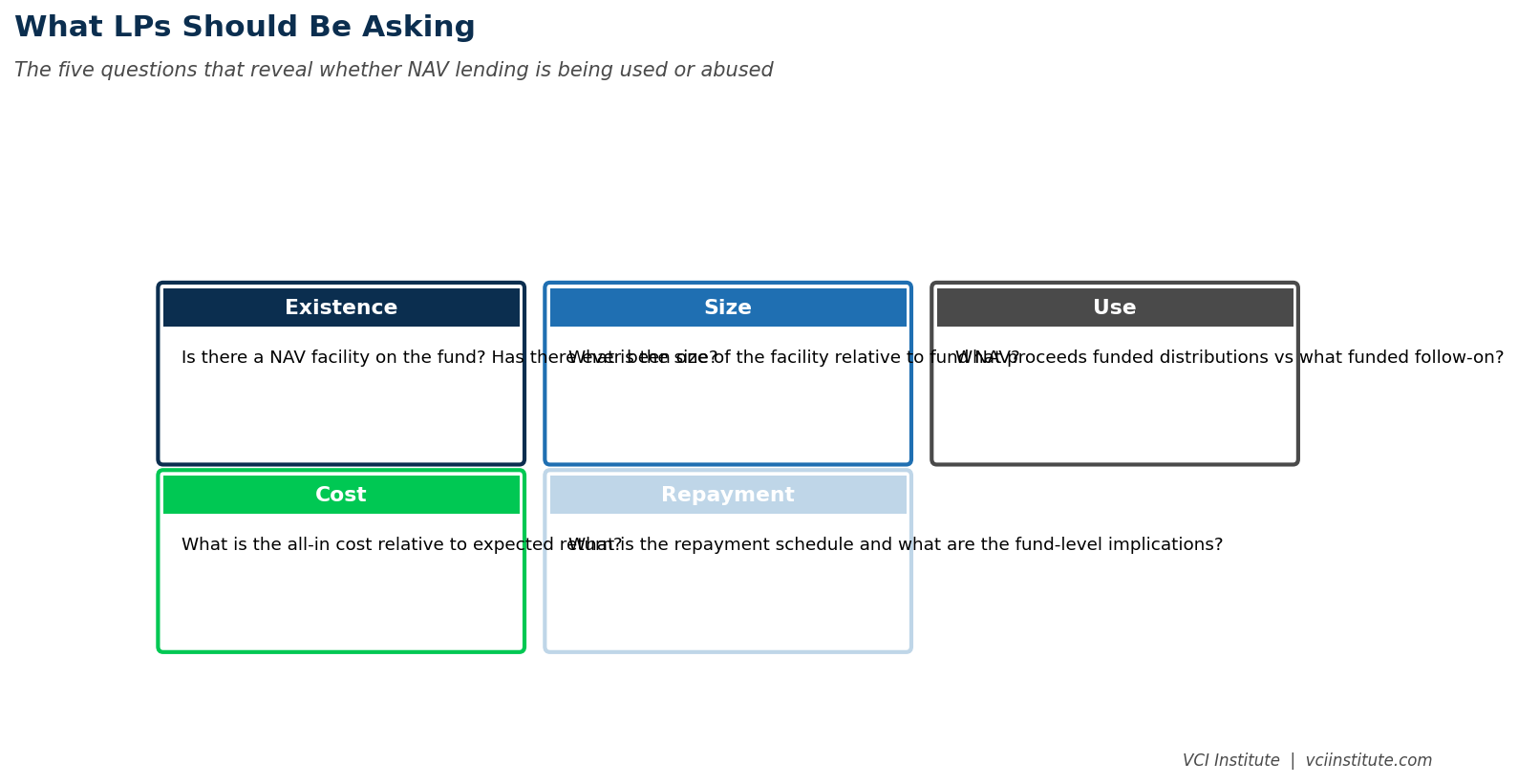

LPs that are sophisticated about this product have started asking specific questions. What is the current outstanding balance of NAV borrowing across our fund. What is the cost of that borrowing. What was it used for. What is the interaction between the NAV facility and the operating leverage at portfolio company level. What is the structure of payment priority between the lender and the LPs at exit. What scenarios would produce a significantly different outcome for LPs than the headline performance numbers suggest.

These questions are not unreasonable. They are, in fact, the questions LPs should be asking about any structural feature that materially affects their economic outcome. Sponsors who can answer them clearly, with documentation, are demonstrating governance maturity. Sponsors who deflect or provide ambiguous answers are creating relationship risk that will surface in the next fundraise.

How Sponsors Should Think About It

For operating partners and deal teams, the discipline around NAV lending is not to avoid the product. The product has legitimate uses. The discipline is to use it transparently, sized to specific needs, with clear LP communication about purpose and impact.

A sponsor that is disciplined about NAV lending typically applies three tests. The first test is whether the borrowing is being used to bridge a known liquidity timing issue with a clear path to repayment, rather than to compensate for portfolio underperformance. If the answer is the former, the borrowing has a defined purpose and a defined endpoint. If the answer is the latter, the borrowing is masking an issue that should be addressed at the portfolio company level.

The second test is whether the borrowing leaves the LPs with a recognizable share of the upside. If the leverage is sized so that even moderate exit outcomes produce reasonable LP returns, the structure is defensible. If the leverage is sized so that LP outcomes depend on aggressive exit assumptions, the structure transfers risk to the LPs in ways that warrant explicit consent rather than implicit acceptance.

The third test is whether LPs have been told in advance that the facility is being put in place, why it is being put in place, and what the implications are for their economic outcome. If LPs are notified after the fact, the disclosure has come too late to be meaningful. If they are notified in advance with sufficient detail, the discussion can happen at the time when the LP advisory committee can actually shape the decision.

What This Means for Operating Partners

Operating partners are usually not directly involved in fund finance decisions. They are, however, increasingly accountable for portfolio company performance in ways that are affected by fund level borrowing. When NAV lending is being used to fund follow-on investments in a struggling portfolio company, the operating partner is being asked to deliver a turnaround under conditions that are now more constrained than the original underwriting.

The discipline for operating partners is to be honest with their deal team partners about whether additional capital, financed by NAV borrowing, is genuinely going to produce the recovery the fund needs, or whether it is going to extend a problem that should be resolved through restructuring, write-down, or sale. The temptation to take additional capital and try harder is real. The cost of taking it and not delivering is real too, both for the LPs and for the operating partner's professional credibility.

A useful reframe is that NAV lending introduces a financial decision that operating partners should weigh in on rather than treat as exogenous. If the borrowing is funding capital that the operating partner does not believe will produce the required recovery, the right response is to push back at the fund level, not to take the capital and hope.

The Quiet Recalibration

The private equity industry is, quietly, in the middle of a recalibration around NAV lending. The early enthusiasm has met with more nuanced LP scrutiny. The underwriting standards of NAV lenders are tightening. The disclosure expectations are rising. The structural features of the facilities, including covenant packages and event of default triggers, are being negotiated more carefully.

Sponsors that anticipate this recalibration and adjust their use of the product proactively will be in a stronger position when the next fundraise comes around. Sponsors that continue to use the product as if the disclosure environment were not changing may find that LPs ask harder questions during diligence than they did during the previous fundraise.

NAV lending is not going away. It will, however, become a more carefully structured, more transparently disclosed, more deliberately sized product than it has been in some segments of the market. Sponsors who get ahead of this shift will have an advantage. Those who do not will face the recalibration on terms they did not choose.

The product, in the end, is a tool. Like any tool, it is useful in the hands of disciplined operators and dangerous in the hands of those using it to defer hard decisions. The next eighteen months will reveal which sponsors fall into which category. The LPs are paying attention.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.