The Asynchronous Fund: Why the Monday Partner Meeting Is the Wrong Place for Real Decisions

May 27, 2026

The Monday partner meeting is, in most established private equity firms, a fixed feature of the operating week. It runs for two to four hours. It assembles the senior partners in a conference room or, increasingly, on a video call. It works through a defined agenda. New deals. Active deals. Portfolio company status. Operations updates. Other business. By the end, the firm has had its weekly cadence. Everyone has been informed of what everyone else is working on. The senior team can claim, accurately, that it is coordinated.

What the firm has rarely done is made any meaningful decision. The Monday meeting has, over time, become a status review meeting that performs the function of decision making without actually doing it. The decisions get made elsewhere, by smaller groups, in side conversations, in emails over the weekend, in one-on-one calls between specific partners. The Monday meeting validates them or, more often, simply notes that they have happened. The room watches the work. The work is not done in the room.

This is not a uniquely PE problem. It is a generic feature of senior coordination meetings in any organization. It is, however, particularly costly in PE because the senior partners' bandwidth is the most expensive resource in the firm, and the Monday meeting consumes a disproportionate share of it for limited return.

The Anatomy of a Typical Monday

A typical Monday meeting reveals its limits if observed carefully. The pattern recurs across firms.

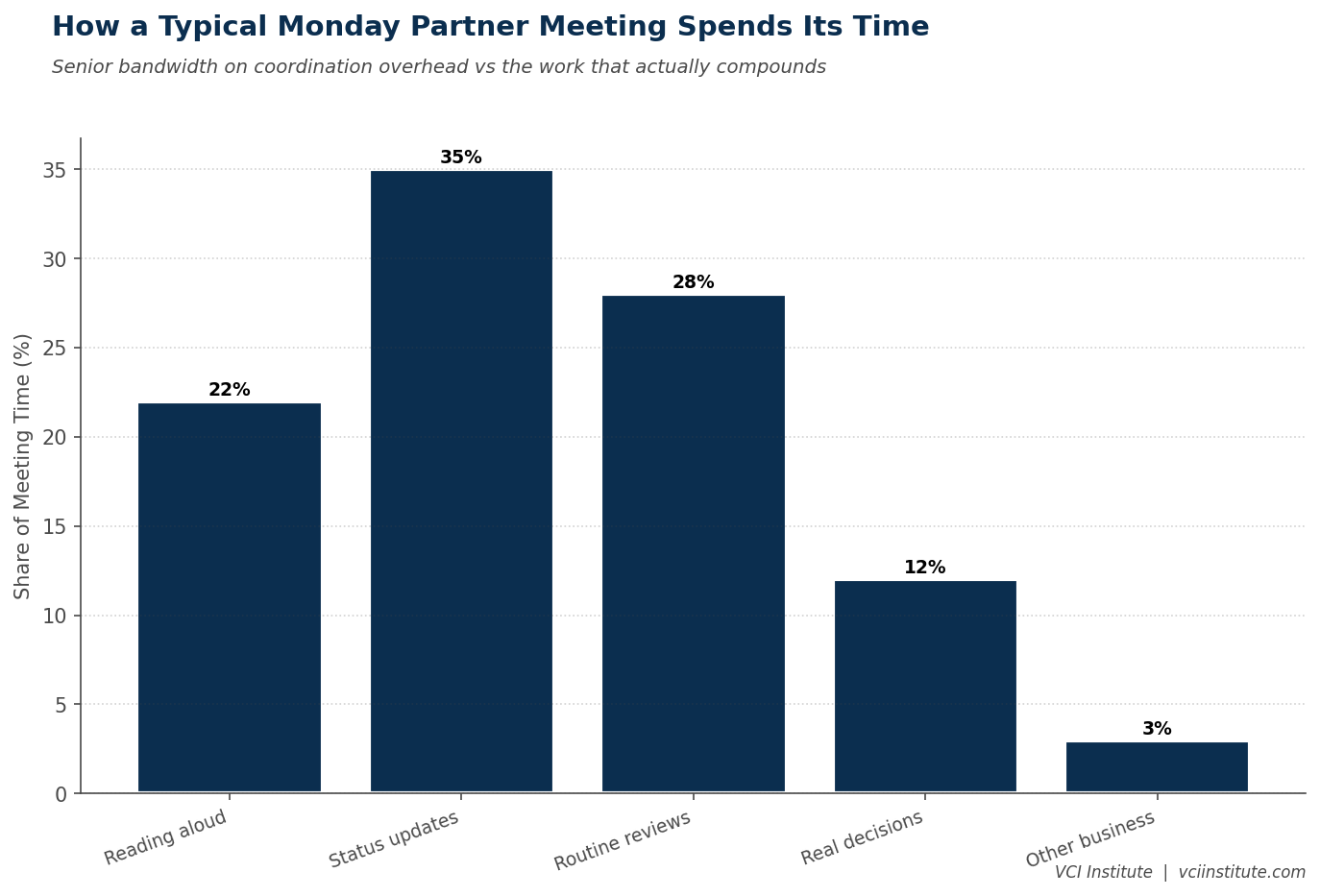

The first thirty minutes are spent on pipeline review. Each deal team partner walks through the deals their team is engaged with. The walk-through is reading material aloud. The information has all been provided in the pipeline document distributed Friday. The reading is performed because the alternative, expecting senior partners to have read the material, has not been institutionalized. The senior partners listen to walk-throughs of information they could have absorbed in fifteen minutes of personal reading.

The middle hour is spent on active deals. Each deal in motion gets a brief update. The updates blend new information that warrants discussion with information that does not. The room engages with most of it at roughly the same depth, regardless of which is consequential. The senior partners ask questions, but the questions are mostly clarifying rather than challenging. The deals that need real decisions get the decisions made in side conversations after the meeting, because the meeting time has been spent on updates rather than on the few items that genuinely required group input.

The last thirty to sixty minutes are on portfolio operations. Each portfolio company gets a brief mention. The discussion ranges across operating issues at varying depths. Most issues are flagged but not resolved, because the bandwidth required to actually resolve them exceeds the time available, and because the operating partners who would drive resolution are sometimes not in the room or are competing for attention with deal team priorities.

By the end of the meeting, several hours of senior bandwidth have been consumed. A small number of decisions have been made, mostly on items that could have been decided asynchronously by a smaller group. A larger number of items have been discussed without resolution and added to the next week's agenda. The cycle continues. The cumulative cost across the year is meaningful. The cumulative output is a coordination that could have been achieved in a fraction of the time.

What an Asynchronous Fund Looks Like

The alternative is not a fund without coordination. It is a fund whose coordination happens primarily through written, asynchronous channels, with synchronous meetings reserved for the small set of decisions and discussions that genuinely require real-time engagement.

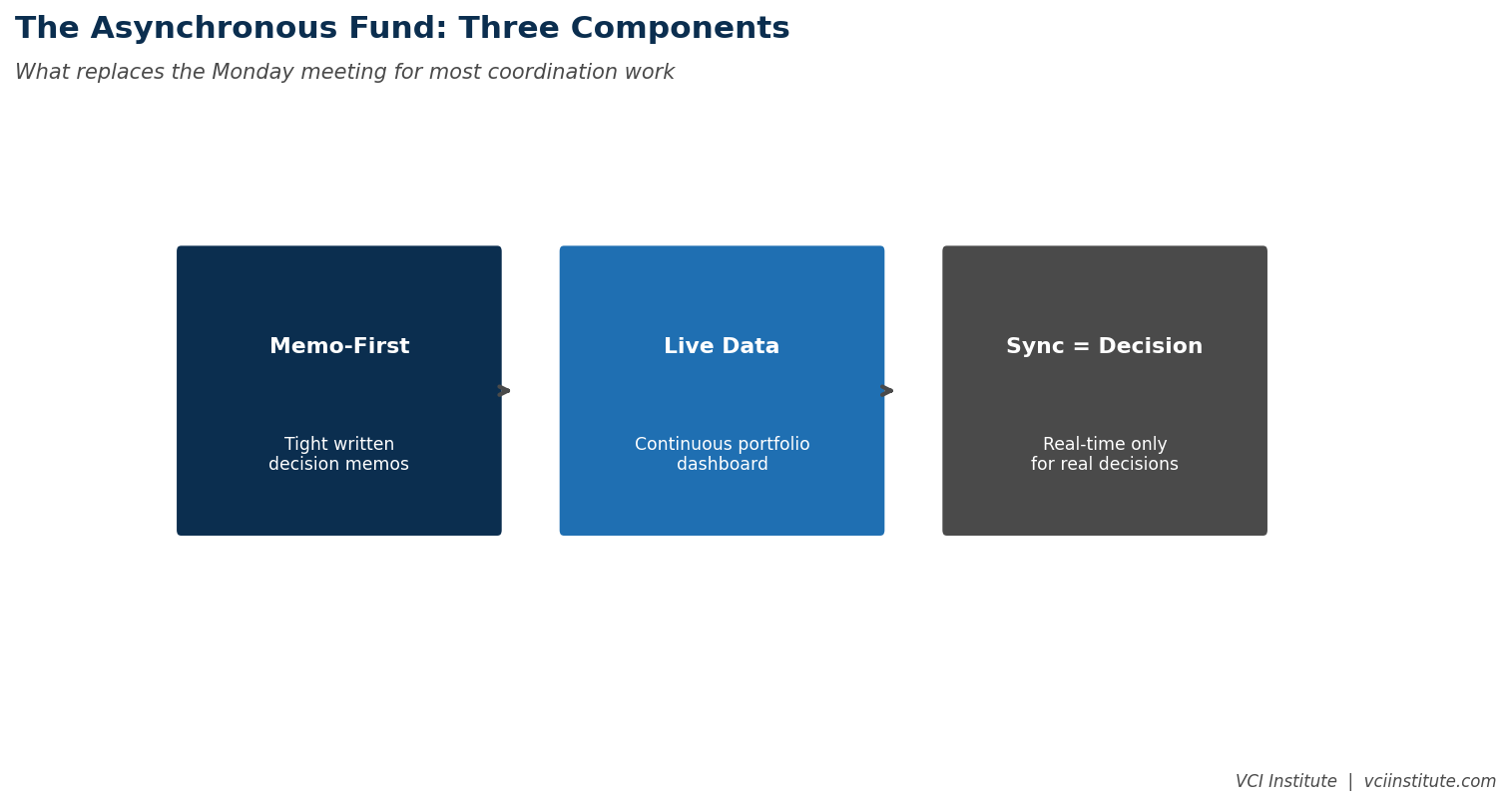

The pattern has three components.

The first component is memo-first communication. Important information is communicated through structured written memos that the recipients are expected to read. Pipeline updates. Deal status reports. Portfolio operating reviews. The memos are written tightly, with the most important content surfaced clearly. The discipline of writing produces clarity that the discipline of speaking does not. The discipline of reading produces engagement with substance rather than passive listening. Several of the most operationally sophisticated firms in technology and consulting have built their cultures on this principle. The PE industry has been slower to adopt it.

The second component is real-time data visibility. Standard operating metrics across the portfolio are available to senior partners through a live dashboard, refreshed continuously. The metrics that would have been reported in the Monday meeting are visible at any time. The senior partner who wants to understand portfolio company performance does not wait for the Monday review. She looks at the data. The data is current. The conversation that follows, if needed, is informed rather than introductory.

The third component is structured asynchronous decision making. When a decision needs to be made, the relevant partner writes a one-page decision memo. The memo states the question, the relevant facts, the recommendation, and the asks of other partners. The other partners respond in writing, with their views. The decision is made by the empowered partner after consideration of the written input. Synchronous discussion is reserved for decisions where the back and forth is genuinely productive, which is a small subset of the total decision flow.

These three components together produce a fund that is more coordinated than the typical Monday-meeting firm and consumes meaningfully less senior bandwidth on coordination overhead. The freed bandwidth becomes available for the work that actually compounds, which is engagement with portfolio companies, sourcing of new opportunities, and development of junior team members.

What Synchronous Meetings Are Actually For

The asynchronous fund does not eliminate meetings. It changes what meetings are for. Three categories of work genuinely require synchronous engagement.

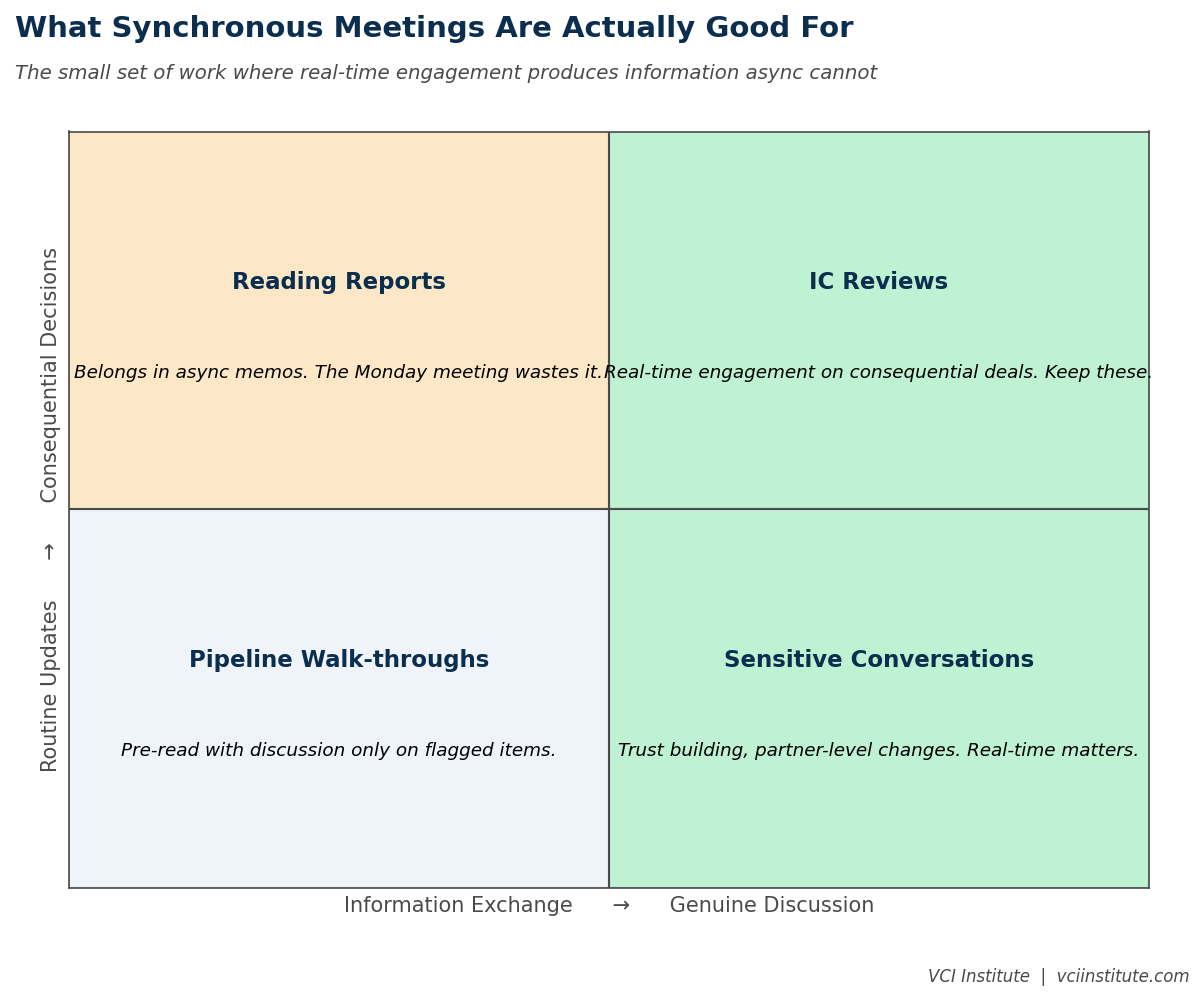

The first category is decisions where the discussion itself produces information that would not exist otherwise. Investment committee reviews on consequential deals where the senior partners' real-time engagement with the proposal surfaces issues, builds shared conviction, and produces commitment that written exchange would not produce. These meetings are valuable and should not be replaced.

The second category is conversations that require trust building or sensitive discussion. Difficult performance conversations with portfolio company management. Negotiations of complex partnership terms with strategic counterparts. Internal discussions about partner-level changes that affect the firm's culture. These conversations work better in person, even when the underlying information could have been communicated in writing.

The third category is creative or strategic work that benefits from real-time exchange. Working sessions where partners brainstorm sourcing strategy, debate sector views, or develop firm strategy. The interactive nature of these sessions produces output that asynchronous exchange would not match.

What is left after these three categories are removed is the bulk of the typical Monday meeting agenda. Pipeline updates. Status reports. Routine portfolio reviews. Standing committee work. None of these require synchronous engagement. All of them currently consume the most expensive bandwidth in the firm because the institutional habit has not been changed.

Why Most Firms Have Not Made the Shift

The shift to asynchronous coordination is, by now, widely understood. Several technology and consulting firms have demonstrated it works. The argument has been made in management literature for over a decade. And yet most PE firms have not made the shift. The reasons are recognizable.

The first reason is that the Monday meeting is culturally encoded. Senior partners have been participating in versions of it for their entire careers. The format feels natural, even when it is not productive. Changing the format requires changing the cultural defaults, which is harder than acknowledging the format is suboptimal.

The second reason is that asynchronous work requires more demanding written communication. Memos that are tight, clear, and decision-focused are harder to write than presentations that are read aloud. The discipline of writing well takes time to develop. Firms that have not invested in writing capability find that the early memos are weak, which produces frustration that confirms the status quo rather than driving improvement.

The third reason is that real-time data visibility requires technology investment that many firms have deferred. The portfolio dashboard that would replace the operating review section of the Monday meeting requires data infrastructure that most firms have not yet built. The infrastructure work is unglamorous and competes with other technology priorities. Without the dashboard, the verbal review continues.

The fourth reason is that some senior partners value the Monday meeting as a social ritual independent of its decision-making content. The meeting provides connection, visibility, and a sense of collective work that the asynchronous alternative does not match. Replacing it requires acknowledging that some of what is being defended is the ritual rather than the productivity, which is uncomfortable to acknowledge.

The combination of cultural inertia, capability gap, technology lag, and ritual value produces a status quo that persists despite widespread recognition that it is suboptimal. The firms that have moved past it have made deliberate cultural commitments and invested in the supporting capabilities. The firms that have not have continued to operate the meetings while gradually losing the most senior partners' engagement, who have learned to use the meeting time for email and to make their actual decisions elsewhere.

The Path to a Better Cadence

The shift does not have to be revolutionary. Three changes, made deliberately, produce a meaningfully better cadence within six to twelve months.

The first change is to require pre-read materials and to enforce the requirement. The Monday meeting opens with the assumption that everyone has read the materials. Walk-throughs are eliminated. Discussion goes directly to the items that warrant discussion. This change alone reduces meeting time by thirty to fifty percent and improves the quality of the engagement that remains.

The second change is to build the operating dashboard. Standard portfolio operating metrics, refreshed at least weekly, accessible to all senior partners. The portfolio review section of the Monday meeting becomes optional rather than central, because the data is available continuously. The exception-driven model that emerges is more useful than the comprehensive review model it replaces.

The third change is to introduce the decision memo discipline. Decisions that historically were made in Monday meetings are increasingly made through written memo and asynchronous response. The Monday meeting becomes a forum for the small set of decisions that genuinely require real-time engagement, not the catch-all decision venue it currently is.

These three changes together transform the cadence without dismantling it. The Monday meeting continues to exist but plays a different role. The bandwidth freed by the shift becomes available for higher-leverage work. The decision quality, by most measures used by firms that have made the shift, actually improves, because the decisions are made by the empowered parties with structured input rather than in real-time conversations that are dominated by the loudest voices in the room.

The cumulative effect, over a fund cycle, is a meaningful productivity gain at the senior level of the firm. Whether that gain shows up in better deals, more thorough operating engagement, or stronger LP relationships depends on what the freed bandwidth is redirected to. In the firms that have made the change deliberately, all three benefits typically show up to some degree.

The Monday partner meeting will not disappear from PE. It is too encoded in the industry's culture. The firms that work past it, deliberately and without theatrical announcement, will operate at a different productivity level than those that do not. The advantage will not be visible from outside. It will be visible in the cumulative output the firm produces over a fund cycle. The choice of how to coordinate the firm is, in the end, a choice about what to do with the most expensive bandwidth in the business. The Monday meeting is not the only answer. It is, increasingly, the wrong one for firms that take their senior partners' time seriously.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.