The Performance Review Conversation Most Sponsors Are Having Twelve Months Too Late

Jun 04, 2026

December and January in mid-market portfolio companies follow a recognizable rhythm. The annual operating plan from the prior year is reviewed against actuals. Performance is assessed. Bonus pools are sized. Individual reviews happen. Some are smooth. Many are difficult. The difficult ones often produce the same patterns. Managers who feel they were held accountable to expectations they did not actually agree to. Employees who feel they were judged against goals that shifted during the year. CEOs who find themselves having to defend or modify the framework they inherited. Sponsors who watch the process and conclude that performance management at the portfolio company is uneven without quite naming what is missing.

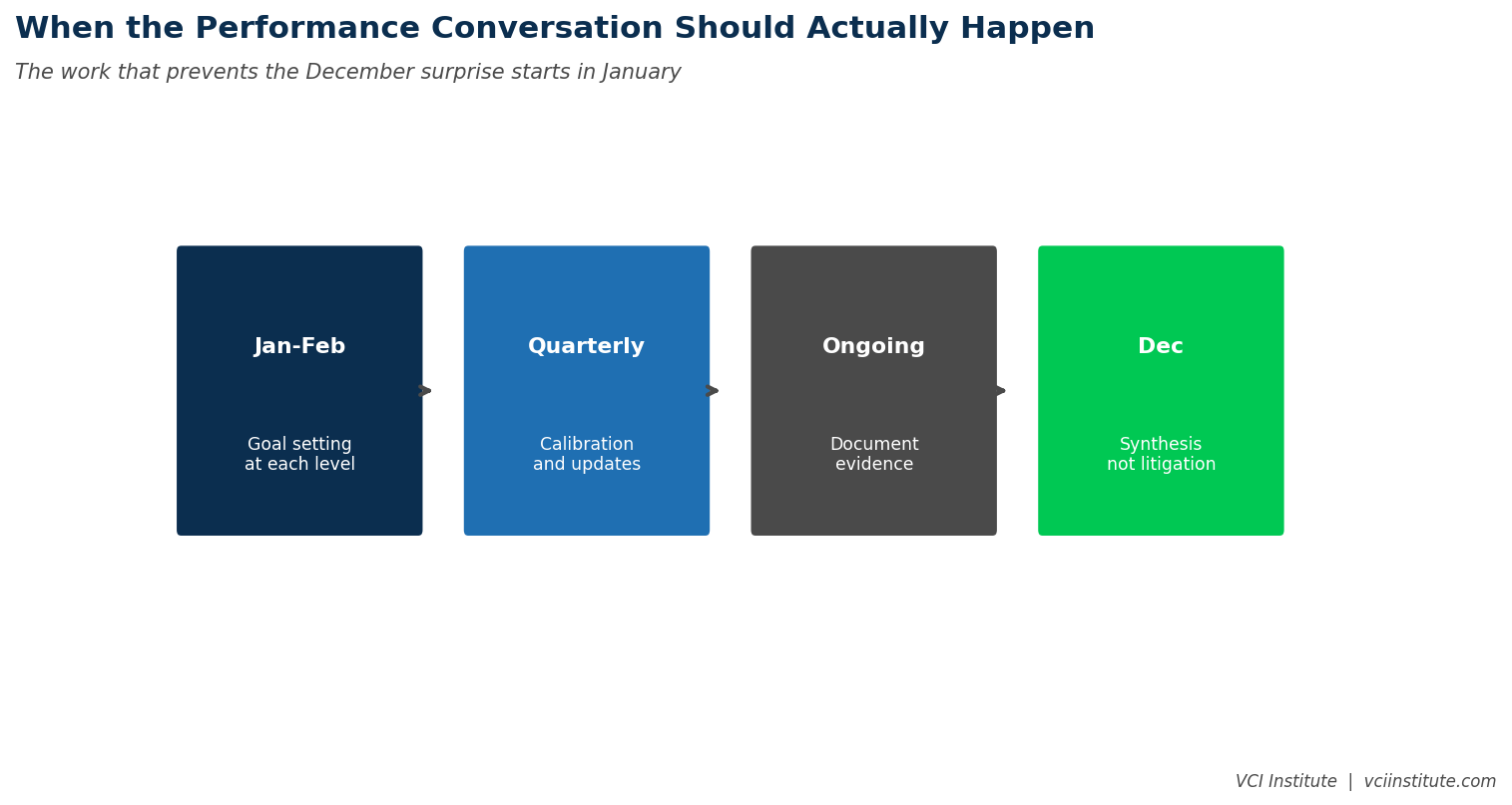

The diagnosis is usually wrong. The problem in difficult year-end reviews is rarely that the review itself was conducted poorly. The problem is that the goals being reviewed against were never properly set in the first place. The conversation that should have happened in January or February of the prior year, when expectations were being established, was either skipped entirely or done so loosely that nobody can later agree on what was actually committed to. The review is then the moment when the gap becomes visible. By December, it is too late to fix the gap. The review can only manage the consequences.

This pattern is so common that most sponsors have learned to live with it. Operating partners hear the December complaints, manage the political fallout, and resolve to do better in the next year. The next year produces the same pattern, because the goal-setting work that would have prevented it still does not happen with the discipline required. The cycle repeats.

Why the Goal-Setting Conversation Gets Skipped

The structural reasons that goal setting gets done badly are recognizable. They show up across portfolio companies regardless of sector or size.

The first reason is that goal setting is harder than it looks. Specifying what success looks like for a complex role, in concrete and measurable terms, requires real thought. The CEO has to think hard about what she actually expects from each direct report. The direct reports have to think hard about what they can credibly commit to. The negotiation between expectations and commitments takes time and produces a document that has to be specific enough to be useful and flexible enough to accommodate the reality that businesses change during the year. Most management teams default to looser specifications because the loose version takes less time to produce and feels easier in the moment.

The second reason is that the timing pressure works against doing it well. The annual planning cycle in most portfolio companies finishes in December or January. The board meeting approves the budget. The CEO is then expected to translate the budget into individual goals quickly so the team can start the year. The translation often gets done in a hurry. Each direct report receives goals that are essentially the budget restated rather than goals that are tailored to what the role specifically should deliver. The goals work as a paperwork exercise. They do not work as an operating tool.

The third reason is that the consequences of weak goal setting are deferred. The cost of a vague set of expectations does not appear in the next quarter. It appears in the December review, eleven months later, when the manager and the employee discover that they have different memories of what was committed to. By then, the cost has been built into the year's outcomes. The poor goal-setting work has produced a poor performance management cycle, but the link between the two is delayed enough that the next year's goal setting often does not benefit from the lesson.

The fourth reason is that goal setting requires the CEO and the operating partner to have a clear and shared view of what each role should produce. Many portfolio companies do not have this clarity. The roles have evolved organically. The CEO has views. The operating partner has views. The two sets of views are not always aligned and are rarely written down. The goal-setting conversation with each direct report becomes the place where the lack of CEO and operating partner alignment surfaces, which produces conversations that are about more than just one person's goals. The complexity discourages doing the work seriously.

What Disciplined Goal Setting Actually Looks Like

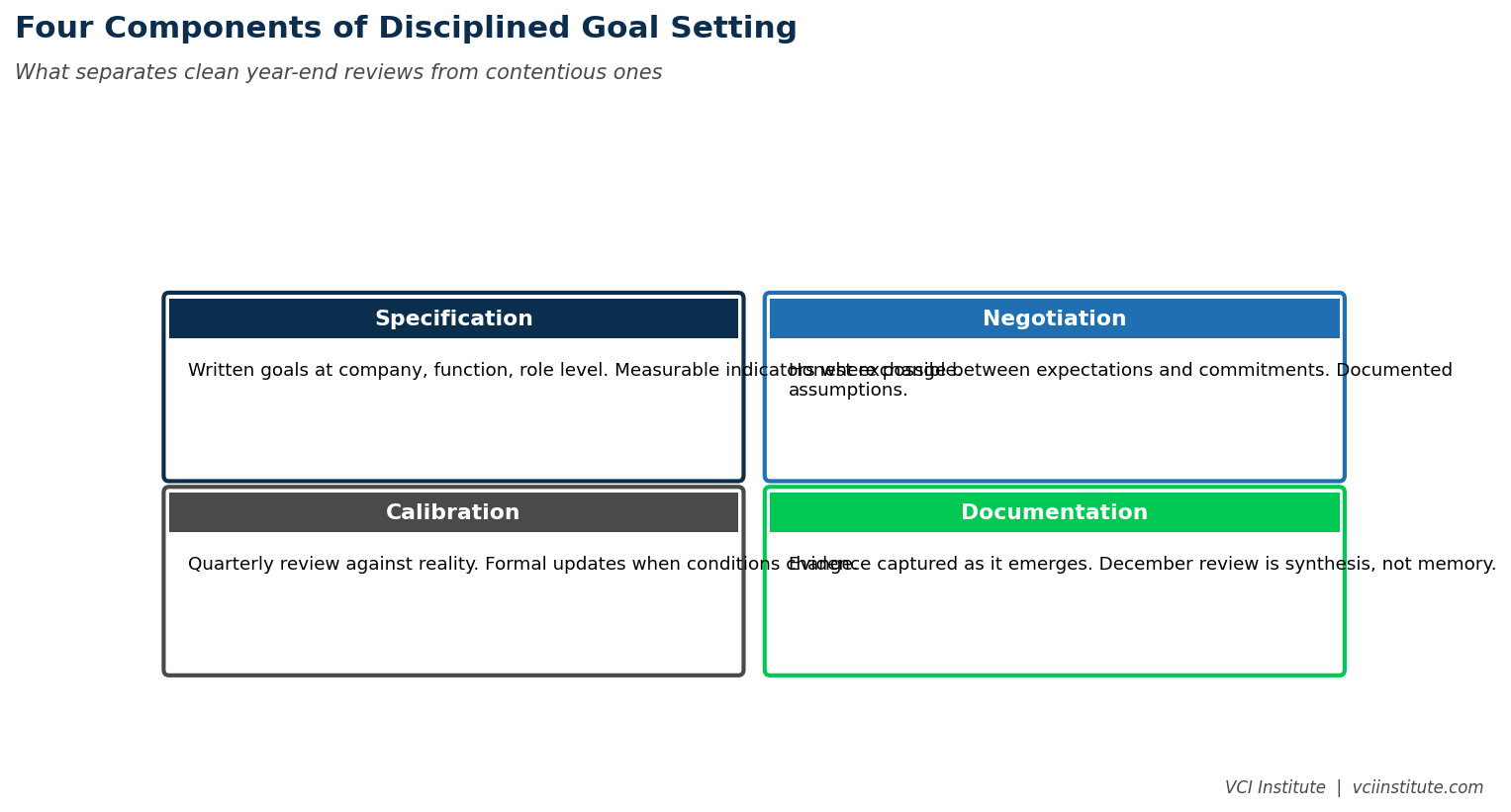

The discipline that produces clean year-end reviews twelve months later is recognizable. It has four components.

The first component is explicit specification of what success looks like at each level of the organization. The company. Each department. Each role. The specifications are written down, with measurable indicators where possible, and reviewed by the CEO with each direct report individually. The work takes two to three weeks if done seriously. The output is a set of agreements about what the year is trying to produce, role by role.

The second component is honest negotiation between expectations and commitments. The CEO has expectations. The direct report has views about what is achievable. The conversation that reconciles these views, in writing, with documented assumptions and contingencies, is the work that produces shared understanding. Without it, the goals end up being the CEO's expectations imposed on the direct report, which produces compliance rather than commitment.

The third component is regular calibration through the year. The goals set in January are reviewed against reality at quarterly intervals. When circumstances change in ways that affect what is achievable, the goals are formally updated, with documentation of why. The calibration prevents the December surprise where the manager and the employee disagree about whether the goal still applied. The discipline of formal updates is unusual in mid-market companies. Without it, informal updates accumulate and produce ambiguity.

The fourth component is documentation of evidence as the year progresses. As performance information emerges, it is captured in writing rather than left to memory. The strong execution on the major project. The struggle with the difficult customer relationship. The hire that worked out and the hire that did not. The documentation makes the year-end conversation a synthesis of recorded evidence rather than a debate about competing memories.

These four components together describe a different relationship between the CEO and the direct reports than what most mid-market companies have. The work to build this relationship takes deliberate investment. It produces year-end reviews that are productive rather than contentious, because the conversation by December is reviewing well-documented progress against well-defined commitments rather than litigating what was meant by ambiguous statements made eleven months ago.

The Question Worth Asking in January

The question every operating partner should ask the CEO of every portfolio company in the first quarter of the year is, what does success look like by December, specifically. For the company. For each function. For each direct report. The question is simple. The answers reveal whether the goal-setting work has been done.

If the CEO can answer the question with specific metrics, with documented agreements, with clear commitments from each direct report on what they will deliver, the year is set up to produce a clean review in December. The work has been done. The framework exists.

If the CEO answers the question with general aspirations, vague metrics, or commitments that have not been written down with each direct report individually, the year is set up to produce the difficult review in December. The framework does not exist. The December conversation will be the moment when the gap becomes visible.

The diagnostic is uncomfortable to apply because it surfaces gaps that are easier to leave undiscovered until December. Operating partners who apply it consistently find that they spend more time in January and February supporting the goal-setting work and less time in December managing the consequences of work that did not get done.

What This Looks Like Across the Portfolio

For sponsors thinking about portfolio operating discipline, the goal-setting cadence is one of the simplest operating practices to standardize across portfolio companies. The standard does not have to be elaborate. Three commitments produce most of the value.

The first commitment is that every portfolio company has, by the end of February each year, documented goals at the company level, the function level, and the individual level for each direct report of the CEO. The documentation is written, signed off by the CEO and the direct report, and shared with the operating partner.

The second commitment is that quarterly reviews include a calibration of the goals against the year-to-date reality, with formal updates documented when circumstances have changed in ways that affect what is achievable. The quarterly reviews are not theater. They are working sessions that adjust commitments to changing conditions.

The third commitment is that year-end reviews are conducted against the documented goals as updated through the year, not against memories of what was discussed informally. The review conversations are easier because the framework exists.

These three commitments, applied across the portfolio, produce a different operating discipline. The portfolio companies that do them well have year-end reviews that are productive. The portfolio companies that do not do them well continue to produce the same December surprises every year. The compounding effect over a hold period is meaningful.

The Compounding Effect of Clarity

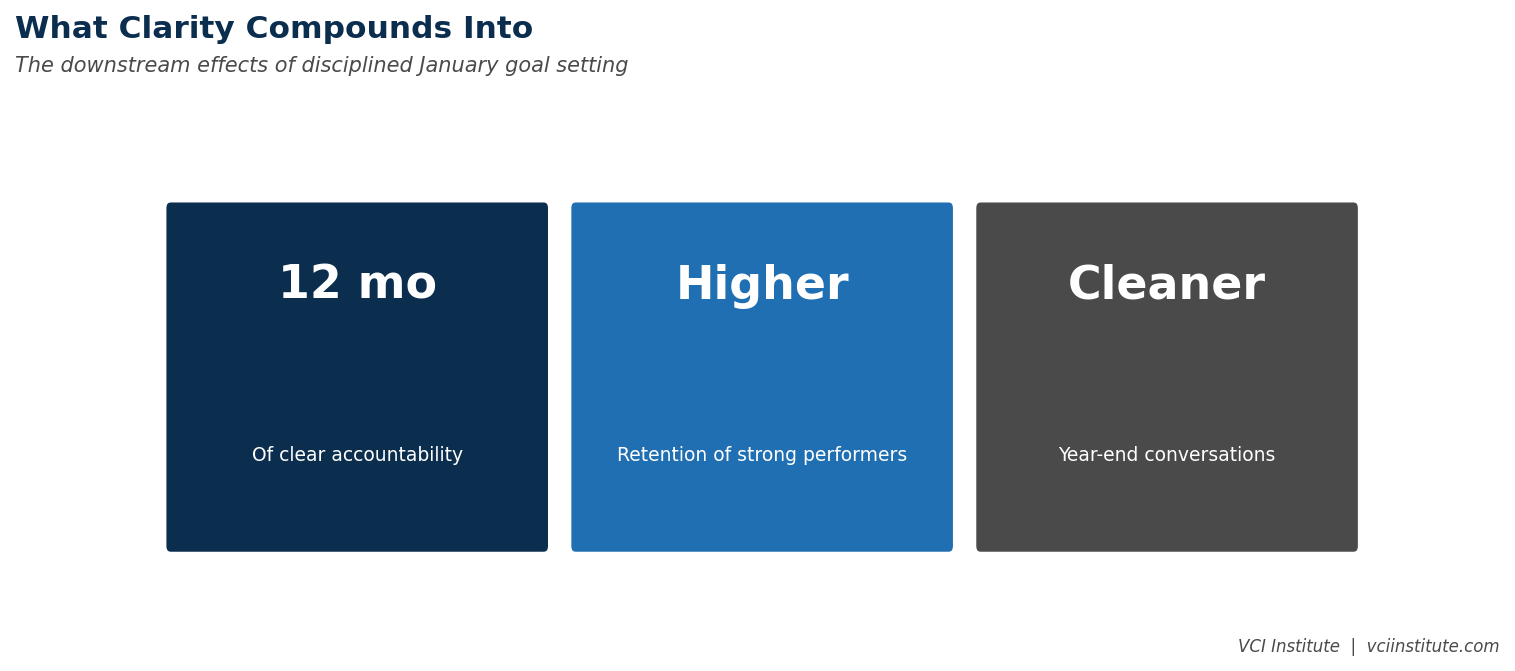

Goal setting and performance management are not the most consequential value creation work in any single portfolio company. They are, however, the work that compounds. A management team operating with clear goals, regular calibration, and clean year-end reviews makes better decisions through the year because everyone knows what they are accountable for. The team retains stronger people because the strong people experience the clarity as fairness. The team executes more reliably because the framework allows performance to be discussed honestly without becoming personal.

The compounding effect is not visible in any single quarter. It is visible across multiple years. The portfolio companies that have built the discipline produce a different operating tempo than those that have not. The CEO is not consumed by repeated litigation of unclear commitments. The direct reports are not navigating ambiguity about what they need to deliver. The operating partner is not spending December cleaning up problems that should have been prevented in January.

This is the kind of discipline that distinguishes sponsors who build durable value creation outcomes from sponsors who deliver transactional improvements that do not compound. The goal-setting work is not glamorous. It does not feature in marketing materials. It is, however, one of the highest leverage capabilities a portfolio company can develop, and one of the most consistent markers of operating maturity that LPs are starting to read.

The performance review conversation most sponsors are having in December is, in the well-run portfolio companies, a reasonably straightforward synthesis of documented work. In the less well-run companies, it is the moment when twelve months of accumulated ambiguity finally becomes visible. The difference is not in the December conversation itself. The difference is in the January conversation, eleven months earlier, that either set up a productive year or did not. Operating partners who insist on the January work, consistently across the portfolio, year after year, produce the kind of operating discipline that is genuinely hard to replicate. Those who do not are doomed to have the same December conversations every year, with the same explanations to the board about why performance management at the portfolio is uneven, without quite naming the upstream choice that produced the unevenness.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.