The Pricing Power Lever Most PE Firms Still Underbuild

May 13, 2026

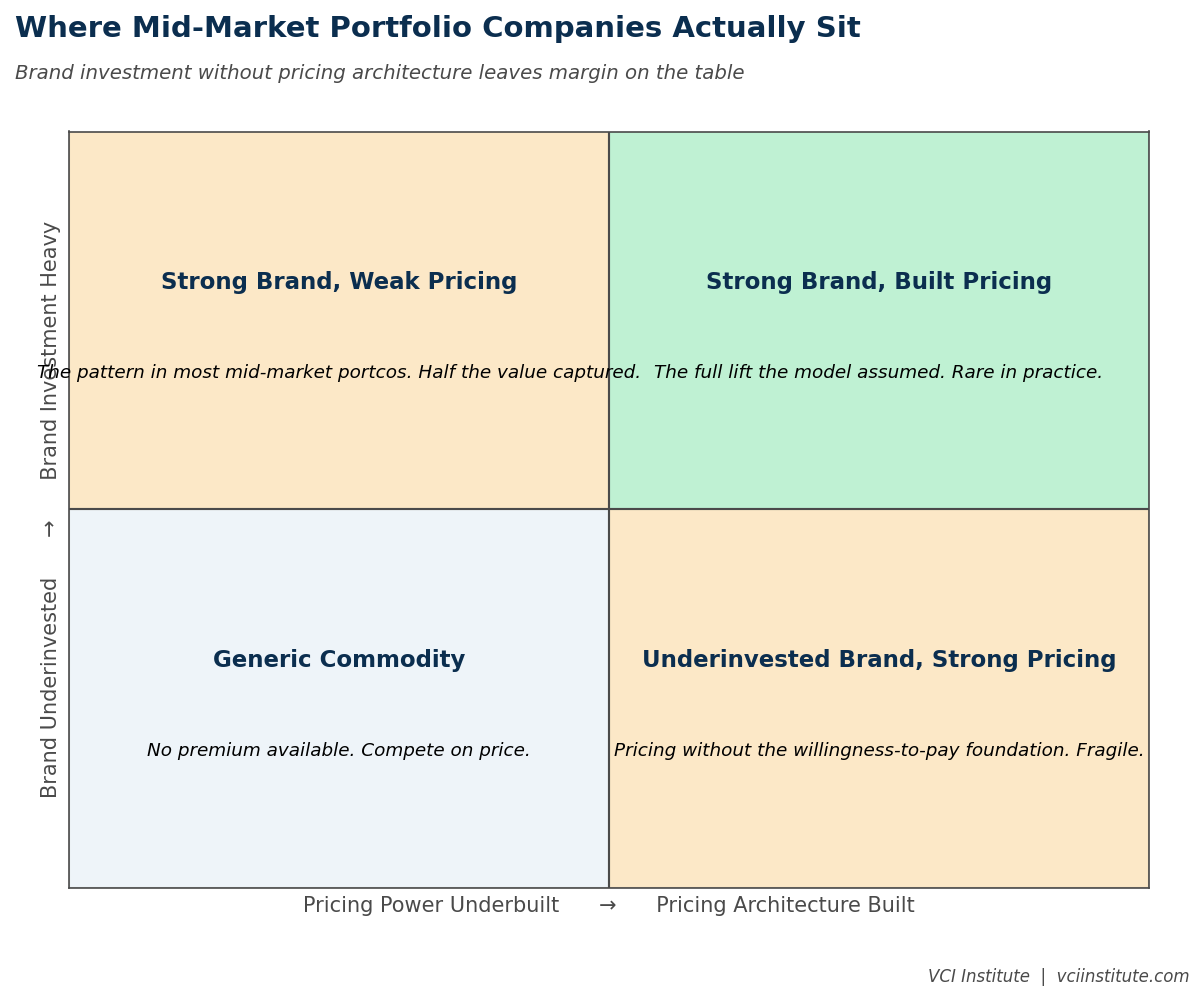

Most mid-market portfolio companies have invested meaningfully in their brand. They have refreshed their websites, modernized their visual identity, hired marketing leadership, built content engines, and refined their positioning narratives. Most of these investments are reasonable. Some are necessary. None of them produce the lift the underwriting case assumed unless they are paired with the lever that actually monetizes the brand work.

That lever is pricing architecture. The disciplined, deliberate engineering of how the company prices its products and services to capture the value the brand investment makes possible. Most mid-market portfolio companies have not built it. The brand work is doing partial duty in their value creation plans, producing some commercial lift but not the full lift the brand investment could generate if pricing were addressed seriously. The gap between what brand investment alone produces and what brand investment plus pricing architecture produces is, in many businesses, several hundred basis points of margin.

This is not a vendor problem. It is an operating discipline problem. The firms that have built genuine pricing capability have done so deliberately, against the cultural pull that treats pricing as either a finance function or a sales function rather than as a strategic capability that requires its own infrastructure.

Why Marketing Without Pricing Underperforms

The logic of why brand investment alone underperforms is straightforward, even if it is rarely stated this way in board meetings.

A brand is, in commercial terms, a willingness-to-pay premium. The customers who recognize and trust the brand are willing to pay more for what they perceive as a more reliable, higher quality, or more aligned offering. The brand investment makes this willingness-to-pay larger. The pricing structure determines how much of the larger willingness-to-pay actually shows up in the company's revenue.

In most mid-market businesses, the pricing structure was set years ago, often by the founder or by a long-tenured commercial leader, based on competitive pricing in the market at that time. The structure has been adjusted incrementally for inflation, but its underlying logic has not been refreshed. The brand investment is increasing willingness-to-pay. The pricing structure is leaving most of the increase on the table.

A simple test reveals this in almost every business. Pull a sample of recent customer transactions and compare the negotiated prices to a basket of comparable transactions in the market. In businesses with weak pricing discipline, the negotiated prices cluster well below what willing-to-pay analysis would suggest the customer would have accepted. The discount is rarely the result of a strategic decision. It is the result of a sales process that anchored on legacy pricing logic and never tested whether the legacy logic still applied.

This is the gap. The brand investment created room. The pricing structure did not move into it.

What Pricing Architecture Actually Looks Like

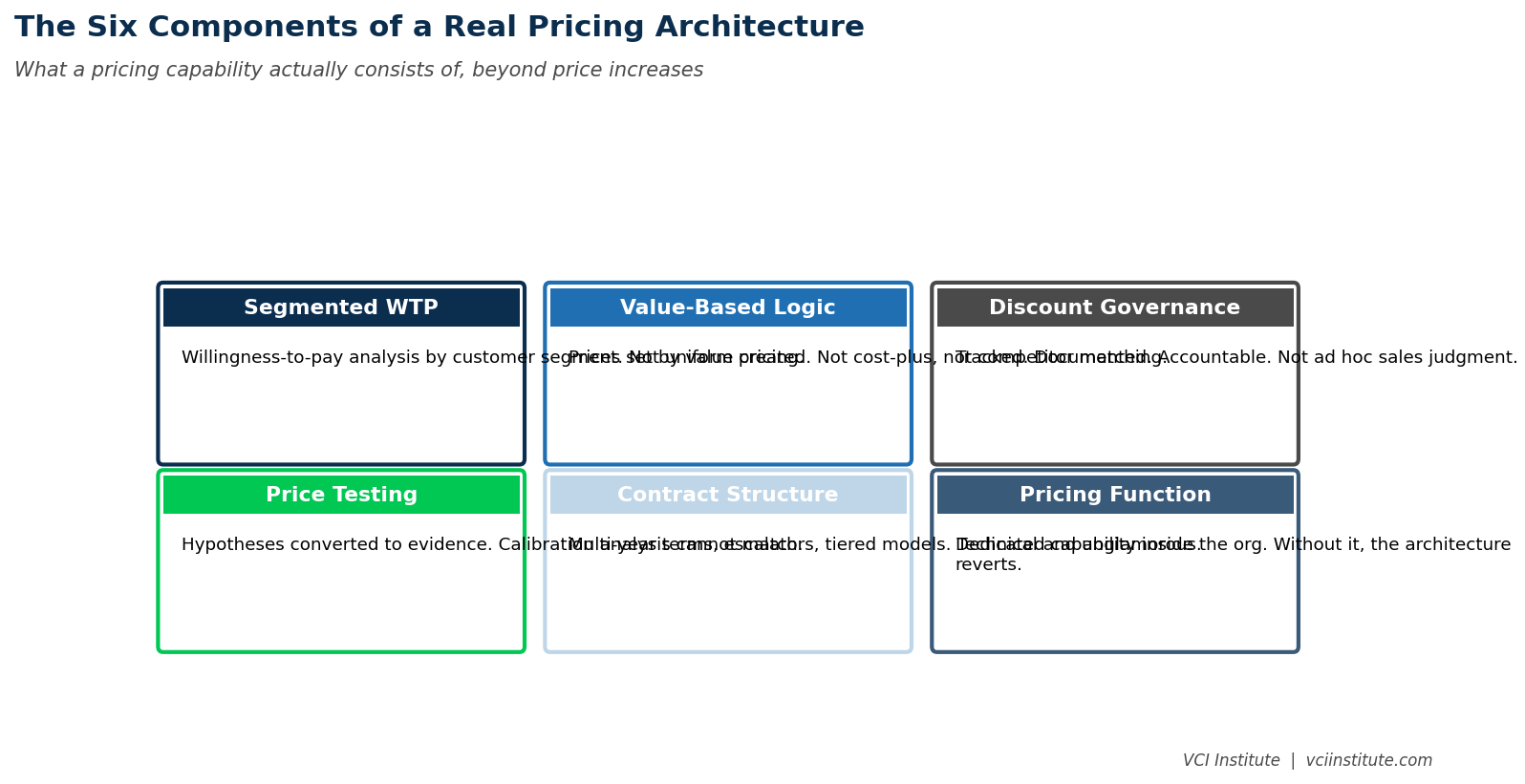

Pricing architecture, as a deliberate capability, has six components. None of them are exotic. All of them are absent from most mid-market portfolio companies.

The first component is segmented willingness-to-pay analysis. Different customer segments have different willingness-to-pay for the same offering, based on the value the offering creates for them, the alternatives available to them, and the strategic importance of the relationship. A pricing architecture worth building starts with understanding these differences, not assuming uniform pricing across segments.

The second component is value-based pricing logic. Prices are set based on the value the offering creates for the customer, not based on cost-plus calculations or competitor matching. The value-based logic produces meaningfully higher realized prices in segments where the value delivered exceeds what cost-plus would imply, while protecting against under-pricing in segments where the offering is genuinely commoditized.

The third component is structured discount governance. Most mid-market businesses have a discount problem they have not named. Sales reps grant discounts to close deals, with limited oversight, limited tracking, and no aggregate discipline. The cumulative effect is meaningful margin erosion. A discount governance structure documents the rules, tracks the actual discounts being granted, and creates accountability for sales leaders to manage discount levels as a metric rather than as a deal-specific judgment.

The fourth component is price testing. The willingness-to-pay analysis is a hypothesis. Price testing converts the hypothesis into evidence. Some segments will accept higher prices than the analysis suggested. Some will reject prices the analysis predicted they would accept. The testing produces calibration that no analytical exercise alone can match. Most mid-market businesses have never run structured price tests. The first wave of testing usually reveals significant pricing power that has been left dormant.

The fifth component is contract structure. Multi-year contracts with built-in escalators. Tiered pricing structures that move customers up the value ladder. Pricing models that align with the customer's consumption pattern. The contract structure work is technical and unglamorous. It produces real lift over time as the customer base rolls onto the new structures.

The sixth component is pricing capability inside the organization. A pricing function staffed with the discipline and authority to maintain the architecture. Without dedicated capability, pricing decisions revert to ad hoc sales judgment within twelve months of any pricing initiative, regardless of how good the initial work was.

Why This Lever Stays Underbuilt

The pricing power lever is well known and rarely deployed in mid-market PE. Three reasons explain the gap.

The first reason is that pricing transformation is uncomfortable. It surfaces conversations the management team has been avoiding. The CFO suspects pricing is too low but has not built the analytical case. The CEO is not sure whether the sales team can hold higher prices. The CRO worries that price increases will disrupt customer relationships that are already fragile. None of these concerns is unreasonable. Together they produce inertia that prevents the work from starting.

The second reason is that pricing transformation requires capability the business does not have. A pricing function is a specialized discipline that mid-market companies rarely have built internally. The work requires either external advisory help, which the company is reluctant to fund, or new senior hires, which the company is reluctant to commit to. The result is that pricing work, when it does happen, is led by people whose primary jobs are something else, with the predictable outcomes of secondary effort applied to primary work.

The third reason is that the payback timeline is uncomfortable for some operating partners. Pricing transformation produces meaningful lift, but the lift takes nine to fifteen months to fully materialize. The first three to six months involve analytical work that has no visible commercial output. The visible lift starts in months six to nine. Operating partners under pressure to demonstrate quick wins sometimes choose other initiatives that produce visible output faster, even when those initiatives have weaker EBITDA bridges than pricing would have produced.

The combination of discomfort, capability gap, and payback timeline produces a pattern where pricing initiatives are discussed in board meetings, agreed in principle, deferred in execution, and then quietly dropped from the value creation plan. The lever sits unused while operating partners pursue other initiatives that produce visible activity but smaller economic impact.

The Implementation Sequence That Works

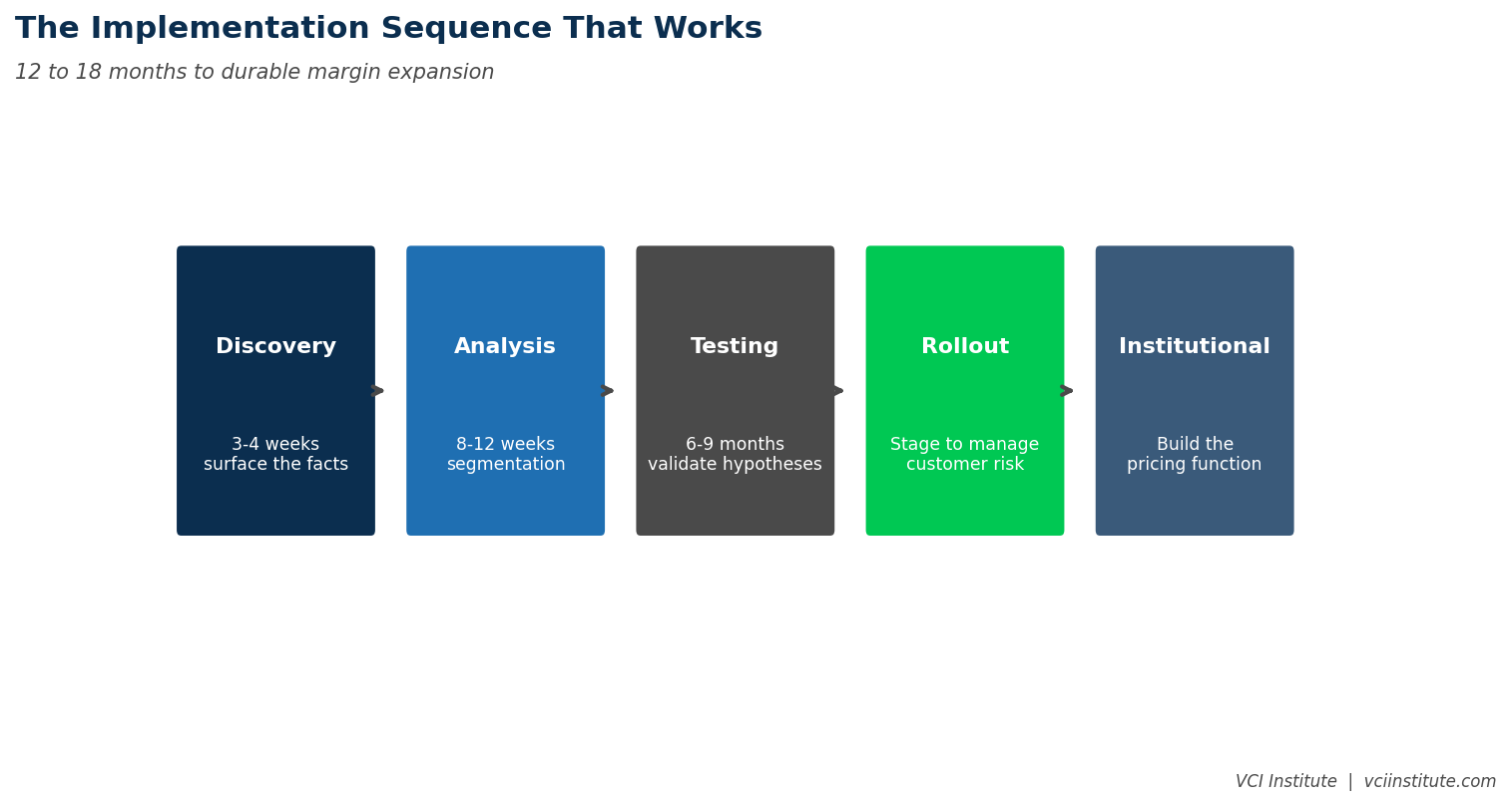

Operating partners that have captured the pricing lever successfully usually follow a recognizable sequence.

The first step is the discovery phase. Three to four weeks of analytical work to surface the pricing reality of the business. Realized prices by segment, by product, by sales rep, by deal size. Discount frequency and depth. Pricing variance compared to competitor benchmarks where available. The output of this phase is usually a presentation to the management team that surfaces the pricing facts the business has not yet seen aggregated. The conversation that follows shapes the political possibility of the next phases.

The second step is segmentation and willingness-to-pay analysis. Eight to twelve weeks of structured customer research, transaction analysis, and competitive benchmarking. The output is a segmented view of the customer base with willingness-to-pay estimates and a hypothesis about which segments are systematically under-priced. This phase produces the analytical foundation for the changes that follow.

The third step is testing. Selected segments and selected products are subjected to structured pricing tests, usually over a six to nine month period. The tests produce evidence about which willingness-to-pay hypotheses hold up in practice and which need revision. The testing is the bridge between analysis and rollout.

The fourth step is rollout. The validated changes are implemented across the broader customer base, with careful customer communication, sales team enablement, and discount governance updates. The rollout is staged to manage customer relationship risk and to allow course correction if specific segments respond differently than the testing suggested.

The fifth step is institutionalization. The pricing function is built or strengthened to maintain the architecture going forward. This is the step that prevents reversion. Without it, the gains erode within twelve to eighteen months as ad hoc sales decisions accumulate and the structure drifts.

The full sequence takes twelve to eighteen months. The compounding lift continues for the rest of the hold. By exit, a portfolio company that has built pricing architecture has typically expanded margin by two hundred to five hundred basis points relative to what brand investment alone would have produced.

What Operating Partners Should Press For

Operating partners working with portfolio companies that are investing in brand and marketing should make sure pricing architecture is part of the same conversation. Three asks usually clarify the issue.

The first ask is to see the pricing facts. What are realized prices by segment. What is the discount frequency and depth. What is the pricing variance across the sales team. If the management team cannot produce these facts in two weeks, pricing has not been treated as a managed function and the transformation work needs to start.

The second ask is to identify the pricing hypothesis. Where in the customer base is willingness-to-pay believed to be underutilized. What is the management team's view of the segments where pricing power is underbuilt. If the team has not yet thought about this question, the analytical work needs to be funded.

The third ask is to commit to capability. Pricing transformation without a pricing function eventually reverts. Either the business builds the capability internally or it commits to external advisory support that builds it. Either path is acceptable. No path is not.

The combination of pricing facts, pricing hypothesis, and pricing capability produces a portfolio company that has actually built the lever rather than discussed it. The lever is one of the highest leverage moves available in mid-market value creation. It costs little. It produces meaningful margin lift. It compounds across the hold period. The only reason it stays underbuilt is institutional inertia. The operating partners who push past the inertia, in the businesses where pricing power is genuinely available, capture economics that their competitors leave on the table. The brand work was never going to be enough by itself. The pricing architecture is what turns brand investment into the EBITDA the model assumed.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.