Why Private Equity Is the Hardest Industry to Apply AI To

Apr 29, 2026

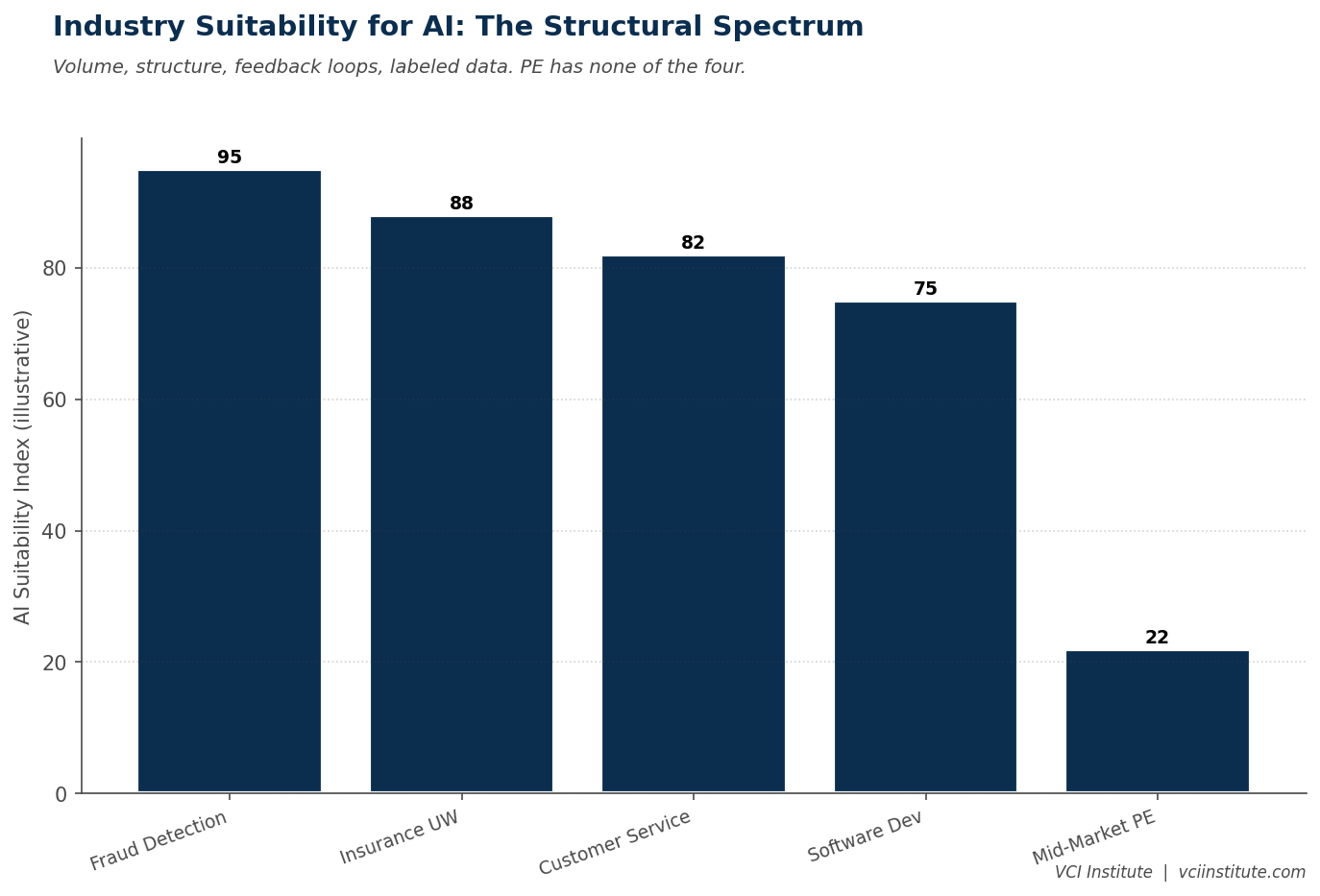

AI has produced visible step changes in several industries over the past five years. Insurance underwriting accuracy has improved measurably. Fraud detection in payments has gotten dramatically better. Software development productivity has shifted by twenty to forty percent in the categories where copilots fit cleanly. Customer service automation has reduced cost meaningfully in high volume contact centers.

Private equity has not seen the same step change. Most senior partners, asked honestly, will admit that the AI investments their firms have made over the past three years have produced incremental productivity rather than transformational improvement. The diligence tools are useful. The portfolio dashboards are cleaner. The drafting assistance saves time. None of it has yet changed how deals are done in any way that would be visible to an LP comparing 2026 returns to 2020 returns.

This is not because PE firms are slow. It is because PE is, structurally, one of the hardest industries to apply AI to. Understanding why is the first step toward an AI roadmap that has any chance of paying back.

Figure: 32a difficulty spectrum

What the Easy Industries Got Right

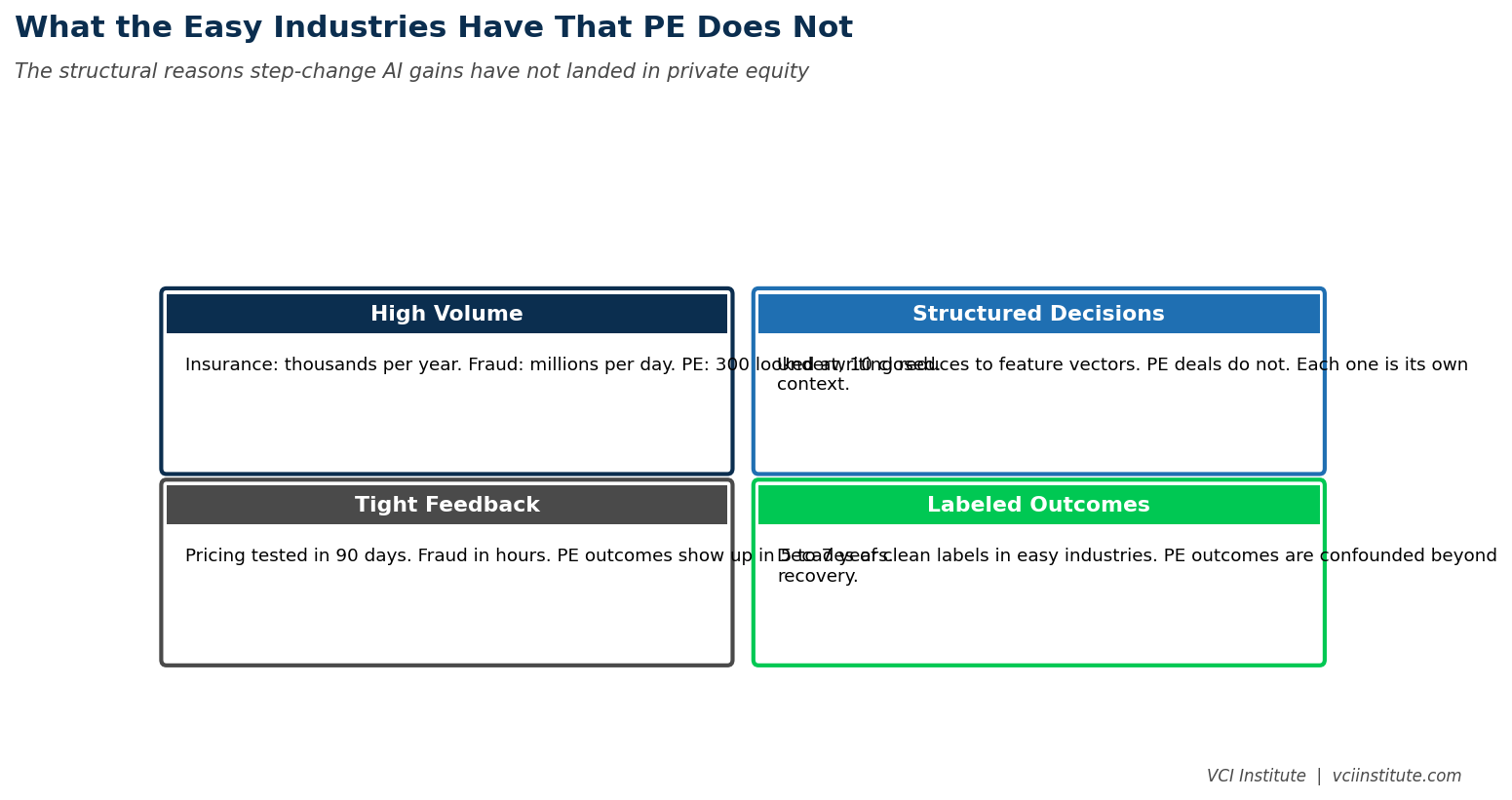

The industries where AI has produced step changes share four features. Each feature is something private equity does not have.

The first feature is high volume. Insurance underwriters look at thousands of policies per year. Fraud systems process millions of transactions per day. Customer service handles millions of interactions per quarter. The volume produces enough data for models to learn patterns, and enough decisions for incremental improvements to matter at scale. Private equity, by comparison, is a low volume industry. A mid-market firm looks at perhaps three hundred deals per year and closes ten. There is no statistical mass.

The second feature is structured decision space. Insurance underwriting decisions can be reduced to a finite set of variables and outcomes. Fraud decisions can be classified into a handful of patterns. Customer service inquiries can be sorted into known categories. Private equity decisions, by contrast, span a vast and unstructured decision space. Every deal is different. Every management team is different. Every market dynamic is different. The patterns exist but they are subtle, contextual, and not reducible to a feature vector.

The third feature is tight feedback loops. An insurance pricing decision shows up in claims data within twelve to thirty six months. A fraud detection decision is validated within hours or days. A customer service routing decision is graded immediately by customer satisfaction signals. The model can learn from each decision quickly. Private equity, by contrast, has feedback loops that run five to seven years. The deal you do today produces signal in 2031. The model cannot learn from your decisions in any operationally useful timeframe.

The fourth feature is labeled training data. The easy industries have decades of labeled records that distinguish good outcomes from bad ones. Private equity does not. Most firms have hundreds of deals across their history, with outcomes that depend on so many confounding factors that simple labels do not capture what actually drove the result. The deal that returned three times the fund invested capital may have done so because the thesis was right, because the market was favorable, because the operating partner happened to be exceptional, or because of factors none of the contemporary records preserve. Untangling these confounds at scale is not what current AI can do.

The combination of low volume, unstructured decisions, long feedback loops, and unlabeled outcomes makes PE structurally less amenable to the techniques that have produced step changes elsewhere. This is not a criticism. It is a description of the terrain.

The Tacit Knowledge Problem

The deeper difficulty is that what makes a great private equity investor is not codifiable in the way that what makes a great underwriter is codifiable. The senior partner who has done deals for thirty years has accumulated something different from a structured rulebook. She has acquired pattern recognition that lets her, after a single management presentation, sense whether the team can execute. She has learned, from cycles of disappointment and surprise, which kinds of growth stories are durable and which dissolve under stress. She has developed a feel for when an industry's economics are about to shift. None of this lives in a document. None of it can be queried. None of it transfers to the next generation through training.

This is the tacit knowledge problem, and it sits at the center of why PE has resisted AI more than other industries. The most valuable knowledge inside a PE firm is the unwritten judgment that senior people have built through years of being right and wrong in expensive ways. AI systems trained on documents miss this knowledge entirely. AI systems trained on outcome data lack the volume and the labels to surface it. AI systems trained by interviewing senior people produce, at best, a thin caricature of what those people actually do.

The implication is uncomfortable. The most powerful asset inside a private equity firm cannot be straightforwardly captured, scaled, or automated by AI. It can be augmented. It cannot be replaced.

Figure: 32b what pe lacks

What This Means for the Roadmap

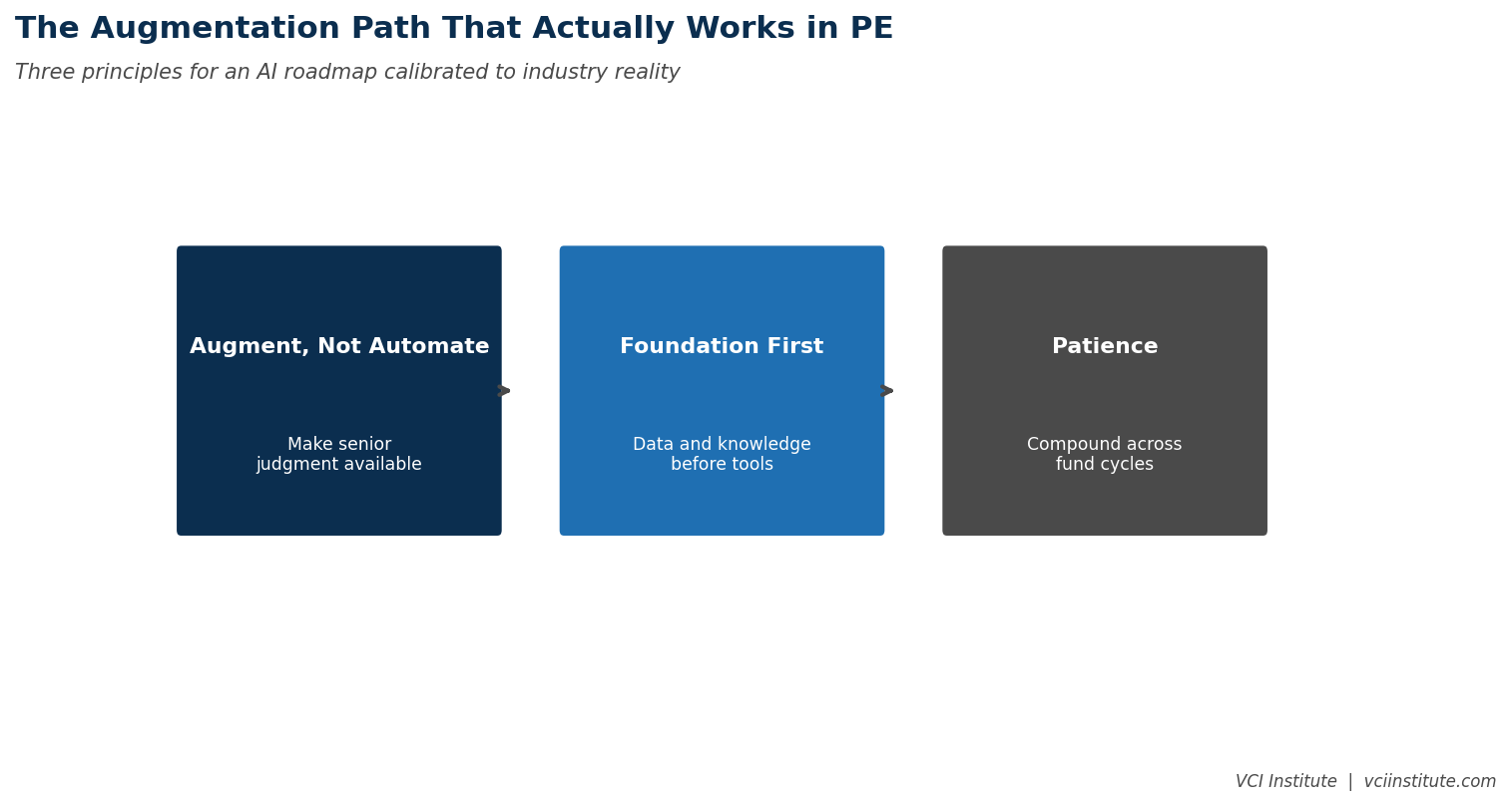

Recognizing the structural difficulty does not mean private equity should give up on AI. It means the roadmap has to be calibrated to what is actually possible rather than to what the vendors are promising.

The roadmap that fits the structural reality has three principles.

The first principle is augmentation, not automation. AI in PE works best when it makes senior judgment more available, more consistent, and more retrievable, not when it tries to replace senior judgment. The use cases that pay back are the ones that surface relevant historical context to a senior partner during a live decision, that compress the time it takes to find the relevant pattern, that bring the firm's accumulated reasoning to the moment when it would otherwise have been forgotten. The use cases that fail are the ones that try to make decisions autonomously in domains where the tacit knowledge is binding.

The second principle is foundation before sophistication. The unstructured nature of PE decisions means that the foundational data and knowledge work has to be unusually thorough. A firm that has not built a clean repository of past deals, past diligence, and past management assessments cannot meaningfully use AI for any decision support, because the substrate is too thin. The foundation work is unglamorous, slow, and expensive. It is also the prerequisite for everything else.

The third principle is patience. The feedback loops in PE are long. The benefit of any AI investment will not be visible for years. The firms that invest patiently, over multiple fund cycles, will accumulate compounding capability. The firms that demand quick wins will find that the quick wins do not exist in this industry, and will conclude prematurely that AI does not work for PE. The conclusion will be wrong, but it will be common.

What Has Worked and What Has Not

A few patterns are now visible across the firms that have made meaningful AI investments over the past three years.

What has worked. Document retrieval that finds the relevant precedent, contract clause, or historical analysis when a partner needs it. Drafting assistance for first drafts of standard documents that are then heavily edited by the senior team. Pattern surfacing in diligence that highlights the recurring red flags from past similar deals. Portfolio monitoring that aggregates standard operating metrics across companies and surfaces deviation. Investor relations support that drafts responses to standard LP inquiries with appropriate context. None of these are transformational. All of them save real time and improve consistency.

What has not worked. Autonomous deal sourcing or evaluation. Predictive models that try to forecast deal outcomes from structured features. Pricing recommendations for portfolio companies operating in unique competitive contexts. Strategic decision support for situations where the tacit knowledge is the binding constraint. Customer-facing AI in industries where reputational risk exceeds the labor savings. Most of these are not failing because the technology is bad. They are failing because the structural conditions PE operates in do not match what the technology is good at.

The honest assessment is that PE will see useful augmentation from AI over the next decade rather than transformational replacement. The firms that calibrate their expectations to this reality will deploy AI productively. The firms that expect transformation will overspend, underdeliver, and conclude that AI is overhyped, having missed the actual value because they were looking for a different one.

Figure: 32c augmented path

The Strategic Implication

For sponsors thinking about how to position their firms over the next decade, the structural difficulty of applying AI to PE is actually a kind of opportunity. The industries where AI works easily have already been substantially transformed. The competitive advantage from AI in those industries is largely arbitraged away. PE, because it is hard, is still a domain where disciplined, patient AI investment can produce real differentiation, because most competitors will either skip the work entirely or do it badly.

The firms that build the foundation, hire the knowledge engineers, document the tacit reasoning, and patiently augment senior judgment with retrieval and pattern surfacing will, by the end of the decade, have institutional capability that their competitors will find difficult to replicate. The capability will not show up in marketing materials. It will show up in the consistency of returns, the depth of diligence, the speed of conviction, and the reduction in unforced errors that compound across a fund cycle.

The firms that wait for AI in PE to become easy will find that, when it finally becomes easy, the firms that did the hard work first will already be operating two cycles ahead.

PE is the hardest industry to apply AI to. That is exactly why the firms that get it right will benefit the most. The discipline is in accepting the difficulty rather than denying it, and in calibrating the investment to what the industry actually allows rather than to what the vendor pitches imply. The roadmap is real. It is just not the one that has been marketed.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.