Cost Cuts That Build Versus Cuts That Bleed: The 2001 Recession Lesson PE Forgot

May 13, 2026

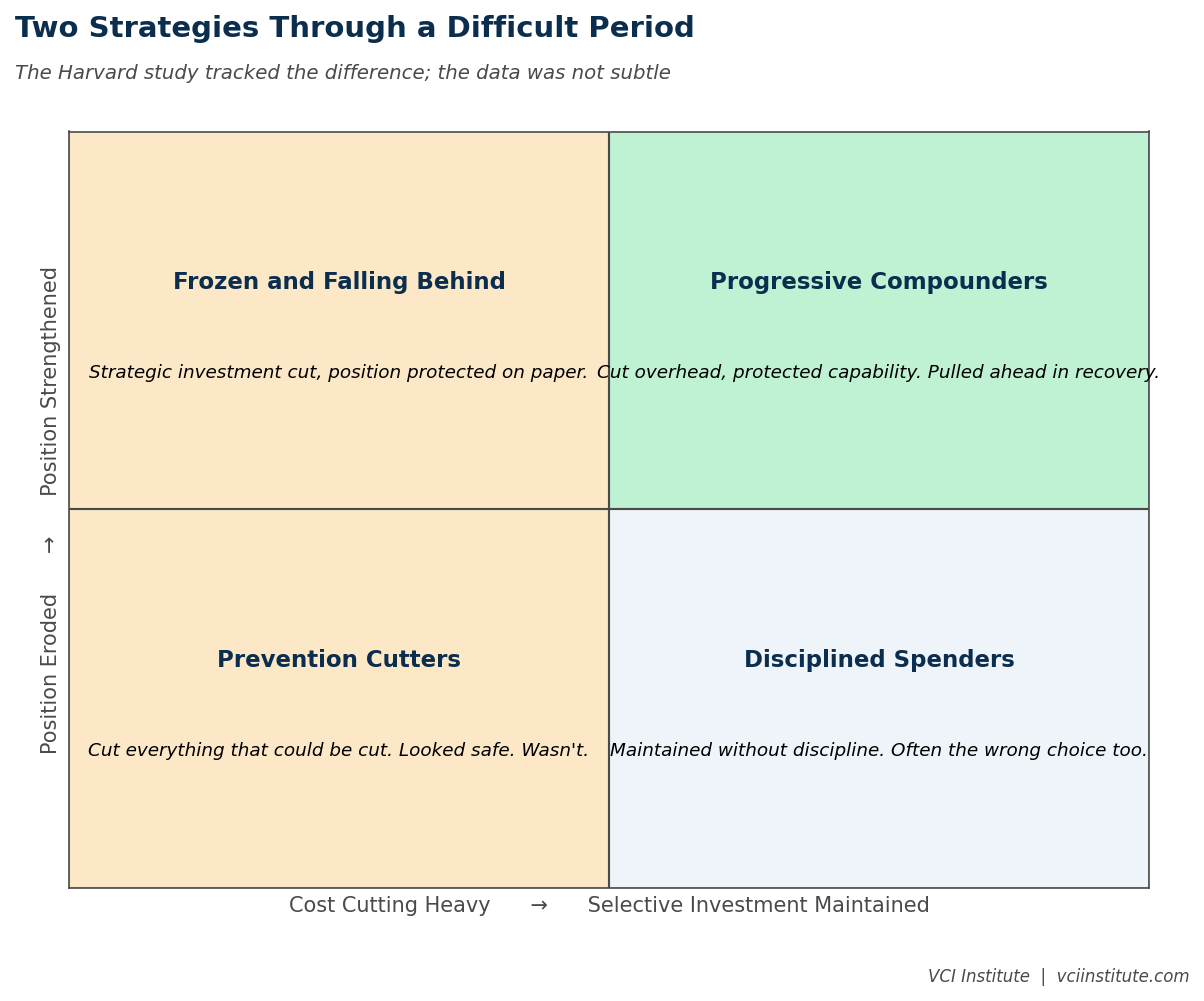

The 2001 recession produced a piece of research that should be required reading for every operating partner in private equity, and yet most have either forgotten it or never engaged with it carefully. The Harvard Business Review study tracked companies through the recession and the recovery and found a clear and uncomfortable pattern. Companies that responded to the downturn primarily through cost cutting fell behind during the recovery. Companies that maintained strategic investment alongside disciplined cost management pulled ahead.

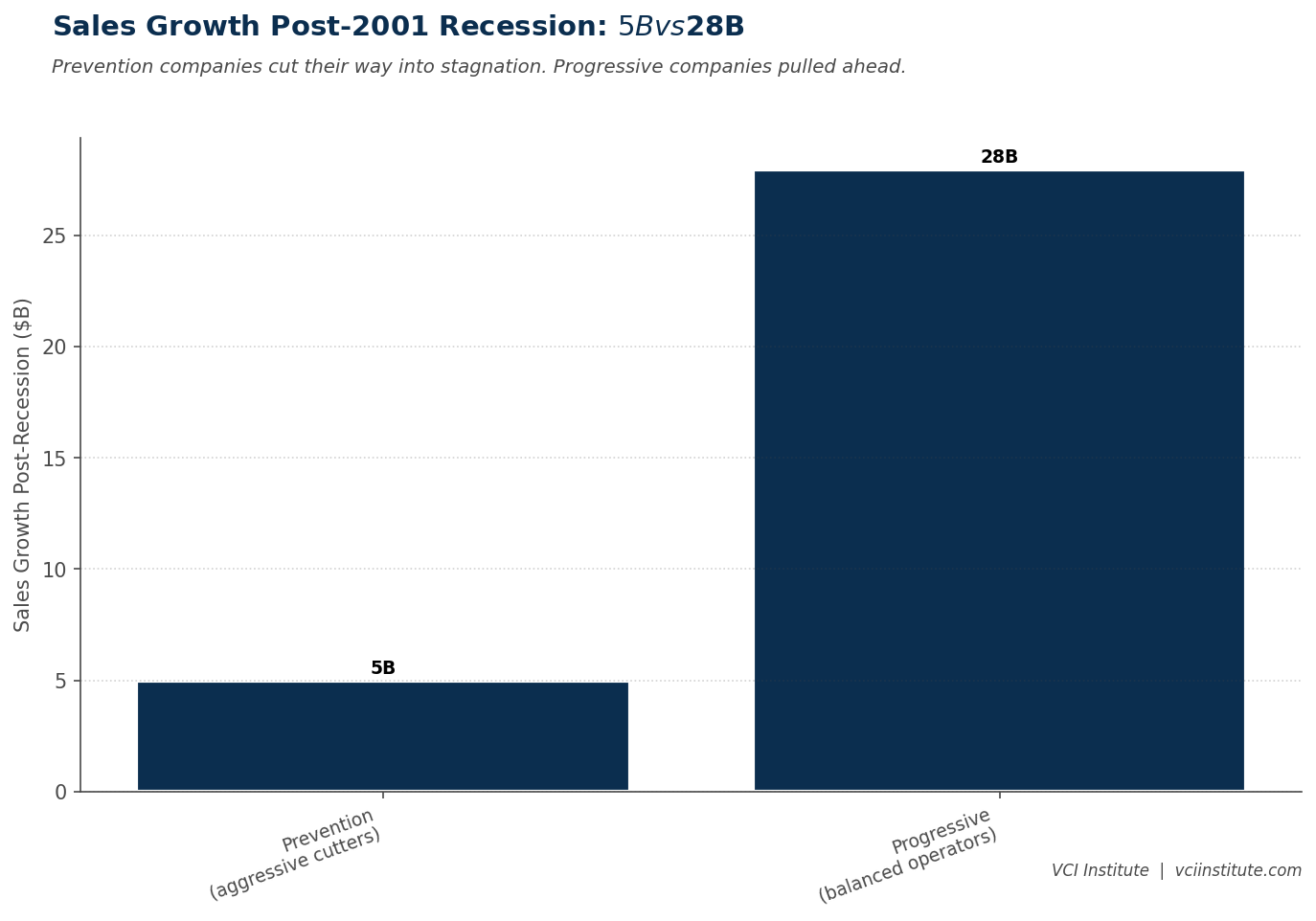

The numbers were not subtle. Prevention-focused companies, which prioritized aggressive cost cutting, grew sales by approximately five billion dollars after the recession. Progressive companies, which balanced cost discipline with strategic investment, grew sales by approximately twenty-eight billion. The gap was not five percent or fifteen percent. It was multiple times.

This research has not aged. The pattern has been replicated in subsequent downturns. The CEOs who freeze growth investment to manage through difficulty produce a posture that looks defensive and turns out to be value destructive. The CEOs who maintain selective investment alongside cost discipline produce a posture that requires more nerve and turns out to compound through the recovery.

Why the Pattern Recurs

The pattern recurs because of the specific mechanics of how cost cutting interacts with competitive position.

When a company freezes growth investment in a downturn, several things happen simultaneously. Sales capacity erodes as the company stops hiring and the existing team works without the support it needs. Marketing presence weakens as the company pulls back on customer acquisition. Customer experience degrades as service investments are deferred. Product development slows as research and engineering budgets are cut. Talent quality declines as the company stops attracting strong people and loses some of its best to competitors who are still hiring.

None of these effects show up immediately. They show up six to eighteen months later, when the recovery starts and the company discovers that it has lost competitive position relative to companies that maintained their investments. The lost position is then expensive to recover, sometimes prohibitively expensive. The cost cutter has saved money in the short term and sacrificed the asset that would have produced returns through the cycle.

The progressive company, by contrast, manages costs in the categories that do not affect competitive position while maintaining or even increasing investment in the categories that do. The result is a leaner overhead structure paired with continued strategic capability. When the recovery comes, this company is positioned to take share from the cost cutters who reduced the wrong things.

The math has been studied repeatedly. The conclusion is consistent. The challenge is that cost cutting is psychologically and politically easier than the disciplined balance the data supports.

What Private Equity Does Wrong

Private equity has a structural tendency toward the prevention pattern. The reasons are recognizable.

The first reason is that cost cutting produces visible results quickly. EBITDA improves in the next quarter. The board pack shows improvement. The deal team can report progress. The lift is real and immediate. Strategic investment, by contrast, produces results over multiple quarters or years. The board pack does not show the same kind of immediate improvement. The temptation to favor visible quick wins over slower compounding investments is strong.

The second reason is that the financial models in private equity have historically rewarded EBITDA improvement on a fixed timeline. The hold period is bounded. The exit valuation is a function of EBITDA at exit. Investments that produce returns beyond the hold period are not always credited in the model. This bias subtly favors cost cuts that produce immediate EBITDA over investments that produce longer-term competitive position.

The third reason is that operating partners under pressure to demonstrate value sometimes default to cost cutting because it is concrete and defensible. Walking into a board meeting with a cost reduction plan looks decisive. Walking into the same meeting with a measured argument for maintaining strategic investment alongside cost discipline requires more nerve and produces less visible activity. The structural pressures inside the firm reward the decisive cost cutter more readily than the disciplined balancer.

The combination of these three pressures produces, across the industry, a tendency to over-cut in difficult periods. The companies that emerge from the difficult period have weaker competitive position than they could have had. The exits that follow produce returns that are lower than a more balanced approach would have produced. The pattern is structural rather than individual, which is why it recurs even among sponsors who are aware of the research.

What Balance Actually Looks Like

The progressive pattern is not the absence of cost cutting. It is the discipline of cutting in the right places while protecting investment in the right places. The categorization is the work.

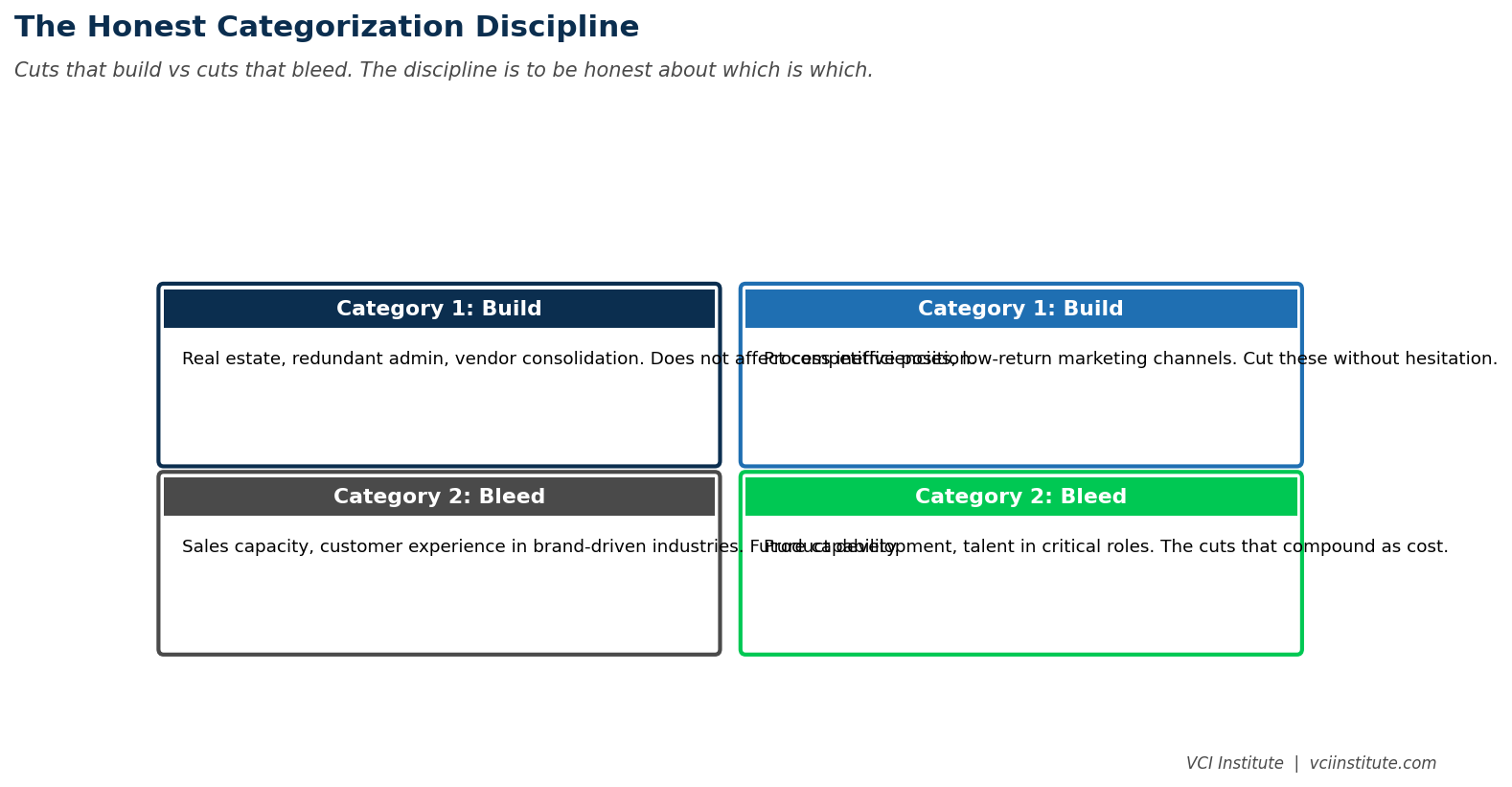

The categories where cost cuts generally produce value, even in normal times, include underused real estate, redundant administrative functions, low-return marketing channels, vendor consolidation opportunities, and process inefficiencies that have accumulated through growth. These categories represent costs that do not affect competitive position. Cutting them produces savings that compound through the cycle without weakening the business.

The categories where cost cuts generally destroy value, particularly in difficult times, include sales capacity in a downturn that will eventually end, customer experience in industries where the brand depends on it, product development in categories where competitive position is technology-driven, talent acquisition for critical roles where the labor market will tighten when conditions improve, and any investment that produces returns over multiple years rather than the current quarter. Cutting these categories produces immediate savings and compounding cost as competitive position erodes.

The discipline is to be honest about which category each line item sits in. The temptation is to claim that all cost cuts are in the first category, when in practice some are in the second. The honest categorization is uncomfortable because it requires admitting that some cost reductions are sacrificing future capability for current EBITDA. The honest categorization is also what distinguishes operators who manage through cycles from operators who optimize quarters.

A useful exercise. Take the list of cost reductions a portfolio company is considering. Force the team to categorize each one as either category one (does not affect competitive position) or category two (sacrifices future capability for current savings). Then ask whether the category two cuts are genuinely necessary to manage through the period, or whether they are being included because they are easier to make than the operationally smarter choice. The conversation that follows is what separates real cost discipline from blind cost reduction.

What Operating Partners Should Do Differently

Operating partners working with portfolio companies in difficult periods can apply three specific disciplines.

The first discipline is to insist on the honest categorization. Every cost reduction proposal should specify which category it belongs to. The aggregate of category two reductions should be capped at what is genuinely required to manage liquidity, with category one reductions doing the bulk of the work. Without this discipline, the path of least resistance leads to category two reductions that produce immediate visible savings and compounding cost over time.

The second discipline is to identify and protect the strategic investments that should not be cut. Sales capacity that the recovery will require. Talent in critical roles. Product development in categories where competitive position is technology-driven. Customer experience capabilities that drive retention. These investments should be named explicitly, protected through the difficult period, and reported on alongside the cost reductions. Their protection is the strategic discipline that the prevention pattern lacks.

The third discipline is to communicate the pattern explicitly to the management team. CEOs under pressure default to cost cutting because it is psychologically easier. The operating partner's role is to give the CEO permission to maintain disciplined investment alongside cost management, with the institutional backing to defend the choice when the board asks why investment levels have not been reduced. Without this backing, even sophisticated CEOs revert to the prevention pattern, because the political cost of maintaining investment without backing is higher than the political cost of cutting it.

The Long View

The 2001 recession lesson is not really about recessions. It is about how operators allocate resources under pressure. The pattern of over-cutting in difficult periods recurs in any environment where management teams are under pressure to demonstrate progress through visible activity. Private equity provides this pressure structurally, even outside formal recessions. The hold period creates a constant pressure to demonstrate EBITDA improvement. Each quarter requires evidence of progress. Each board meeting evaluates the trajectory. The structural pressure produces the same prevention bias that recessions produce, just in a more diffuse form.

The progressive pattern, applied not just to recessions but to private equity ownership generally, is the discipline of distinguishing cost reductions that build the business from cost reductions that bleed it. Most portfolio companies under PE ownership receive both kinds. The proportion varies based on how thoughtfully the operating partner has framed the choice for the management team. Operating partners who default to cost cutting produce companies that are leaner and weaker. Operating partners who insist on the honest categorization produce companies that are leaner and stronger. The difference shows up at exit.

The Harvard study has been available for two decades. The research has been replicated in subsequent cycles. The pattern is recognized in the academic literature and in the better-run firms in the industry. And yet the prevention bias continues to dominate the actual practice of cost management in mid-market private equity, because the structural pressures favor it and the discipline to resist it requires more nerve than most operators routinely deploy.

The operators who do deploy that nerve, consistently across deals, produce outcomes that compound favorably through cycles. The operators who do not produce a pattern of leaner companies that struggle to grow when conditions improve. The difference is not in the cost cutting. The difference is in what was protected while the cuts were happening. The 2001 lesson, if it is taken seriously, points operators toward the discipline that produces durable value rather than the discipline that produces visible quarters. The choice is available in every difficult period. The pattern of which firms make it well is, by now, predictable enough that LPs are starting to read it as a marker of quality. The lesson PE forgot is the lesson that, applied honestly, separates the firms that compound through cycles from the firms that optimize them.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.