Deal Team or Operating Partner: Two Trades That Look Similar and Are Not the Same Job

Apr 29, 2026

A common mistake in private equity hiring is to assume that the deal team and the operating partner team are doing variations of the same job. Both work on portfolio companies. Both engage with management teams. Both are accountable for value creation outcomes. Both report ultimately to the firm's senior leadership. The titles and the org charts often blur the boundary, and the compensation conversations sometimes treat the two roles as interchangeable.

They are not interchangeable. They are two different trades that look similar from a distance and require different reflexes, different time horizons, and different skill sets up close. Firms that treat them as interchangeable, that staff one role with people trained for the other, produce predictable patterns of underperformance. Firms that recognize the distinction and staff each role with people whose training fits, produce better outcomes across the board.

Figure: 35a two trades

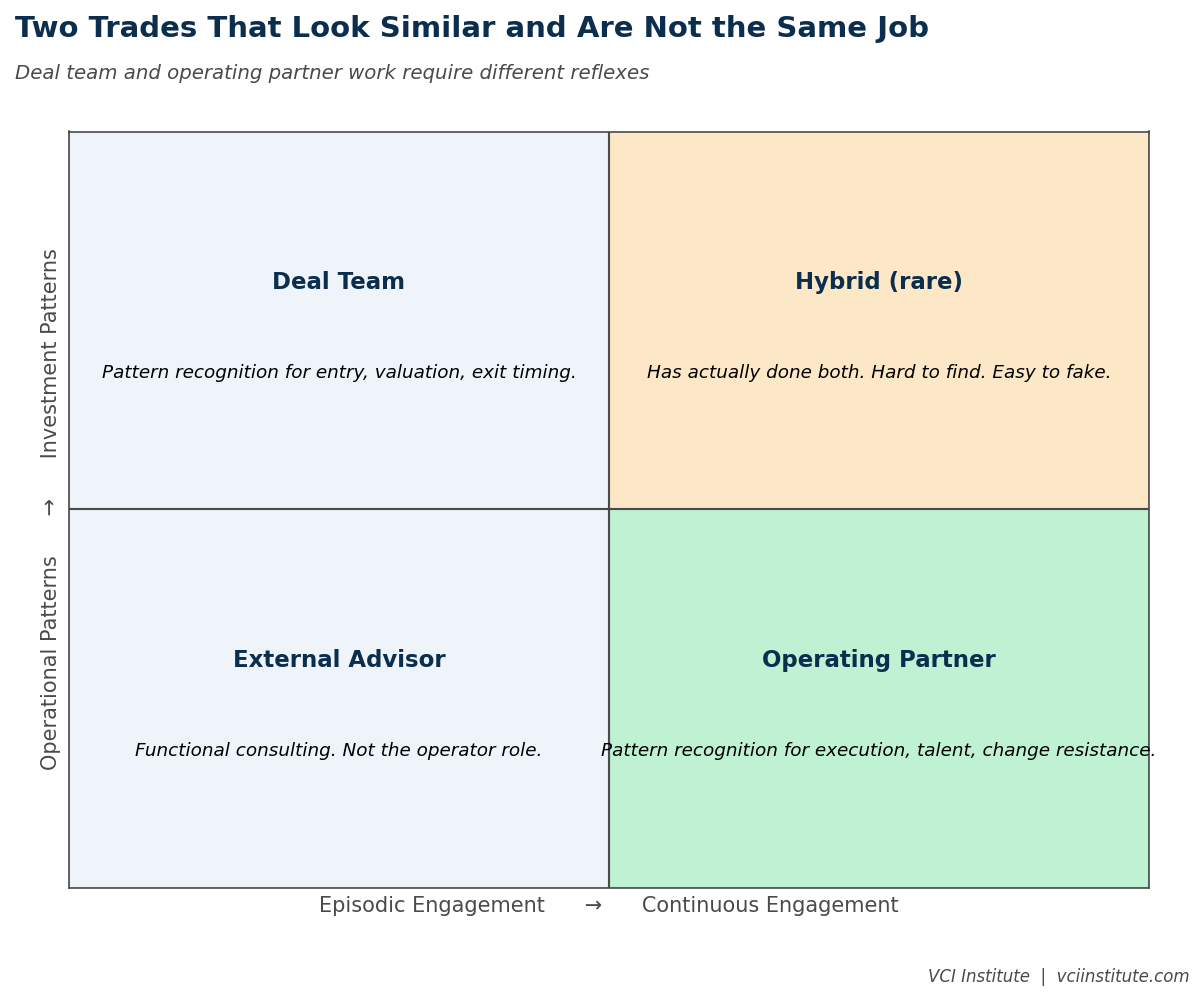

What the Deal Team Actually Does

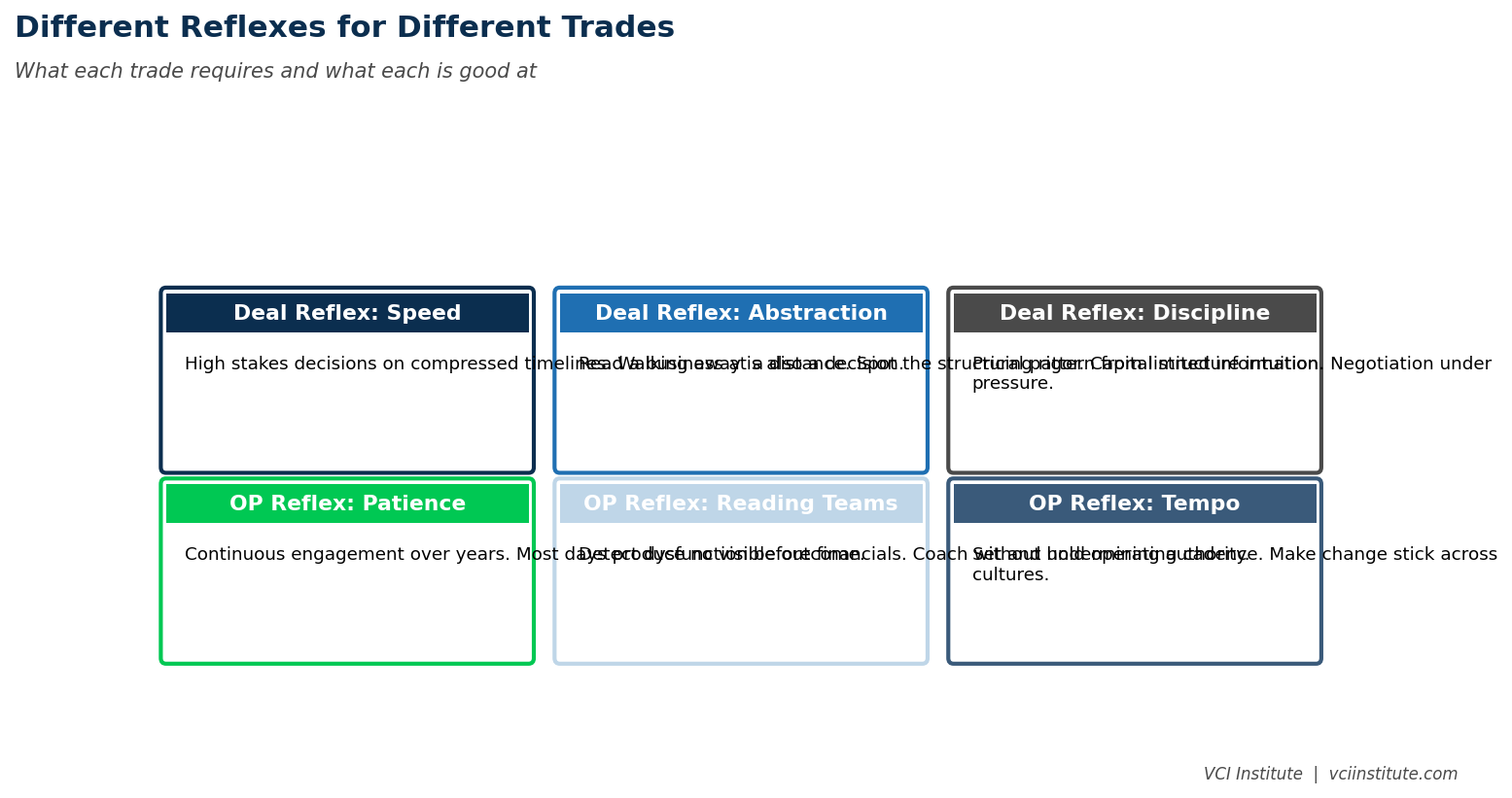

The deal team's trade is the trade of investment selection and structuring. The reflexes that matter are pattern recognition for entry dynamics, for capital structure, for valuation discipline, and for exit positioning. The time horizon is the lifecycle of the deal, from initial sourcing through eventual exit, with the most intense engagement at the front and the back of the cycle.

A deal partner is paid to make a small number of high stakes decisions extremely well. Whether to pursue a specific opportunity. Whether the price clears the firm's hurdle. What capital structure produces the best risk-adjusted return. When to commit and when to walk away. When to start the exit process. Which buyer to engage. The decisions are infrequent but consequential, and the cost of getting any one of them badly wrong is large.

The skills that produce this trade well are mostly analytical. Modeling discipline. Industry pattern recognition. Negotiation. Capital markets fluency. The ability to read a CIM critically. The ability to construct a fundable thesis from incomplete information. The ability to manage a competitive process without losing pricing discipline. These skills are usually developed through structured training programs, through apprenticeship under senior deal partners, and through repeated exposure to deal cycles. The training is recognizable. The career path is reasonably standard.

The cultural rhythm of the deal team is project oriented. Sprints of intense engagement during diligence and exit, alternating with periods of pipeline building and portfolio review. The team operates with significant autonomy on individual deals but with high accountability at the level of fund performance.

What the Operating Partner Actually Does

The operating partner's trade is the trade of execution inside portfolio companies. The reflexes that matter are pattern recognition for management effectiveness, for operating cadence, for change resistance, and for the gap between stated plans and lived reality. The time horizon is continuous and unfocused, with engagement that spans years of portfolio company hold rather than the discrete events of acquisition and exit.

An operating partner is paid to make a much larger number of smaller decisions, most of them not visible to the deal team and many of them not visible to the management team either. Whether the CFO can grow into the role. Whether the new COO understands the operating reality of the business. Whether the customer concentration risk is being addressed or papered over. Whether the management team is learning from the previous quarter's miss or just rationalizing it. Whether the value creation plan is on track or has quietly drifted into a different plan that nobody has named yet.

The skills that produce this trade well are mostly relational and observational. The ability to read a management team in real situations rather than in scripted presentations. The ability to coach a CEO without undermining her authority. The ability to identify operational dysfunction before it appears in the financials. The ability to drive change in cultures that resist it without producing the kind of conflict that destroys the change effort. The ability to work effectively with a CEO who would rather not have an operating partner involved at all. These skills are not produced by analytical training. They are produced by years of running businesses, working closely with executives under pressure, and accumulating the kind of pattern recognition that only comes from being in the operational mess repeatedly.

The cultural rhythm of operating partners is sustained engagement. Weekly or biweekly contact with each portfolio company. Monthly board engagement. Quarterly deep dives on specific issues. The team operates with less individual autonomy than the deal team but with broader awareness of patterns across the portfolio.

Figure: 35b reflex comparison

What Goes Wrong When Firms Confuse the Roles

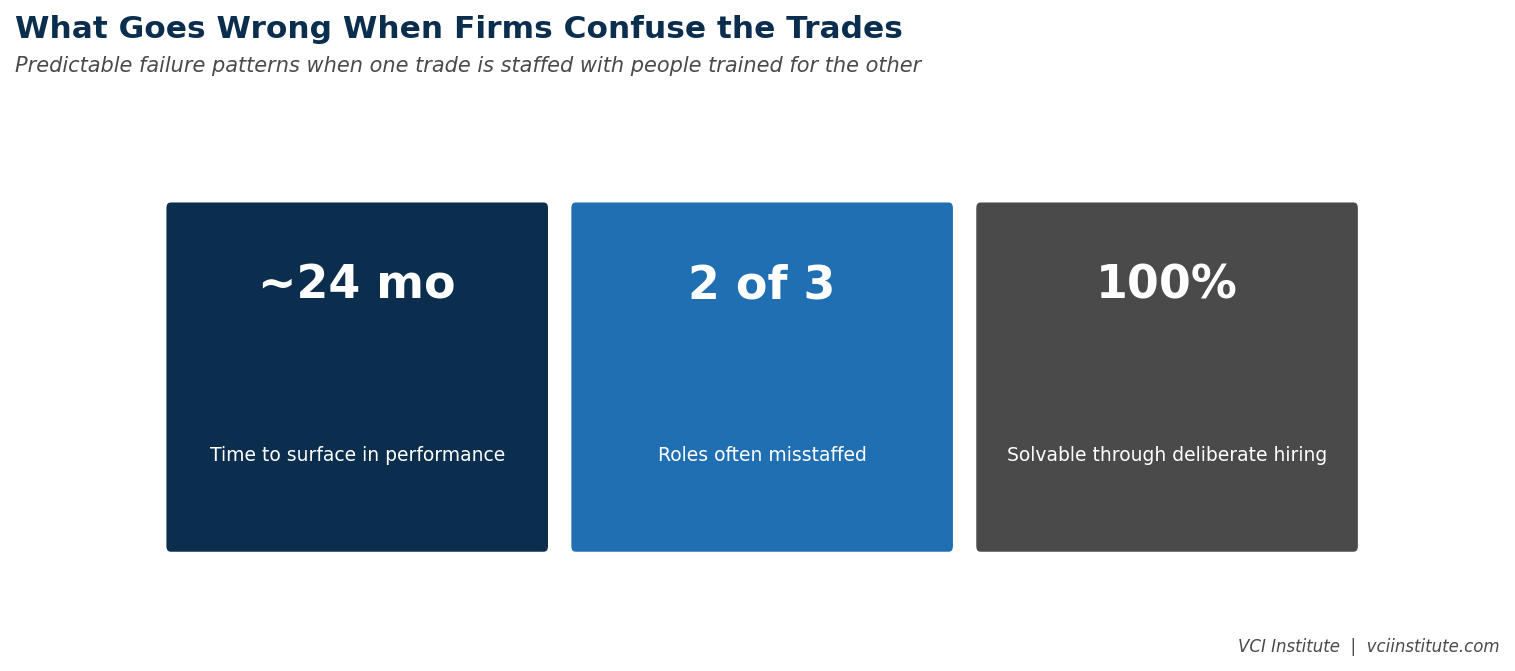

Firms that treat the two roles as interchangeable produce two specific failure patterns that recur with predictable consistency.

The first pattern is staffing operating partner roles with people whose training was on the deal side. The hire makes intuitive sense to the firm because the person has investment experience, understands the business model, and is fluent in the firm's culture. The hire fails operationally because the person has not actually run a business at scale, has not built a management team, has not driven change against organizational resistance. The reflexes that produced strong deal outcomes do not transfer to the work of execution inside a portfolio company. The new operating partner runs the role as if it were an extended diligence engagement, producing analyses and recommendations but not driving the operational outcomes the deal thesis requires.

The second pattern is staffing deal team roles with people whose training was on the operating side. The reverse mistake. A successful operator who has built and run businesses joins the deal team and struggles with the speed, the abstraction, and the analytical density of investment work. The instincts that drove operational excellence do not translate to the work of evaluating opportunities at speed across a wide pipeline. The deal team gradually filters out the operator's contributions, and the firm has effectively paid for capability it cannot use.

Both patterns share a root cause. The hiring decision was made on the assumption that the trades were similar and that strong performance in one would transfer to the other. The assumption is wrong. The trades use overlapping vocabulary but require different reflexes that are developed through different paths. Strong performance in one is, at best, weakly predictive of performance in the other.

The Hybrid Profile and Its Limits

There are people who have done both trades well, but they are rare. The career path that produces a credible hybrid usually involves significant time on the operating side first, followed by deliberate cross-training on the deal side, followed by years of doing both. Most firms do not have the patience or the bench depth to develop hybrids deliberately.

The risk in pursuing hybrids as a default hiring strategy is that most candidates who claim hybrid backgrounds have actually done one trade well and dabbled in the other. The dabbling does not produce the reflexes. A deal partner who has served on a portfolio company board for two years has not actually run the business. An operator who has worked on a few diligences has not actually evaluated capital structure choices at speed. The credentials look hybrid. The capability is mostly one-sided.

Firms that need genuine hybrid capability should usually accept that hybrids are exceptions and staff each role primarily with specialists. The team coordination then becomes the source of integrated capability, rather than expecting individual people to embody both trades.

The Coordination Question

If the two trades are genuinely different and most people do one or the other well, the question becomes how to coordinate them effectively. This is the actual operating model question that firms should be asking, rather than the staffing question they often ask instead.

The coordination model that works has three features.

The first feature is shared upstream involvement. Operating partners participate in the deal cycle from sourcing through close, not just in execution after close. The participation does not require operating partners to do deal team work. It requires them to bring operating perspective to investment decisions before commitment. This is the pre-LOI involvement that the most sophisticated firms now build in. The deal team retains decision authority. The operating partner contributes the operational read that sometimes changes the deal team's view.

The second feature is shared accountability for outcomes. Both teams are accountable for fund performance, with structures that prevent the deal team from claiming credit for what the operating partner delivered or the operating partner from blaming the deal team for what should have been executed. The compensation structures matter here. Carry parity sends a real signal about whether the firm treats both roles as equally important to outcomes.

The third feature is mutual respect rooted in genuine understanding of what each role contributes. The deal team understands that operational execution is hard, longer term, and not reducible to a project plan. The operating partner understands that investment selection is high stakes, requires speed, and does not always allow the time for the operational depth she would prefer. Each trade learns to respect what the other does without trying to do it themselves.

Figure: 35c role clarity

What This Means for Firm Building

For sponsors building or refining their firms, the implication is to be deliberate about staffing each role with the right kind of person, and to build the coordination model that integrates them rather than expecting individuals to bridge the gap.

For deal team hires, prioritize analytical depth, capital markets fluency, and structured pattern recognition. The career path is mostly investment-focused. Operational exposure is useful as context but not as primary qualification.

For operating partner hires, prioritize lived operational experience, relational sophistication, and pattern recognition built from running businesses through cycles of pressure. The career path is mostly operational. Investment exposure is useful as context but not as primary qualification.

For coordination, build the structures that integrate the two trades at the moments where integration produces value. Pre-LOI involvement. Joint quarterly portfolio reviews. Shared annual planning. Honest debriefs of completed deals that draw on both perspectives. The coordination is the source of integrated capability, not the expectation that any individual person will embody both trades.

Firms that get this right end up with stronger operating partner teams, stronger deal teams, and better coordination between them. Firms that get this wrong end up with mediocre versions of both, because they hired people who looked like they could do both jobs but actually did neither well. The mistake is correctable. The first step is recognizing that the two trades are different jobs that look similar from a distance, and that the distance is exactly what makes the confusion so common in an industry that has not yet been forced to articulate the difference clearly.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.