The 100-Day Autopsy: Why Most Value Creation Plans Stall by Day 90

Jun 11, 2026

The 100-day plan is one of the most universally adopted, universally underperforming artifacts in private equity. Every fund has one. Every IC memo gestures at one. Every operating partner is handed one on day one of close. And yet, when we go back and look at what actually happened during the first hundred days of any given deal, the gap between the plan as documented and the work that actually got done is consistently large.

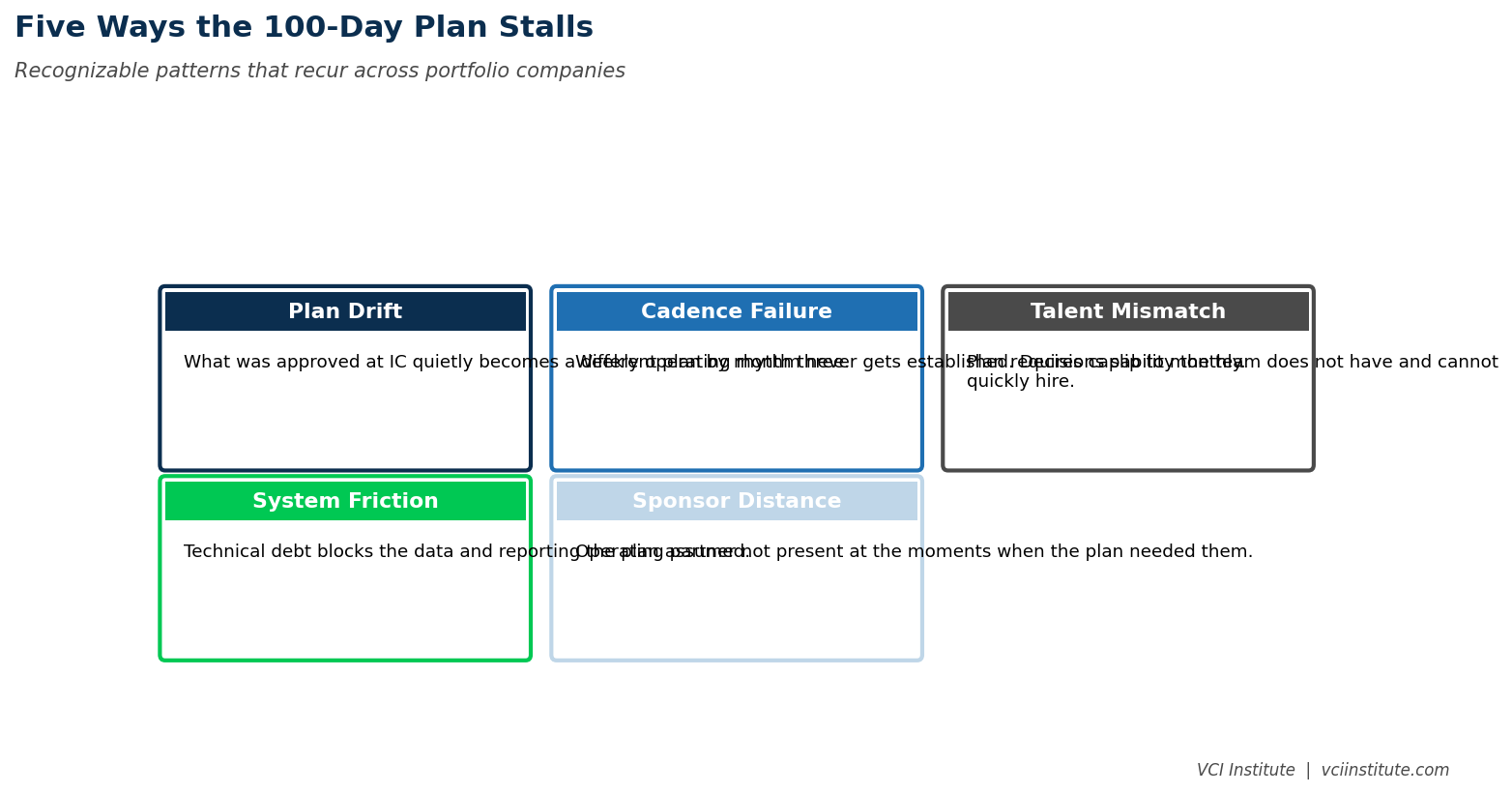

The failures rarely come from a lack of effort. They come from predictable, repeating patterns that are easier to see in retrospect than to prevent in real time. After looking across dozens of post-close diagnostics, we have found that nearly every stalled hundred day plan fails along one or more of four lines.

Failure Mode One: The Plan Was Written Before Anyone Knew the Business

The first failure mode is the one most people will not say out loud. The hundred day plan was largely written before close, by a team that had access to data rooms and management presentations but had never spent significant time inside the business. The plan reflects the deal team's hypothesis about the company, not a tested view of how the company actually runs.

This is structurally unavoidable. The deal team has to write something. The IC requires it. The LP reporting cycle assumes it. The operating partner who arrives at close is then asked to execute a plan built on assumptions she had no chance to challenge before signing.

The diligence period gives the deal team perhaps eight weeks of intensive engagement with the target. Most of that time is spent on financial validation, market sizing, and customer references. Very little of it is spent inside the operating system of the business. By the time close happens, the deal team has a confident view about market opportunity and a fragile view about what it will take to capture it. The plan reflects the confident view. Reality reflects the fragile one.

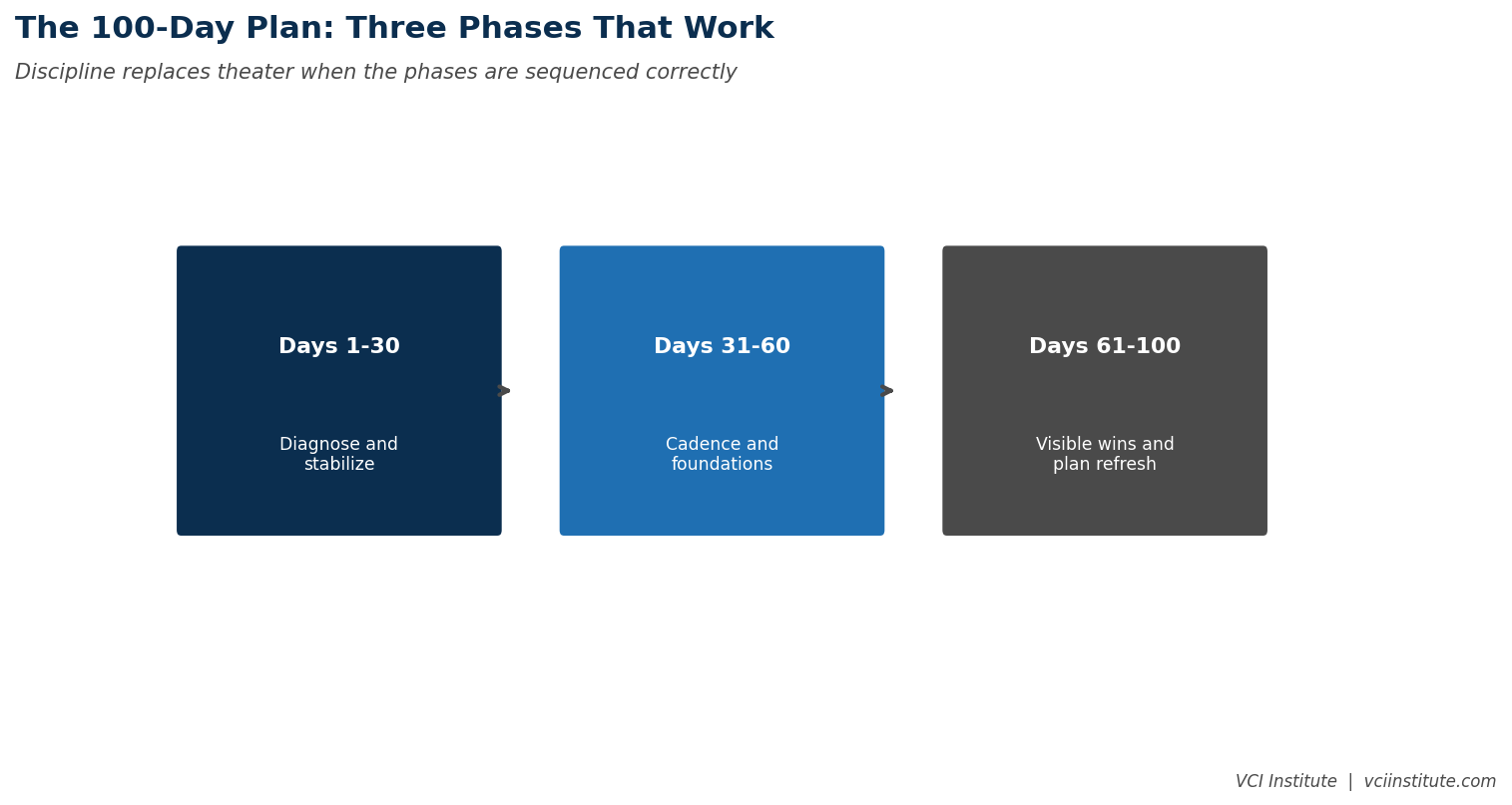

The fix is to treat the first thirty days after close as a learning sprint, not an execution sprint. The plan should be explicitly redrafted between day twenty and day forty, after the operating team has spent meaningful time inside the company. The redraft is not a confession of failure. It is the moment when the plan converts from hypothesis to thesis. Firms that resist this redraft, because the original plan was approved at IC, end up executing the wrong plan with discipline. That is worse than executing a corrected plan with imperfect discipline.

Failure Mode Two: The Plan Has Too Many Initiatives

The second failure mode is initiative inflation. The hundred day plan, as approved by the IC, contains forty or fifty workstreams. Revenue initiatives. Cost initiatives. Procurement initiatives. Pricing initiatives. Talent initiatives. Systems initiatives. ESG initiatives. Customer experience initiatives. Each one looks small in isolation. Together they add up to a backlog that no real management team could deliver while also running the business.

The first symptom is that everything moves at the same slow pace because the management bandwidth is divided forty ways. The second symptom is that low priority initiatives consume the attention of people who should be focused on the two or three things that actually drive the value creation thesis. The third symptom is that nothing finishes, because every workstream is between thirty and sixty percent complete at any given moment.

Effective hundred day plans have between five and seven workstreams. Not forty. The five to seven are chosen because they directly support the value creation thesis, not because they appeared in a McKinsey decklet two years ago. Anything beyond the seven gets added to a backlog and rotated in only as bandwidth opens up.

The discipline here is brutal. Sponsor teams that are uncomfortable saying no to good ideas end up with bloated plans. Sponsor teams that understand bandwidth as a constraint end up with focused plans. The difference shows up in execution velocity, which over a year becomes the difference between a value creation plan that compounds and one that drifts.

Failure Mode Three: The Wrong People Are Running the Plan

The third failure mode is execution leadership. Hundred day plans require dedicated execution capacity. The CEO has a business to run. The CFO has financial close cycles to manage. The COO has operations to keep moving. None of them have the bandwidth to also run a hundred day plan as a side activity, even though that is exactly what often happens.

The visible symptom is that workstream owners hold weekly status meetings, produce slides, and make modest progress. The invisible symptom is that the workstream owners are operating as project managers rather than as decision makers. They report status. They flag issues. They wait for someone else to remove blockers. The plan does not advance because the people running the workstreams do not have the authority or the bandwidth to push through resistance.

Strong sponsors solve this by deploying dedicated execution capacity. Sometimes this is an external transformation lead. Sometimes it is an internal operating partner who spends meaningful time on site. Sometimes it is a chief of staff role created specifically for the hundred days. Whatever the model, there is a person whose primary job is to drive the plan, with the political backing of the sponsor, the bandwidth to focus, and the authority to make decisions when the management team is divided.

Without that person, the hundred day plan becomes a document that gets reviewed monthly until the energy fades.

Failure Mode Four: There Is No Cadence, Only Reporting

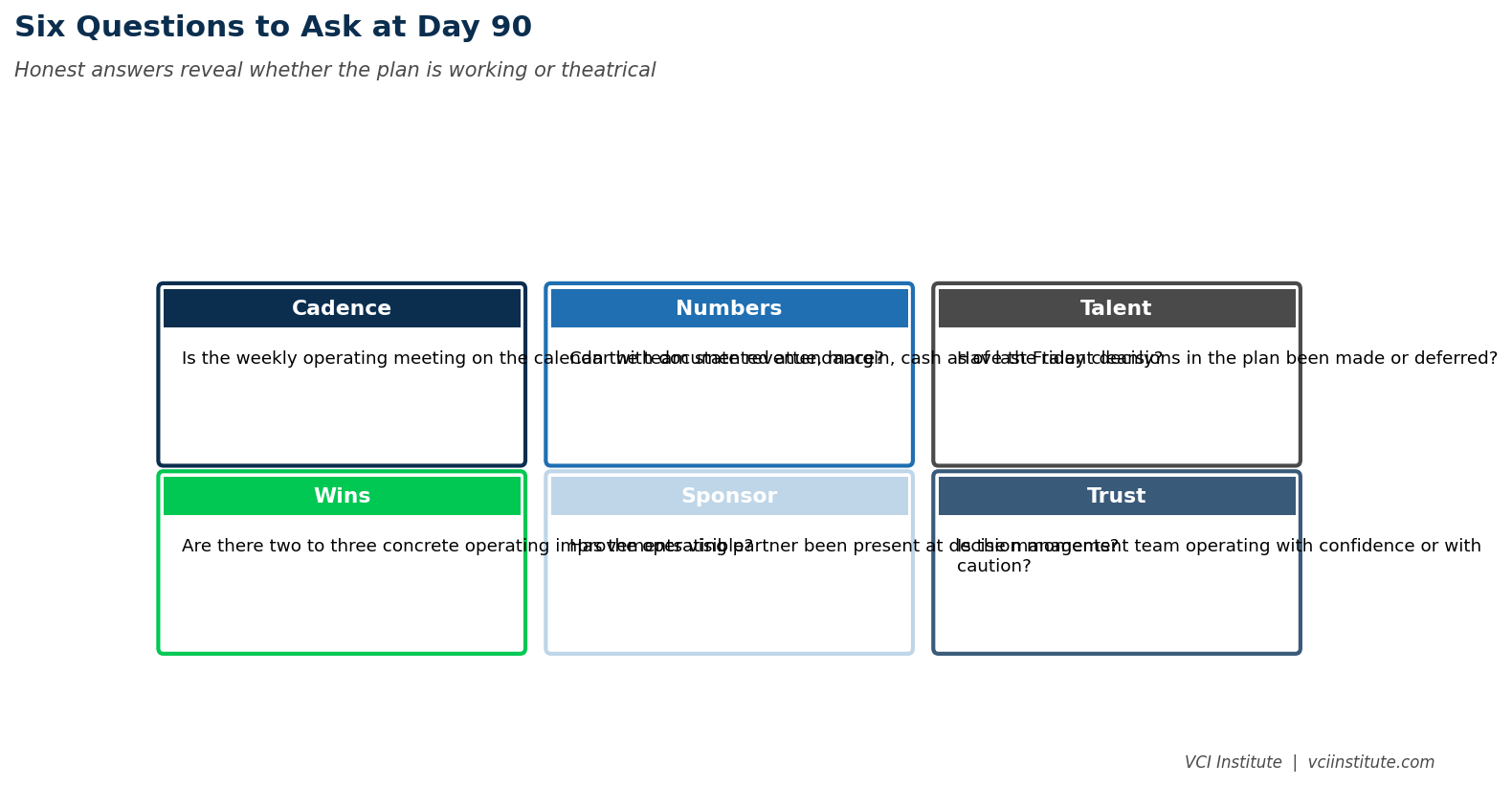

The fourth failure mode is the one that hides in plain sight. The plan has a governance structure on paper, including weekly check-ins, monthly steering committees, and quarterly board reviews. In practice, these meetings degenerate into reporting sessions where workstream owners describe what they did and the sponsor team listens. There is no real decision making. There is no real escalation. There is no real reallocation of resources when something is failing.

A reporting cadence is not the same thing as an operating cadence. A reporting cadence asks what happened. An operating cadence asks what we are going to do about what happened. The first leaves the plan running on its existing trajectory. The second changes the trajectory based on what is being learned.

Effective hundred day governance has three layers. The weekly cadence is short, action oriented, and brutal in surfacing blockers. The monthly cadence rebalances resources across workstreams based on what is and is not working. The quarterly cadence is when the plan itself is allowed to be modified, not just executed. Each layer makes a different kind of decision. Without all three, the plan runs on autopilot until it crashes into reality at month six.

What a Good 100-Day Plan Actually Looks Like

A good hundred day plan is short. It fits on five pages, not fifty. It identifies the three to five workstreams that materially advance the value creation thesis, not the comprehensive list of every improvement opportunity that exists in the business. It assigns an owner with bandwidth and authority to each workstream. It defines what success looks like in concrete, measurable, time-bound terms, not in aspirational language.

A good plan also has a section that openly names what is not being done. Initiatives that are sensible but not currently funded. Improvements that are deferred to phase two. Capabilities that are missing but cannot yet be built. The discipline of explicitly deferring things is what protects the bandwidth of the things being delivered. Plans that include everything end up delivering nothing.

A good plan finally has a learning section. What we believed at close. What we have already learned to be different. What we will need to revise if certain assumptions prove wrong. This is the section that almost no formal hundred day plan contains, because it requires sponsors and management teams to admit, in writing, that some assumptions might be wrong. The plans that include this section end up more accurate at day ninety. The plans that do not include it end up generating the divergence that creates the autopsy.

The Pre-Mortem Habit

The simplest practice that prevents most of these failure modes is the pre-mortem. Before the plan is approved, the sponsor team and the operating team sit in a room and ask one question. It is now day ninety. The plan has stalled. What went wrong. The team brainstorms the failure modes openly. The output is a list of risks the plan has to address, by design, before execution begins.

A pre-mortem run honestly will surface every one of the four failure patterns above, plus a few that are specific to the business in question. The plan then gets revised to anticipate them. The pre-mortem takes about three hours. It saves between thirty and sixty days of wasted execution. It is one of the highest return interventions available to any operating partner.

Most sponsors skip the pre-mortem because it feels like it slows down the plan. In reality it accelerates it. The plan that survives a pre-mortem is structurally tougher than one that did not. The plan that did not survive a pre-mortem will encounter the same questions in execution, except by then the cost of being wrong is much higher.

What Happens at Day 100 If You Get This Right

Sponsors who address the four failure modes at the start of the hundred days arrive at day one hundred with a different deliverable than most of their peers. They have a small number of completed workstreams that have demonstrably moved the business. They have a clear picture of what is and is not working in the value creation thesis. They have a management team that has been stress tested under pressure and either earned its position or revealed gaps that need filling. They have the data hygiene foundation that the next phase of the plan can build on.

This is the difference between a hundred day plan that produces momentum and one that produces a report. The plan does not have to do everything. It has to do a few important things well, in a way that compounds into the next phase of the hold. Operating partners who understand the autopsy patterns make this difference deliberately. Those who do not, write the same plan their peers did, get the same outcome, and discover the gap only when it is too late to close cheaply.

The hundred days are short. The patterns are predictable. The discipline is unglamorous. And the outcome shows up in the IRR of the deal three years later, even if nobody connects it back to a Tuesday in week three when the sponsor decided to redraft the plan instead of executing it as written.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.