The AI Ceiling: Why Tooling Keeps Outpacing the Operating Model

Jul 13, 2026

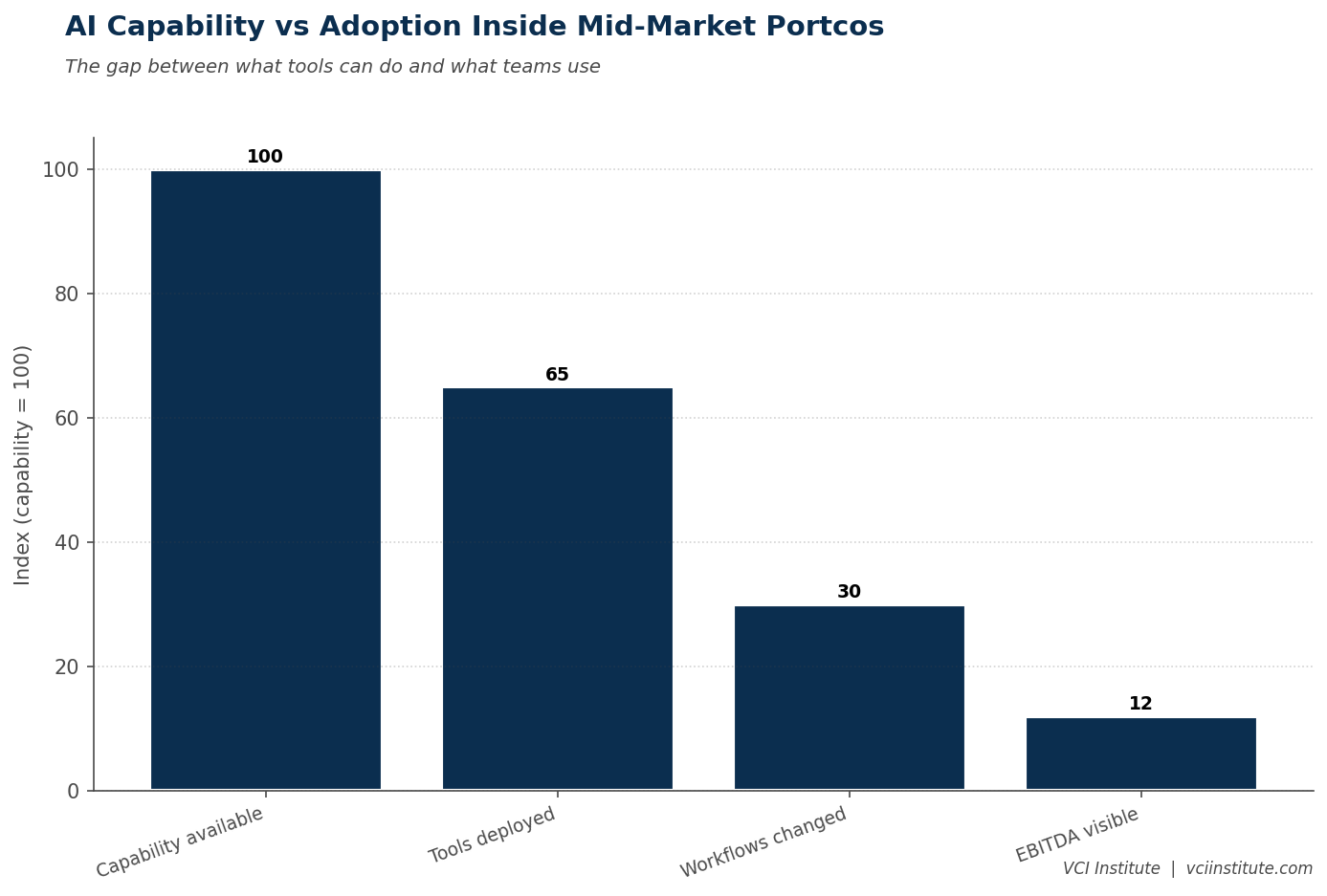

The AI capability of available tools has improved by an order of magnitude over the past three years. The AI absorption capacity of mid-market portfolio companies has improved by perhaps thirty percent over the same period. The gap between the two, growing each quarter, is the AI ceiling.

Most operating partners experience the ceiling in the same way. They sign the contract for a powerful new platform. They preside over a successful pilot. They sponsor a rollout plan. Then the deployment runs into a wall. Adoption stalls. Use cases that worked in the pilot do not propagate to the broader user base. The platform's full capability sits unused while the portfolio company pays the full subscription cost. The quarterly review meetings turn into apologetic explanations from management about change management challenges, training needs, and adoption headwinds.

The ceiling is not a temporary phenomenon. It is the structural condition of the moment. The tools have outpaced the operating models inside the businesses that own them. Until the operating models catch up, additional tooling will produce diminishing returns.

What the Ceiling Actually Is

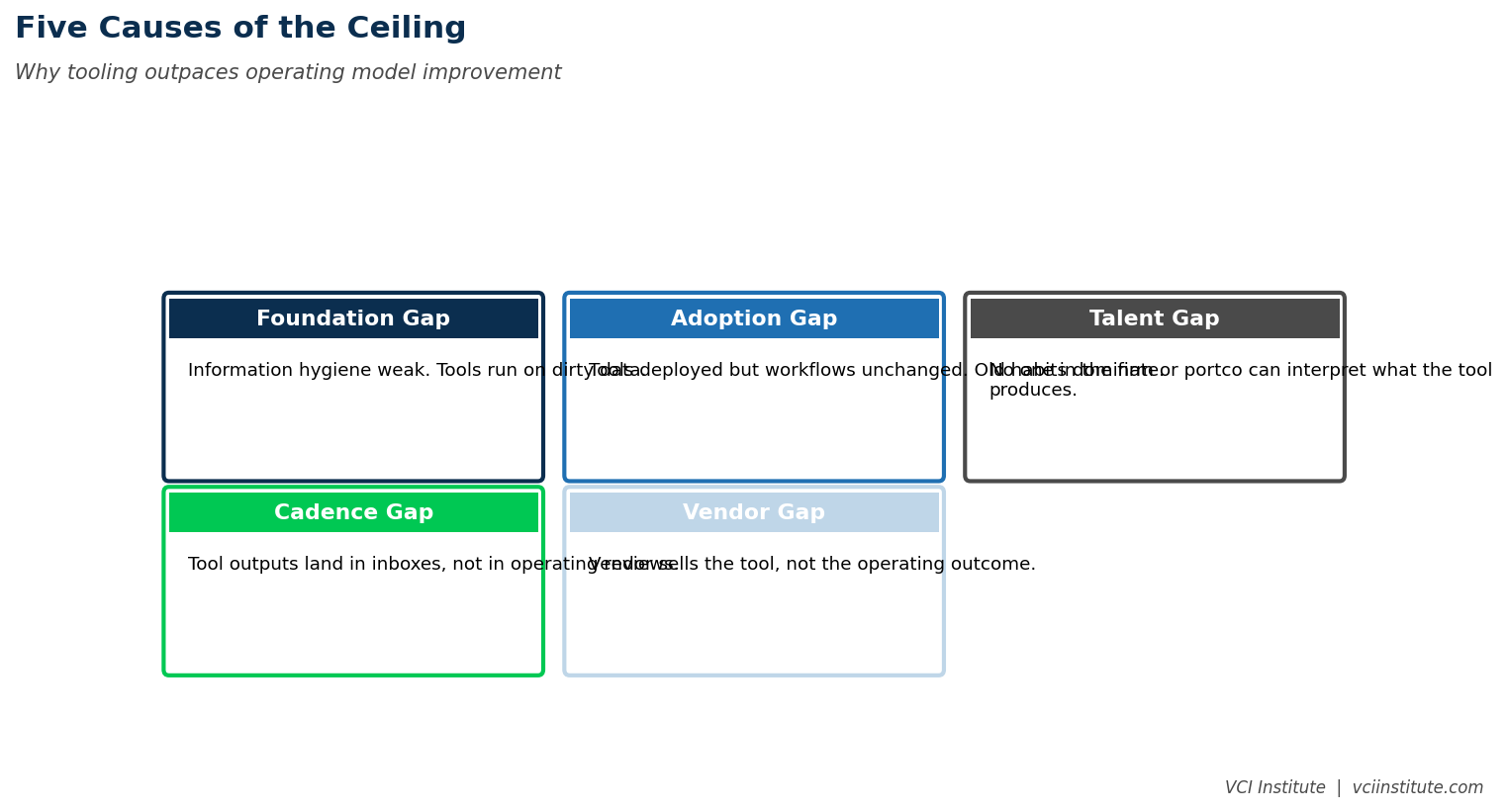

The ceiling has four components. Each one limits how much of a tool's capability the business can actually use. A diagnostic that examines all four reveals where the binding constraint is and what it would take to relax it.

The first component is data quality. AI tools amplify whatever data is fed into them. If the data is accurate and complete, the tool produces accurate, useful outputs. If the data is patchy, inconsistent, or out of date, the tool produces outputs that look confident but are wrong, undermining user trust and reducing adoption. Many ceiling problems are really data quality problems wearing the mask of adoption problems.

The second component is process maturity. AI tools work best when they are inserted into workflows that have known steps, known decision points, and known handoffs. When the underlying process is informal or varies by individual, the tool either gets ignored or gets used in ways that bypass its intended design. The tool's capability exceeds the organization's ability to plug it into structured work.

The third component is talent absorption. AI tools require users who can prompt effectively, evaluate outputs critically, and integrate the outputs into their work judgment. These are real skills. They are not innate. Mid-market workforces typically have between five and fifteen percent of users who acquire these skills quickly, another thirty to forty percent who acquire them with focused training, and the rest who do not engage meaningfully with AI tools at all without sustained intervention. The talent distribution sets the realistic upper bound on absorption.

The fourth component is governance maturity. AI tools introduce new categories of risk. Confidentiality exposure when proprietary information is used in prompts. Compliance exposure when AI generated outputs are used in regulated communications. Liability exposure when AI recommendations are followed without human judgment. Mid-market companies usually do not have the governance infrastructure to manage these risks, and either deploy tools without managing the risks at all or deploy them so cautiously that adoption is suppressed.

When all four components lag the tooling investment, the ceiling is severe. When all four are aligned with the tooling, the ceiling is high enough that adoption issues become rare. Most mid-market portfolio companies are somewhere in the middle, with one or two components binding harder than the others.

How Operating Partners Hit the Ceiling

The pattern is consistent across portfolio companies. The first AI tool gets deployed. It works. The pilot produces measurable benefit. The team is excited. A second tool gets approved. It also works, in pilot. A third gets approved. By the third or fourth tool, the cumulative deployment has exceeded the absorption capacity of the organization, and the marginal benefit of each new tool starts to fall sharply.

The symptom is that adoption metrics for the newest tools are weaker than those for the earlier ones. Users complain about tool fatigue. Training sessions are sparsely attended. The CIO points to license utilization data showing that the third and fourth tools are seeing limited use. The CFO asks why technology spend is increasing faster than the productivity benefits of the prior wave have stabilized.

This is the ceiling becoming visible. The business has reached the limit of what its current operating model can absorb. Adding more tools at the same pace will increase costs without producing proportional benefit.

Operating partners who recognize the pattern early reframe the AI investment from tooling acquisition to absorption capacity expansion. The next investment is not another platform. It is in the components of the operating model that are limiting how much the business can use what it already owns.

What Lifts the Ceiling

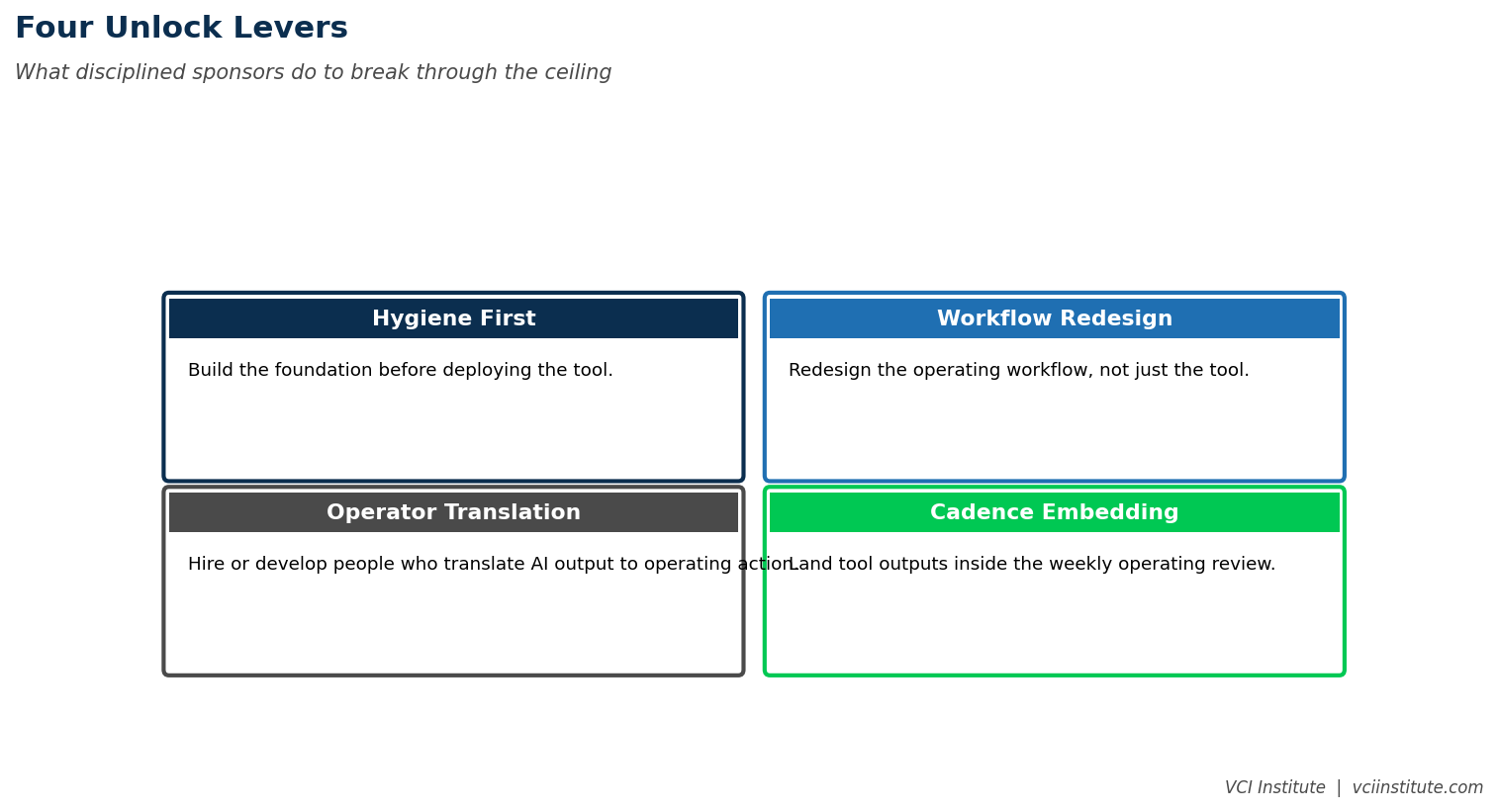

Lifting the ceiling requires investment in the components that are binding. The right investment depends on the diagnosis. Three patterns appear most often.

The first pattern is data foundation lift. When data quality is the binding constraint, the right next investment is data infrastructure rather than additional AI tools. Master data hygiene. Integration between core systems. Reporting automation that produces canonical numbers. Companies that complete this work find that their existing AI tools suddenly produce better outputs, because the inputs improved. Adoption recovers without any change in tooling. The same money spent on a new platform would have produced less benefit than the same money spent on cleaning up the foundation.

The second pattern is workflow design lift. When process maturity is the binding constraint, the right investment is in workflow design and documentation. What does the customer onboarding process actually look like, step by step. Where does the AI tool fit in. What does the user do with its output. What is the next step. Companies that complete this work find that the same AI tool, deployed against a designed workflow rather than an informal one, produces dramatically higher adoption and clearer benefit. The investment is unglamorous. The return is large.

The third pattern is capability lift. When talent absorption is the binding constraint, the right investment is in user enablement that goes beyond standard training. Identifying and cultivating internal champions. Creating peer learning networks where successful users share patterns with less skilled colleagues. Building role specific use case libraries that reduce the friction of figuring out how to use the tool. Embedding AI capability directly into the performance evaluation framework so that demonstrated AI fluency is part of how individual contributors are assessed. Companies that complete this work find that the talent distribution shifts. The middle band of users moves from passive to active. Adoption becomes self sustaining.

In each pattern, the lever is investment in the operating model rather than acquisition of more tools. The lift produced by this investment is non-linear. Modest spend on the binding constraint can unlock substantial benefit from existing tools that were underutilized.

The Governance Component

The governance component is often treated as a compliance afterthought. In ceiling terms, it is sometimes the binding constraint that no one is willing to name. Companies that deploy AI tools without explicit governance produce risk exposure that eventually becomes visible. Companies that deploy AI tools with overly conservative governance suppress adoption to the point that the tools cannot deliver value.

Effective AI governance for mid-market companies has three layers. The first layer is data classification. What information is allowed in prompts. What information is not. Which tools can process which classifications. The classification framework is created once, communicated clearly, and reinforced through training. Without it, employees either share too much sensitive information or share too little useful information.

The second layer is output review. For each category of AI generated output, who is the reviewer of record. What does the review require. When is the review documented. The framework is built into workflows rather than imposed on top of them. Without it, AI outputs propagate into customer or regulatory communications without scrutiny, and the company carries risk it has not measured.

The third layer is logging and audit. Which tools log which interactions. How long are logs retained. What review and audit cadence applies. Mid-market companies often have weak logging infrastructure for AI usage, which creates problems when an issue emerges and the relevant context cannot be reconstructed. Investment in logging is routine and inexpensive but easy to defer.

Operating partners who insist on governance maturity early in the AI deployment journey find that the ceiling lifts higher than they expected. Users feel safer experimenting with tools. Outputs are reviewed appropriately. Risk is managed without suppressing adoption. Governance, properly designed, is a multiplier on adoption rather than a brake.

The Pacing Discipline

The most common error operating partners make in confronting the AI ceiling is to keep buying more tools, faster, hoping the next platform will break through. The ceiling does not yield to additional tooling. It yields to investment in the operating model that supports tooling.

A pacing discipline that respects the ceiling looks roughly as follows. Deploy a small number of tools at a time, in sequence rather than in parallel. Spend at least two quarters between major new deployments, allowing the previous deployment to stabilize and produce measured benefit before the next one absorbs management attention. Use the gap between deployments to invest in data foundation, workflow design, capability building, and governance. Measure adoption rates honestly, and treat low adoption as a signal that the next investment should not be in another tool.

Sponsors who follow this discipline find that their portfolio companies absorb fewer tools than competitors but produce more measured benefit per tool. The AI portfolio looks smaller. The AI impact is larger. The cumulative spend is comparable or lower.

Sponsors who do not follow this discipline build portfolios where most of the AI investment is sitting on the shelf, lightly used, and where the productivity gains promised at the time of approval cannot be substantiated at the time of exit. The investment was made. The ceiling kept it from delivering.

The Underrated Investment

The most underrated investment in private equity AI strategy in 2026 is in the operating model rather than in tools. The operating model is what determines how much of the available capability the business can use. The tools, by themselves, produce diminishing returns once the model is saturated. The model, properly invested in, lifts the ceiling on every tool the business has already bought and every tool it will buy in the next two years.

This is not a glamorous position. Vendors do not market it. Conference keynotes do not feature it. It is, however, the position that produces durable AI driven value creation in portfolio companies, and the position that distinguishes sponsors who realize the AI thesis from those who fund it without capturing it. The ceiling is real. The path through it is operational, not technological. The firms that understand this are the ones whose portfolios will demonstrate, in three years, that AI investment translated into the kind of EBITDA improvement the underwriting case assumed.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.