The Multiple Arbitrage Obituary Was Premature: What SRS Distribution Actually Proved

May 13, 2026

For the past three years, the consensus across private equity has been that multiple arbitrage is finished. The cycle of buying small platforms cheaply, rolling up adjacent businesses, and selling the larger entity at a premium multiple was supposed to have been competed away by sophistication. Every roll-up thesis is now contested. Every multiple expansion assumption faces skepticism in IC. The pitch deck that opens with multiple arbitrage as a primary value driver is treated, in most rooms, as evidence that the team has not adapted to the modern environment.

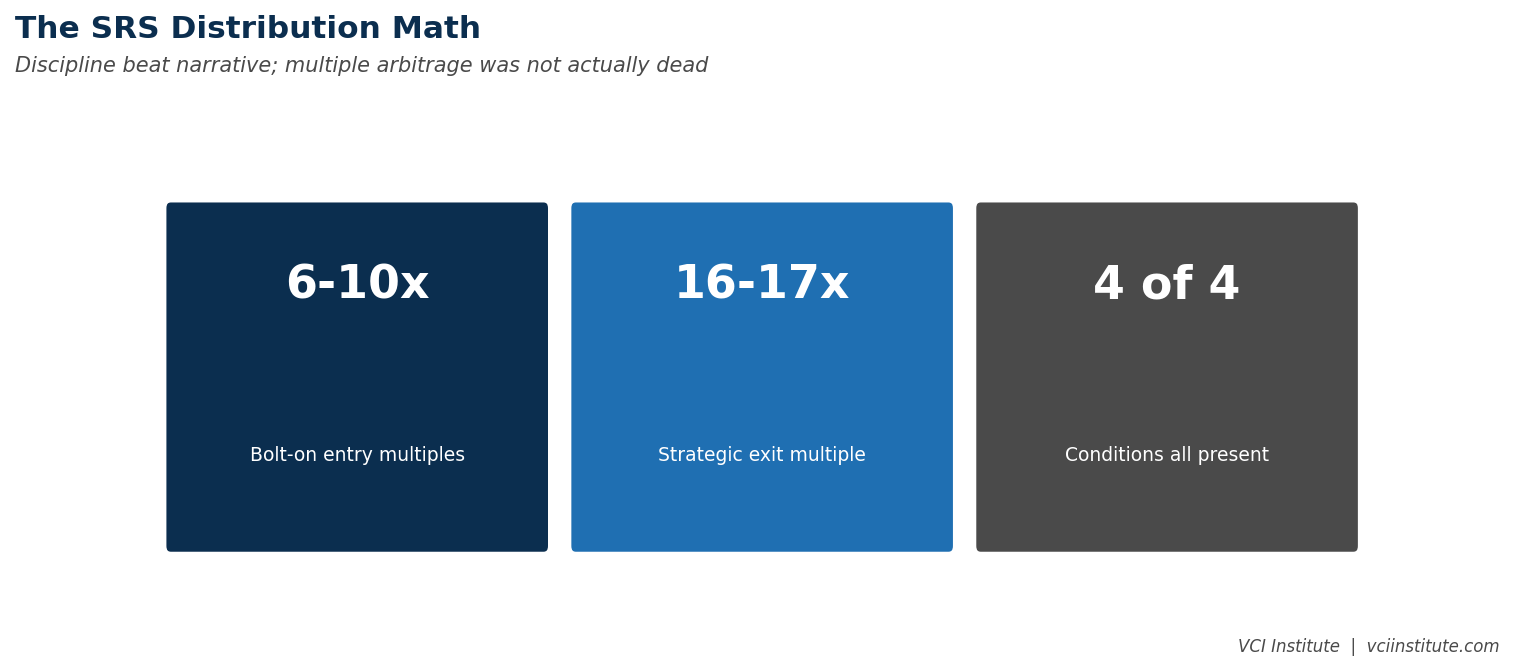

Then SRS Distribution sold to Home Depot at sixteen to seventeen times EBITDA, an asset assembled through acquisitions completed at six to ten times. The transaction did not happen quietly. It was one of the largest deals of its vintage. It produced returns that vindicated the multiple arbitrage thesis at exactly the moment the industry had declared the thesis obsolete.

This is worth taking seriously. Not as a celebration of one transaction, but as a correction to a piece of consensus that has hardened too quickly. Multiple arbitrage is not dead. It is harder. The conditions under which it works have narrowed. The discipline required to capture it has increased. The category of sponsors who can still execute it has gotten smaller. None of this is the same as the obituary.

What the Obituary Got Right

The obituary was not entirely wrong. Several patterns that supported multiple arbitrage in earlier cycles have genuinely weakened.

The pricing gap between platform and bolt-on transactions has compressed in many sectors. The smaller targets that used to trade at meaningful discounts to platform multiples now trade closer to the platform pricing, because financial sponsors compete for them more aggressively, because owners of small businesses have become more sophisticated about the value they hold, and because intermediaries have become more skilled at extracting full value in sale processes.

The integration premium has been increasingly questioned by buyers. The buyer of a roll-up is now looking for evidence that the integration was real, that the synergies were captured, and that the operating discipline produced a coherent business rather than a collection of acquisitions stitched together by financial structure. The integration story that satisfies buyers in 2026 is more demanding than the integration story that satisfied buyers in 2018.

The exit multiples themselves have compressed in some sectors, particularly those that were aggressive multiple compounders during the 2017 to 2021 period. The buyer pool has gotten more selective. Strategic buyers have become more disciplined. The IPO option has narrowed. The financial sponsor secondary buyer pool has become more skeptical of structures that produce value mostly through multiple expansion rather than through operational improvement.

These shifts are real. They make multiple arbitrage harder than it was. They do not make it impossible.

What the Obituary Got Wrong

The obituary missed three patterns that continue to support multiple arbitrage in the segments where it still works.

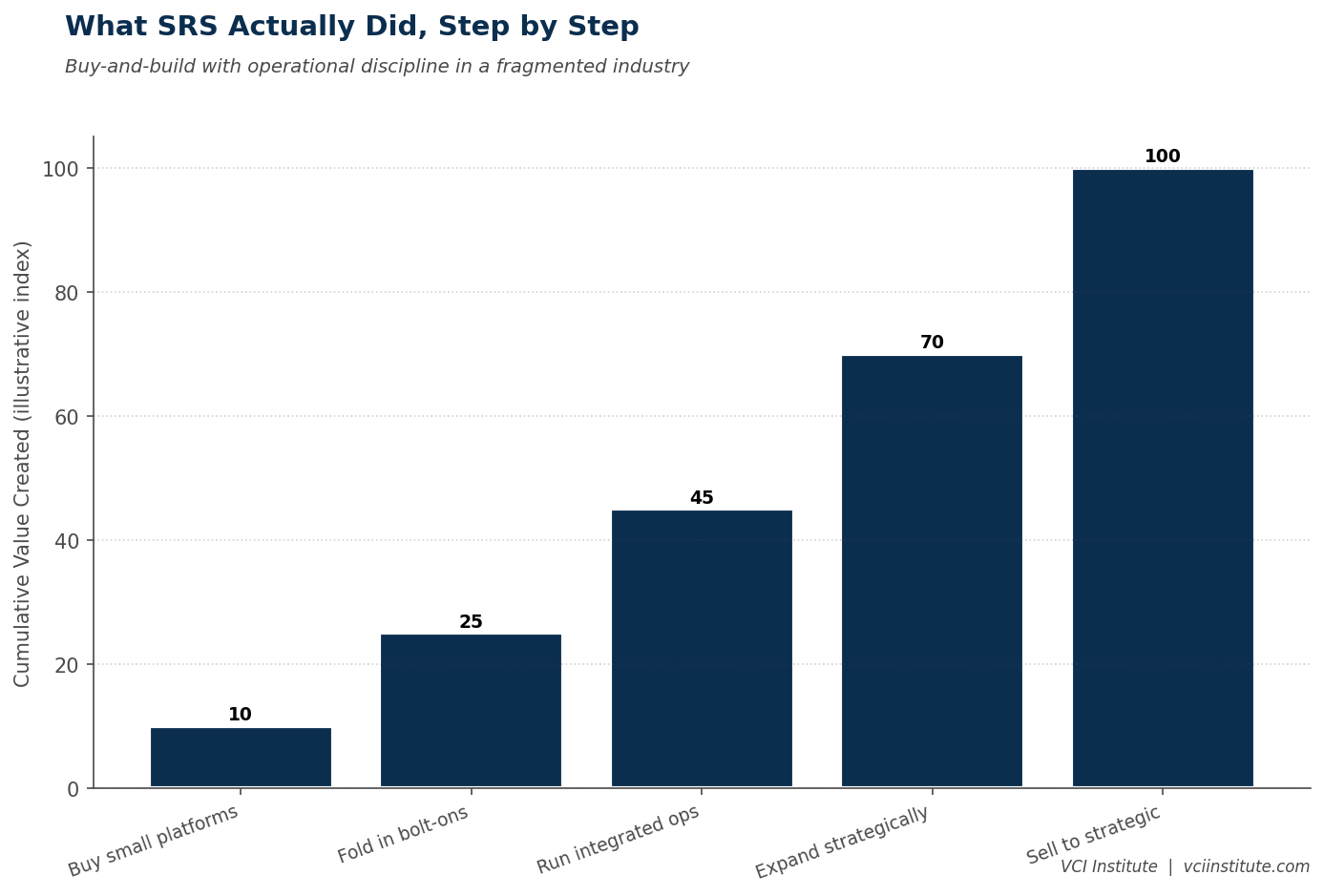

The first pattern is genuine fragmentation. Several large mid-market industries remain genuinely fragmented, with thousands of small operators who individually are too small to be of interest to strategic buyers or to scale-focused financial buyers. The pricing in these markets is structurally lower because the buyer pool for individual targets is small. A platform that aggregates these operators into a larger entity creates an asset that strategic buyers can engage with. The arbitrage is real because the buyer pools are different at the small scale and the platform scale.

The second pattern is operational scale economics. Some industries have genuine economies of scale that emerge above certain size thresholds. Below the threshold, individual operators have higher unit costs, lower negotiating power with suppliers, weaker capability investments, and limited regional reach. Above the threshold, the unit economics improve substantially. A roll-up that crosses the threshold creates an entity with structurally better economics than its component businesses had individually. The buyer who acquires the consolidated entity is paying for the better economics, not just for the multiple expansion.

The third pattern is strategic platform value. Some platforms become attractive to strategic buyers because they offer geographic coverage, customer access, or category presence that the strategic buyer cannot replicate organically. The premium the strategic buyer is willing to pay reflects the strategic value of the platform, not just the financial value of the underlying cash flows. The arbitrage in these cases is real because the strategic buyer values the platform differently than a financial buyer would.

The SRS Distribution transaction illustrates all three patterns. A genuinely fragmented industry. Real operating economics that emerged at scale. Strategic value to a buyer that wanted geographic and category coverage. The arbitrage was not narrative. It was structural.

What Still Works When the Discipline Is There

The conditions under which multiple arbitrage still works are recognizable. Sponsors that operate against these conditions can still produce strong outcomes. Sponsors that pursue arbitrage outside these conditions usually fail.

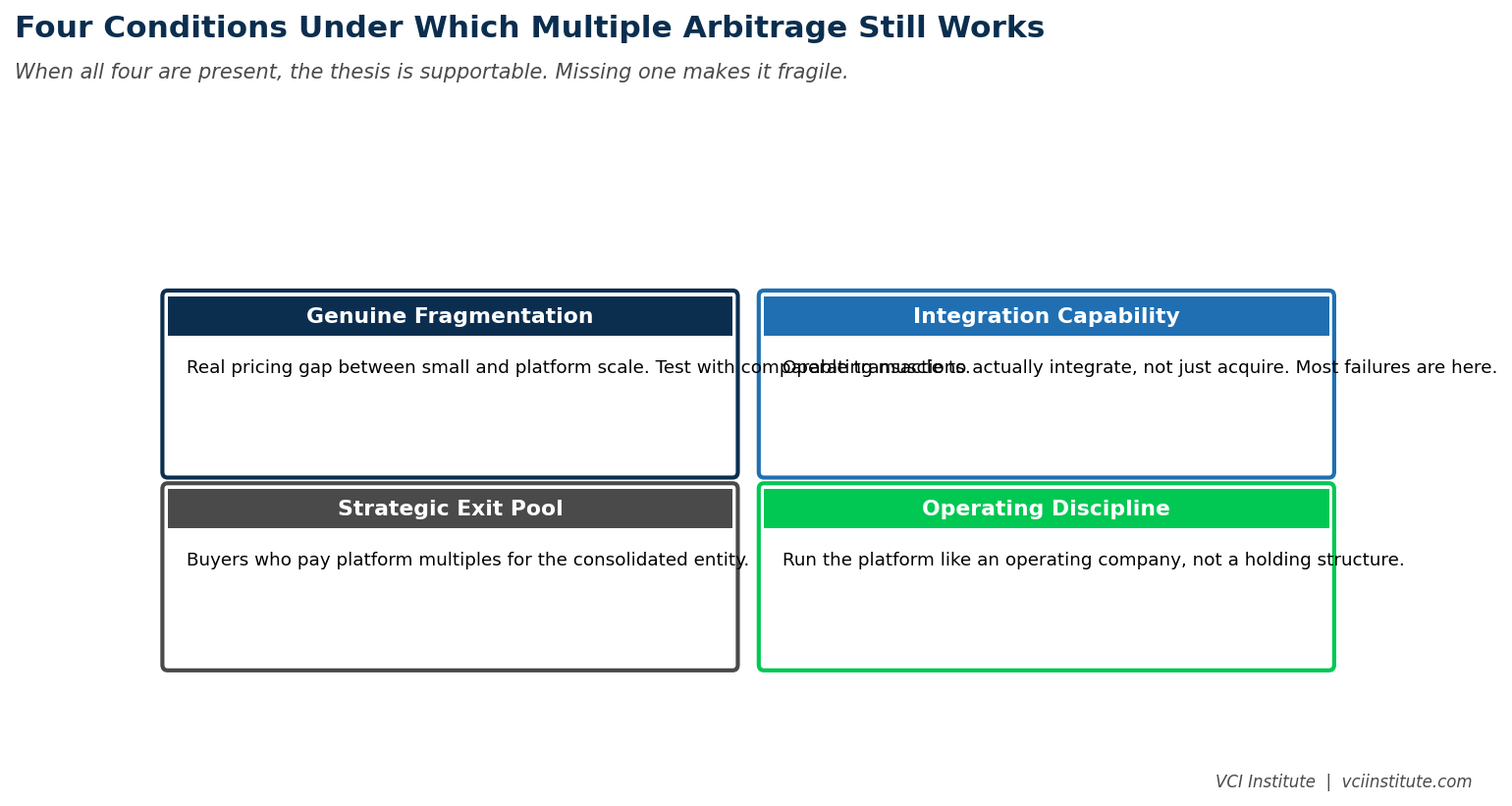

The first condition is genuine industry fragmentation with a meaningful pricing gap between small and platform scale. The pricing gap has to be real, not assumed. Diligence should test it explicitly with comparable transaction analysis at multiple scales. If the gap is below a hundred to two hundred basis points of EBITDA multiple, the arbitrage is fragile. If the gap is several hundred basis points, the structural support is real.

The second condition is operating capability that can actually integrate. Most multiple arbitrage failures are integration failures. The platform buys the bolt-ons but does not integrate them effectively. The operating costs do not converge to the platform's better economics. The systems do not consolidate. The talent does not deploy across the combined entity. Sponsors that pursue arbitrage without genuine integration capability produce a collection of small businesses with platform overhead, not a coherent platform.

The third condition is a credible strategic buyer pool at exit. The arbitrage requires that the platform, once built, has buyers who will pay platform multiples for it. If the strategic buyer pool is thin, the eventual exit may have to be sponsor to sponsor, which compresses the multiple compared to the strategic premium. The exit pool needs to be assessed at the time of platform formation, not at the time of exit.

The fourth condition is operational discipline through the integration cycle. The buy and build that succeeds is the one that runs operating discipline alongside the M and A activity. The acquisitions are integrated into a coherent operating model. The KPIs are aligned. The talent is rotated across the combined entity. The pricing is harmonized. The systems consolidate. Without operational discipline, the platform looks larger but produces less than its component parts did before, because the integration costs have eaten the synergies.

When all four conditions are present, multiple arbitrage still works. SRS Distribution had all four. The thesis was not novel. It was disciplined.

What Stopped Working

It is worth being clear about what stopped working, because the obituary captured something real.

Multiple arbitrage based on financial structure alone, without genuine operational improvement, has stopped working. Buyers no longer pay platform multiples for what is essentially a holding company of acquired businesses. The integration discipline is now the price of admission to the multiple.

Multiple arbitrage in industries that have already been substantially consolidated has stopped working. The fragmentation that supported the arbitrage in the first cycle has disappeared in many industries. Pursuing arbitrage in already-consolidated industries means competing for assets at platform multiples and trying to expand the multiple further, which is a different and harder game.

Multiple arbitrage with operational discipline that exists on paper but not in practice has stopped working. Buyers conduct deeper diligence on integration claims than they did five years ago. The portfolio company that claims integration but cannot demonstrate it loses the multiple premium quickly when the buyer's diligence team probes.

These three failure patterns are what produced the obituary. The pattern is real. The conclusion that multiple arbitrage as a category is dead is the overgeneralization.

The Sponsors Who Can Still Execute

The sponsors who can still execute multiple arbitrage successfully share a recognizable profile. They have deep sector specialization in industries that remain genuinely fragmented. They have built operating capability for integration that they can deploy reliably across acquisitions. They have credible relationships with strategic buyers that give them visibility into the eventual exit dynamics. They have the patience and discipline to execute the platform build over four to seven years rather than rushing to scale.

These sponsors are a smaller group than the population of sponsors that pursued buy-and-build during the peak years. The category has narrowed. Within the narrowed category, the discipline produces results comparable to what the broader category produced earlier in the cycle.

Operating partners working with sponsors that have a buy-and-build thesis should test the thesis honestly against the four conditions. Genuine fragmentation with pricing gap. Real integration capability. Credible exit pool. Operating discipline. If all four are present, the thesis is supportable. If any one is missing, the thesis is fragile and the value creation plan should be calibrated to a more modest assumption about multiple expansion.

What This Means for the Next Cycle

The lesson of the SRS Distribution exit is not that multiple arbitrage is back. It is that the obituary was premature, and that the category was always more nuanced than the consensus made it sound. Some sponsors will continue to extract real value from disciplined buy-and-build in genuinely fragmented industries. Most sponsors will not, because the conditions are demanding and the discipline is hard.

For sponsors evaluating their own buy-and-build positions, the discipline of testing each thesis against the four conditions is the work that matters. Theses that pass produce returns the model assumes. Theses that fail produce returns that disappoint. The market is not the variable. The thesis quality is.

The category is harder than it used to be. It is not extinct. The sponsors that have continued to do it with discipline, against the consensus that declared it over, will continue to capture returns that more skeptical sponsors have walked away from. The obituary was, in the end, less a description of the category than a description of the typical execution within the category. The execution that still works produces results that look like SRS Distribution. The execution that does not produces the disappointments that the obituary was written to explain. Both kinds of execution will continue to occur. The disciplined ones, in the right industries, will continue to be among the best deals in private equity.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.