Transformation Theatre: Why Sponsors Should Stop Funding It (And What to Fund Instead)

May 13, 2026

The most overused word in private equity portfolio company communication in 2026 is transformation. Every portfolio company is undergoing one. Every CEO is leading one. Every board pack opens with progress against the transformation. The word has been emptied of meaning through repetition. It has become the universal alibi for underperformance, the rhetorical placeholder that occupies the space where actual progress should be.

The pattern is recognizable. A portfolio company misses plan for the second consecutive quarter. The CEO presents to the board with a measured tone. The numbers are explained. The challenges are acknowledged. Then the pivot happens. We are still on track with our transformation, the CEO says. The board nods. The conversation moves to the next agenda item. Nobody asks what the transformation actually consists of, what specific outcomes it has produced, or what would constitute evidence that it is working as opposed to evidence that it is being executed. The word has done its job. It has converted underperformance into progress without requiring the underperformance to be addressed.

This is transformation theatre. It is funded by sponsors, executed by management teams, and validated by boards across the industry. It produces visible activity, satisfying narratives, and growing margin pressure on operating partners who are increasingly being asked to deliver value that the theatre is consuming.

What Transformation Theatre Actually Looks Like

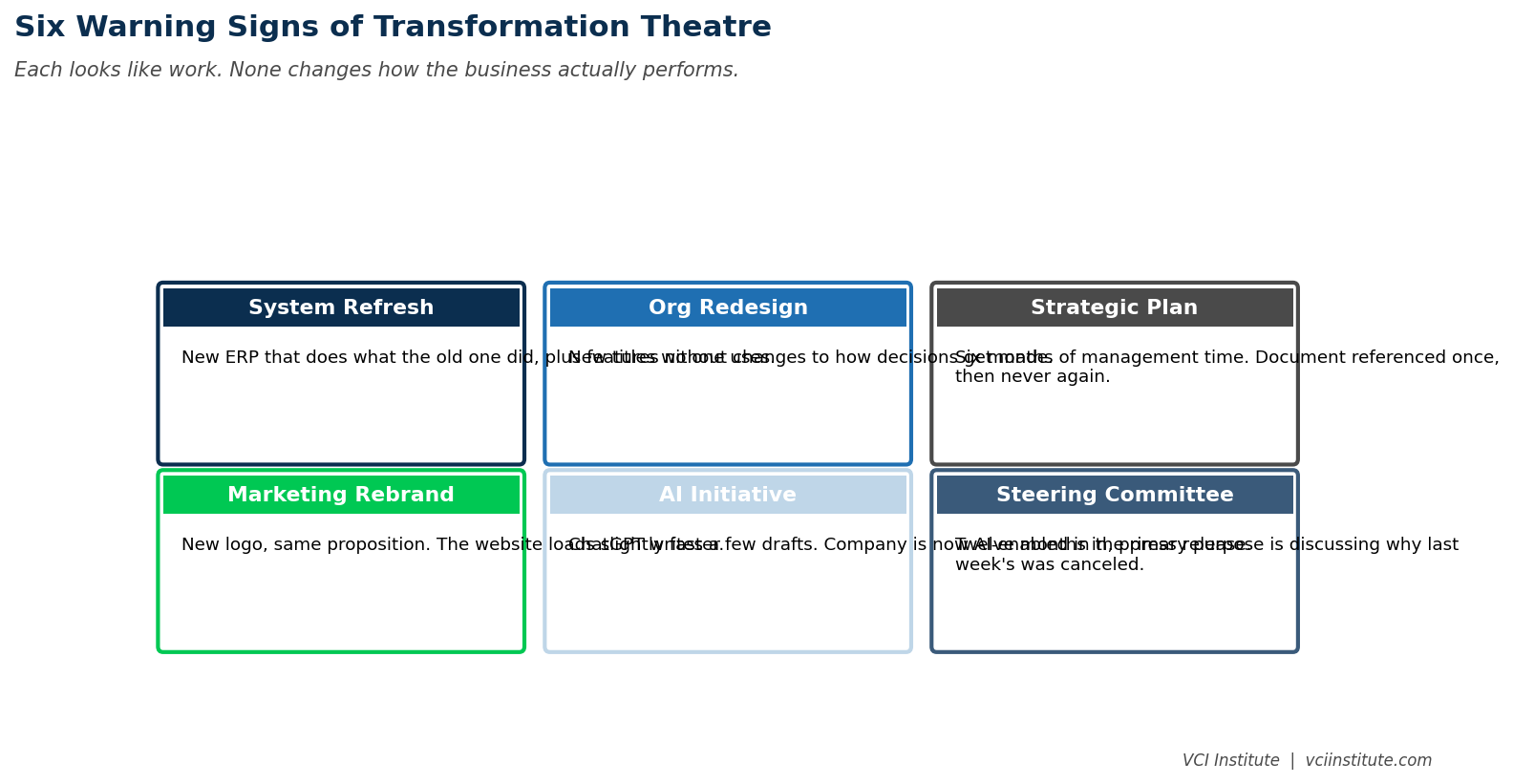

Transformation theatre has recognizable components. Each one has the appearance of substantive work and the actual content of activity that does not move the business forward.

The technology refresh that replaces functioning systems with similar functioning systems, packaged as digital transformation. The new ERP that does what the old ERP did, plus a few features the team will not use, at five times the implementation cost. The new CRM that imports the same dirty data from the old CRM and produces the same misleading reports.

The org redesign that creates new titles without changing how decisions get made. The chief growth officer role that absorbs the responsibilities of the CMO and the CRO without providing the authority to make either of them work better. The center of excellence that has no operating responsibility but produces lengthy strategy documents.

The strategic planning exercise that consumes six months of management bandwidth and produces a document that nobody references again. The annual operating plan that looks substantively similar to last year's plan but with new framing language and a refreshed visual identity.

The marketing rebrand that updates the logo and color palette while leaving the underlying customer proposition unchanged. The new website that loads slightly faster. The new tagline that focuses-grouped well and means nothing.

The AI initiative that asks ChatGPT to draft a few documents and then declares the company AI-enabled. The chatbot deployment that handles the easiest customer inquiries and routes everything difficult to the same understaffed call center.

The transformation office staffed with consultants who produce slides about progress and have no operational authority to actually drive change. The weekly steering committee whose primary purpose, twelve months in, is to discuss why last week's steering committee was canceled.

Each of these components looks like work. Each consumes real time and real money. None of them, individually or collectively, changes how the business actually performs. The word transformation provides the connective tissue that lets the components be presented as a coherent program. Without the word, the components would be exposed as the disconnected, low-impact activities they are. With the word, they cohere into a narrative the board can engage with and approve.

Why Sponsors Keep Funding It

Operating partners watching transformation theatre play out in their portfolios sometimes ask why sponsors keep funding it. The reasons are structural and recognizable.

The first reason is that transformation provides political cover for management teams who would otherwise have to confront harder operational conversations. The CEO who is honest that the business is missing plan because of specific operational issues invites accountability for those issues. The CEO who is missing plan but is leading a transformation has reframed the conversation. The accountability is deferred to the eventual completion of the transformation, which is conveniently always twelve to eighteen months out.

The second reason is that the consultants and vendors whose products require transformation framing have substantial commercial interests in maintaining the language. The transformation office model is staffed by consultants. The technology refresh is sold by vendors. The strategic planning exercise is run by another consultant team. Each of these revenue streams depends on the transformation framing. The collective interest is in keeping the framing alive, regardless of whether specific transformations actually produce results.

The third reason is that sponsors have reputational stakes in transformation narratives. The IC memo at acquisition often described the value creation thesis through transformational language. The mid-hold update is shaped by the same language. The exit story will be presented in similar terms. Acknowledging that the transformation has been theatrical rather than substantive requires walking back the institutional narrative the sponsor has been telling. The walk-back is uncomfortable. The continued funding of theatre is, in some sense, easier than the honest reckoning.

The combination of management cover, consultant interest, and sponsor reputation produces the structural conditions under which theatre flourishes. The theatre is rational for each individual party. The aggregate effect is an industry-wide drift toward funded activity that does not produce results.

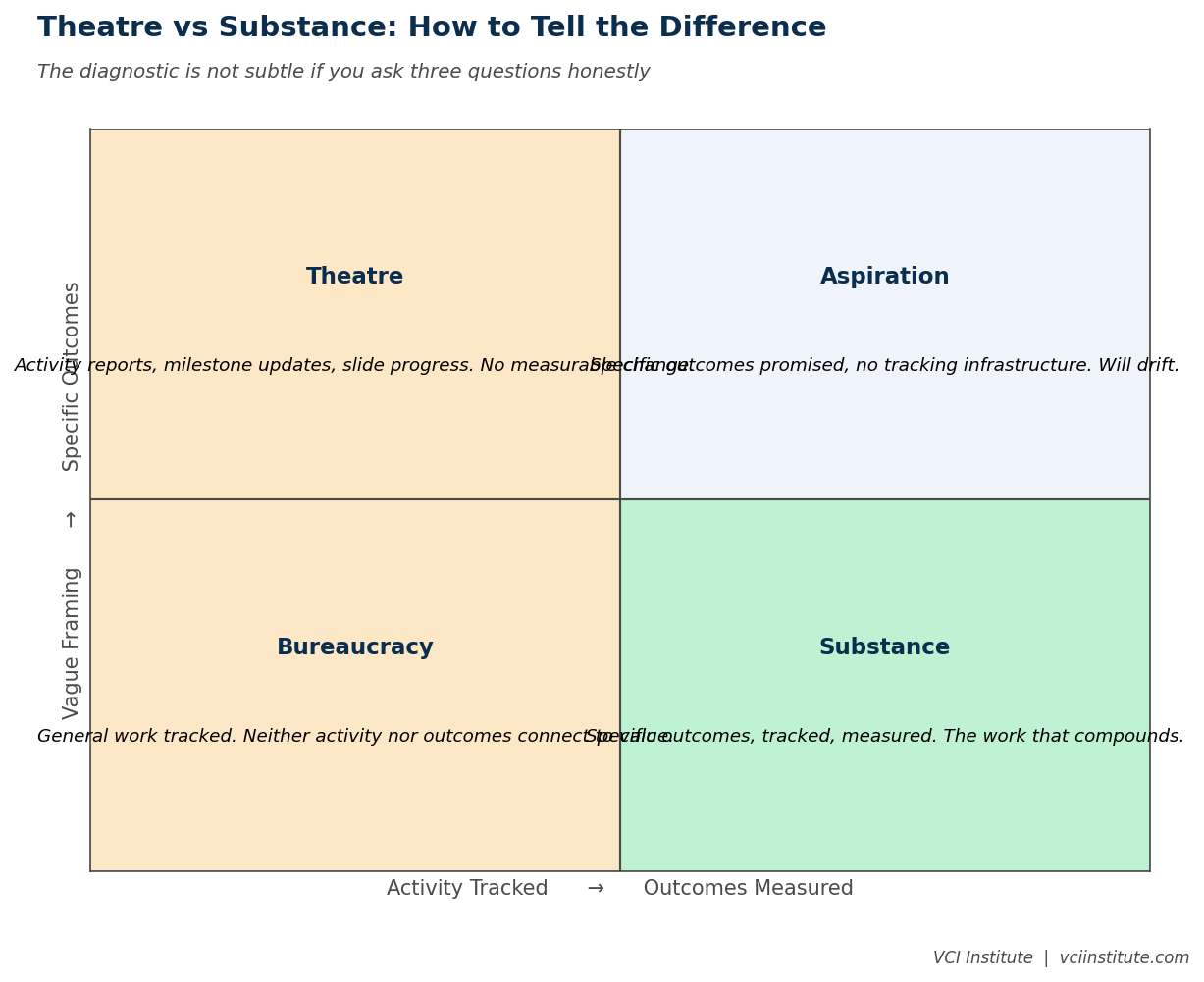

How to Spot the Theatre

The diagnostic is not subtle. Operating partners can ask three questions of any portfolio company transformation initiative and get a reasonably clear read on whether the work is substantive or theatrical.

The first question is, what specifically is supposed to change about how the business operates as a result of this initiative. The answer should be concrete. The sales process will look like this. The customer onboarding will look like this. The pricing structure will look like this. If the answer is general, refers to capability building, or describes activities rather than outcomes, the initiative is more theatrical than substantive.

The second question is, what evidence will distinguish progress from absence of progress. The answer should be measurable. Specific KPIs that move. Specific operational metrics that improve. Specific customer or employee experiences that change. If the evidence consists of milestone completions, slide updates, or reports of activity, the initiative is being scored on activity rather than outcome.

The third question is, what would a reasonable person, looking at this initiative twelve months from now, conclude about whether it had worked. If the framing is set up so that almost any outcome can be presented as success, the initiative is theatrical. If the framing produces a clear test that could fail and be visible as failure, the initiative is substantive.

These three questions, applied honestly, distinguish work that will produce results from work that will produce reports. The honest application is the discipline. Most board meetings do not ask these questions because the answers are uncomfortable. Operating partners who insist on asking them will find themselves alone in some meetings and proven correct over time.

What to Fund Instead

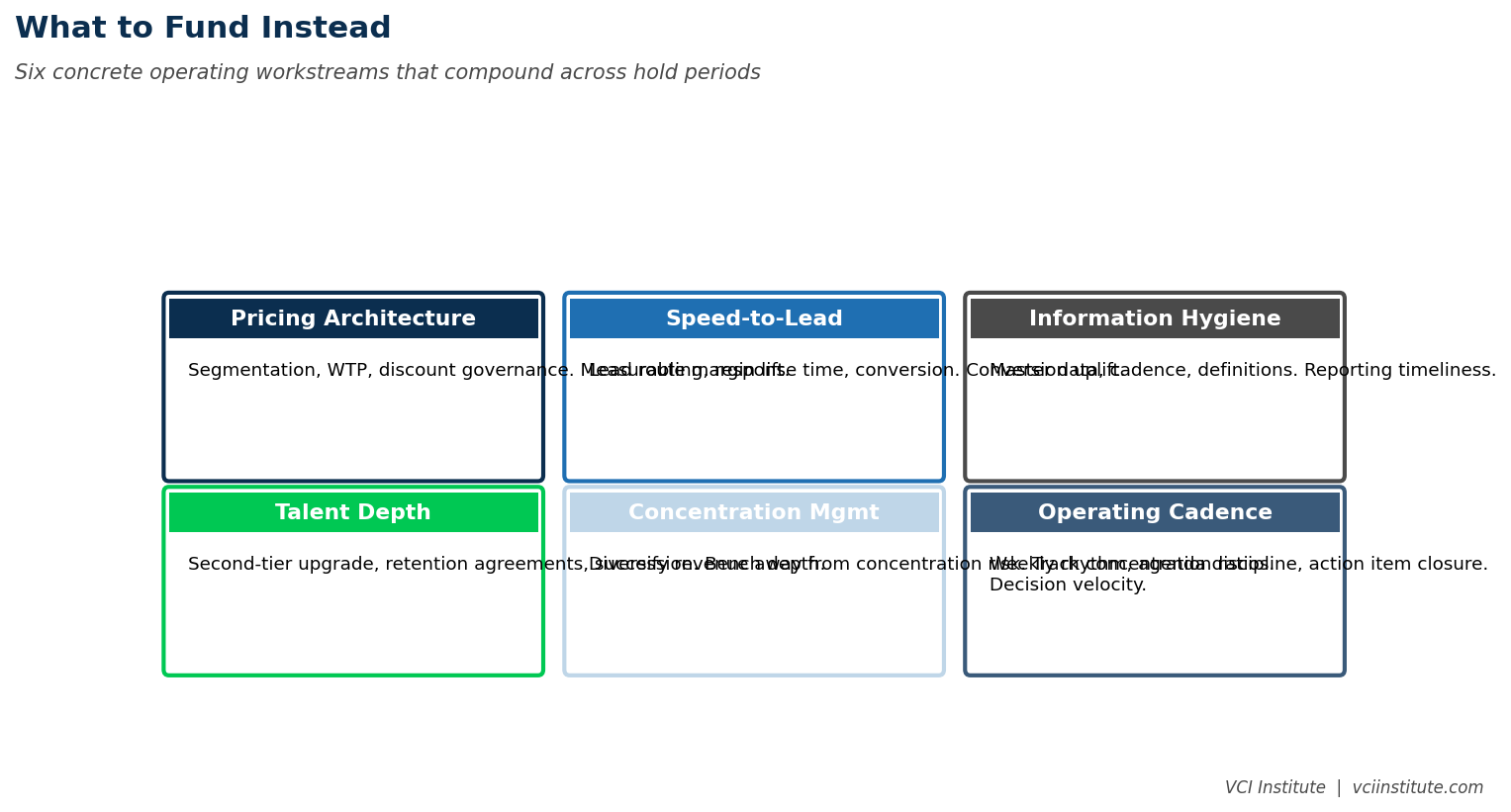

The alternative to theatre is not the absence of change. It is the presence of disciplined operational work that has the unfashionable virtue of being concrete. Several patterns of work consistently produce results across mid-market portfolio companies, and they share the feature of being unglamorous, unbroad, and easily measured.

Pricing architecture. Specific work on segmentation, willingness to pay, and discount governance, with clear metrics for realized prices and margin expansion.

Speed-to-lead infrastructure. Specific work on lead routing, response time, and conversion measurement, with clear metrics for response time and conversion uplift.

Information hygiene. Specific work on master data, reporting cadence, and metric definitions, with clear metrics for reporting timeliness and consistency across functions.

Talent depth. Specific work on the second tier of management, retention agreements for indispensables, and succession planning, with clear metrics for retention rates and bench depth.

Customer concentration management. Specific work on diversifying revenue away from concentration risk, with clear metrics for concentration ratios over time.

Operating cadence. Specific work on the weekly operating rhythm, including agenda discipline, action item closure, and KPI accountability, with clear metrics for cadence consistency and decision velocity.

These six work streams, executed with discipline, produce more value over a typical hold period than the broadest transformation program. They share three features that distinguish them from theatre. They are concrete enough to be specified. They are measurable enough to test. They are unglamorous enough that no consultant or vendor has built a substantial business around marketing them under transformation framing.

The Honest Vocabulary

The fix for transformation theatre is partly a vocabulary change. The word transformation has been so corrupted by overuse that operating partners trying to drive substantive work are sometimes better served by abandoning the word entirely. Specific work produces specific results. The vocabulary should match.

We are improving pricing. We are upgrading our second-tier management. We are building reporting cadence. We are reducing customer concentration. None of these phrases are theatrical. All of them describe work that can be specified, measured, and either completed or not completed. The discipline of using specific language constrains the work itself toward specificity. The discipline of using transformation language permits the work to drift toward generality.

This is not a marketing concern. It is an operating concern. The language a portfolio company uses to describe its value creation work shapes the work that gets done. Companies that describe their work in specific language produce specific results. Companies that describe their work in transformational language produce transformations, which is to say, theatre.

For operating partners working with portfolio companies, the small but real discipline of insisting on specific vocabulary in board materials, in operating reviews, and in strategic conversations produces a cumulative effect. The management team learns that vague framings will be questioned. The consultants learn that transformation packaging will not be sufficient. The board learns to expect concrete answers to the three questions above. Over a hold period, the cultural change in how value creation work is described produces a real change in how it is executed.

The word transformation will not disappear from private equity vocabulary. It is too useful as institutional cover. The question is whether the firms that operate against it, by insisting on specific work and specific results, can build a different kind of track record. The answer, based on the firms that have made the discipline part of their culture, is yes. The track record is real. The exits are cleaner. The narratives at fundraise are more credible. The LPs increasingly notice the difference.

The theatre will continue to be funded by firms that have not yet made the choice. The substance will continue to compound for the firms that have. The choice is available to every operating partner, in every portfolio company, in every board meeting. The cumulative effect of choosing substance over theatre, deal by deal, board meeting by board meeting, is the kind of differentiated capability that wins fundraises and produces the returns that justify the work.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.