Speed-to-Lead Economics: How Response Time Quietly Compounds Into EBITDA

Jun 15, 2026

There is a number that almost no portfolio company tracks consistently and that turns out to predict an unreasonable share of commercial performance. It is the elapsed time between an inbound lead arriving and the first meaningful contact attempt by the company.

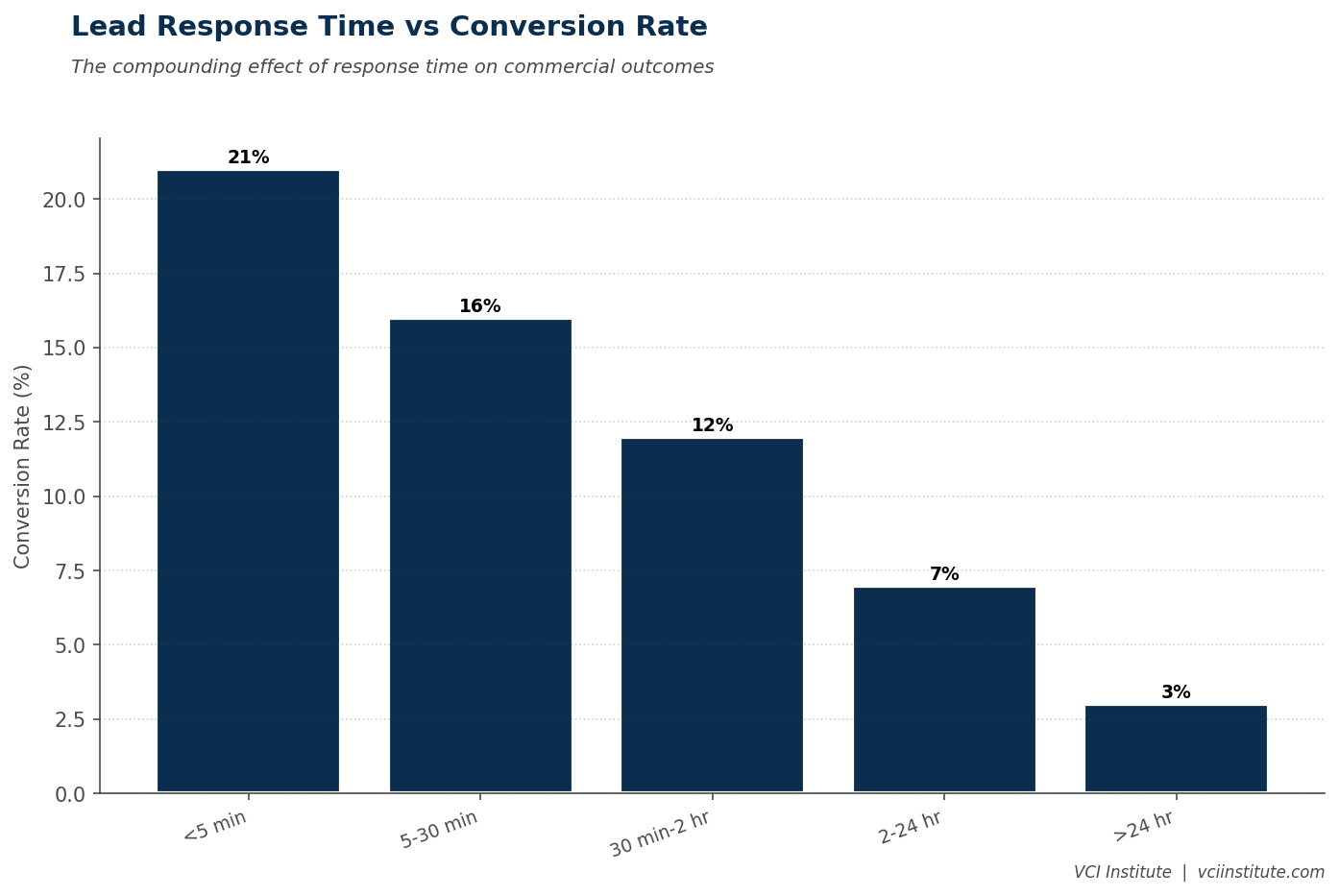

The data on this is not new. Studies going back more than a decade show that contact attempts within five minutes of lead arrival convert at meaningfully higher rates than attempts within an hour. Attempts within an hour outperform attempts within twenty four hours. After forty eight hours, the lead is essentially a marketing list. Response curves vary by industry and channel, but the shape is consistent. Speed compounds. Delay decays.

What is striking is how rarely this metric makes it into the operating cadence of mid-market portfolio companies. Most companies track lead volume. Many track conversion rates. Some track customer acquisition cost. Few track time to first contact. Even fewer track it segmented by lead source, lead quality, and rep, which is where the actionable intelligence sits.

This is a gap, and a productive one for any sponsor who understands its economics.

The Math Hidden in Minutes

The mathematics of speed to lead are almost embarrassing in how mechanical they are. A business with one thousand qualified leads per month, a current contact rate of seventy percent within forty eight hours, and a conversion rate of fifteen percent on contacted leads, generates one hundred and five new customers per month. If average contract value is fifty thousand and gross margin is fifty percent, the monthly contribution from new logos is roughly two and a half million.

Now imagine the same business shifts its contact rate to ninety percent within five minutes, with no change in lead volume or quality. Conversion lifts to twenty two percent based on industry data. The monthly customer count jumps to one hundred ninety eight. The contribution doubles to roughly five million. Annualized, that is a thirty million dollar swing in gross margin from operating discipline alone, with no change in marketing spend, no new headcount, and no new product.

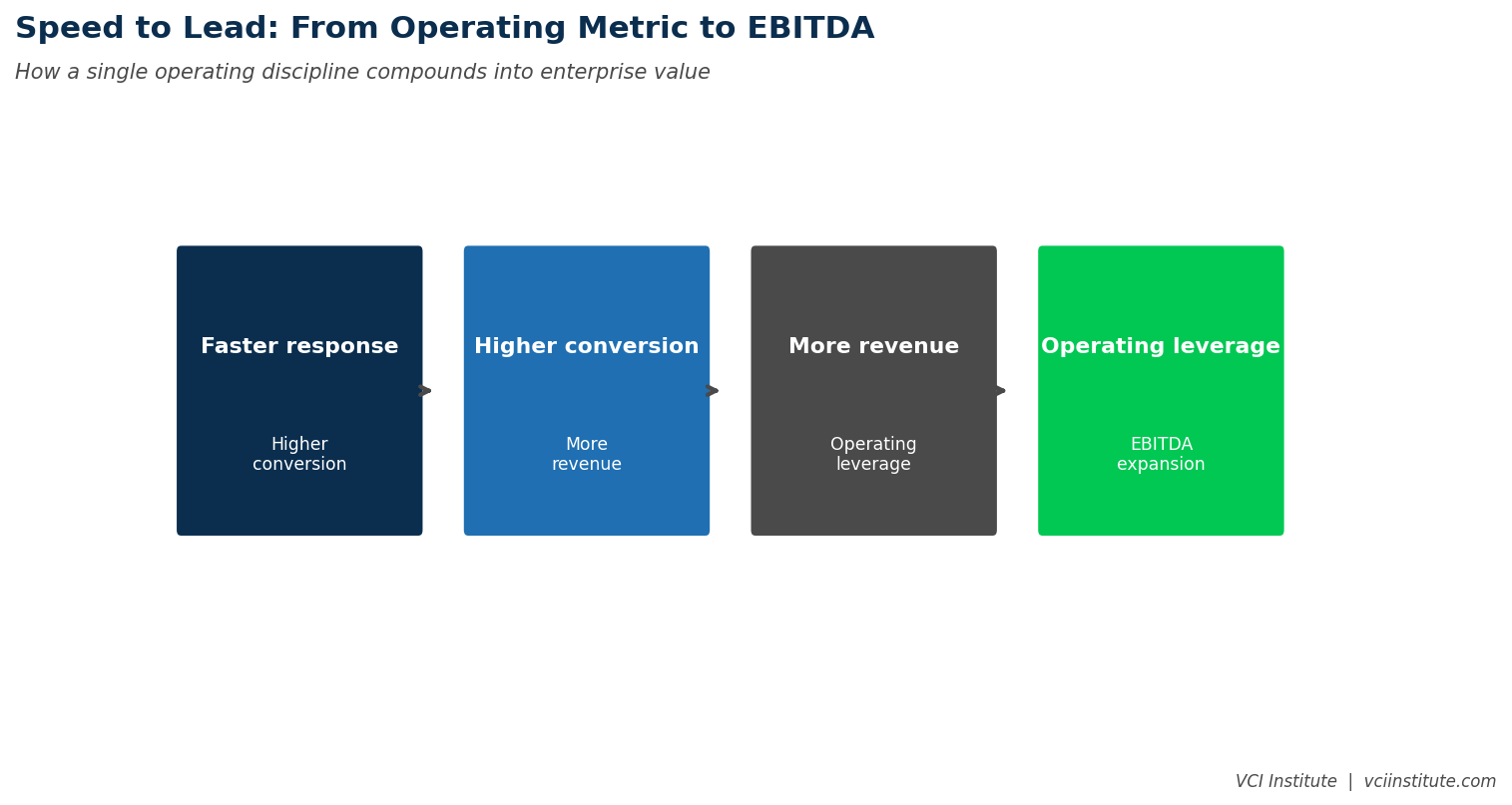

The numbers above are illustrative, but the pattern is consistent across every commercial business we have analyzed. Improving speed to lead by an order of magnitude usually produces somewhere between thirty and seventy percent more closed business from the same lead pool. The lift is essentially free, in the sense that it does not require capital investment. It requires operating discipline.

In a private equity context, that lift converts directly to EBITDA. Most commercial businesses have ninety percent gross margin or higher on incremental revenue from existing customers. Even on new logos, gross margin is usually high enough that the speed to lead lift translates one to one into operating profit. A two times multiple expansion at exit on this kind of margin improvement is meaningful capital.

Why Companies Do Not Already Do This

If the lift is so accessible, why do most companies not already capture it. The answer is a familiar pattern of organizational dysfunction.

The first reason is that nobody owns the metric. Marketing claims responsibility ends at lead delivery. Sales claims responsibility starts at qualified opportunity. The handoff between marketing and sales is a process gap where the lead sits, unattended, sometimes for hours. Each function has its own KPIs and its own cadence. Speed to lead, which lives in the gap, is owned by neither.

The second reason is that the process is informal. Leads arrive in a CRM, an inbox, a marketing automation system, or a phone line. They are routed by rules that have not been audited in years. They are picked up by reps based on availability rather than priority. There is no SLA. There is no escalation. The lead either gets called or it does not, depending on what else is happening that morning.

The third reason is that the system architecture often makes speed structurally difficult. The CRM is not integrated with the marketing automation tool. The lead arrives in one system and the rep gets notified in another. The phone system is not connected to the CRM. The reporting that would surface a speed problem is not built. Each gap adds friction. The cumulative friction is enough that even a motivated sales team cannot consistently respond fast.

The fourth reason is that nobody is measuring it. What is not measured is not managed. Most CRMs can produce a speed to lead report with a few configuration changes. Almost no mid-market company has done those configurations. The metric does not appear on any dashboard the executive team sees. The board never asks about it. Months go by without anyone noticing that the company's lead response is in the seventy second percentile of decay rather than the second percentile of opportunity.

The Three Levers of Speed Improvement

Closing this gap is one of the cleanest commercial transformations in the operating partner toolkit. Three levers do almost all the work.

The first lever is routing. The current routing logic in most companies is a relic. Round robin distribution among reps. Geographic assignment that no longer matches the customer base. Manual triage by a sales operations analyst who is not always available. The fix is to build automated routing that sends the right lead to the right rep instantly, based on rules that reflect actual lead quality and rep specialization. This is mostly a CRM configuration project. It pays back in weeks.

The second lever is notification. The current notification model in most companies is email. Email is a slow channel. Reps check it on their schedule, not on the lead's schedule. The fix is to move lead notifications to push channels that interrupt rather than wait. SMS to the rep's phone. Slack alerts to the team channel. CRM mobile app push notifications. The technology already exists. The configuration takes a few days. The behavior change takes a few weeks.

The third lever is response. The current response model in most companies depends entirely on rep availability. If the rep is in a meeting, on another call, or out of office, the lead waits. The fix is to add automated first touch responses that engage the lead immediately while the human follow up is still being arranged. Modern conversational AI tools can credibly hold a first conversation, qualify the lead further, and book a calendar slot for the rep. This is the highest leverage AI use case in commercial operations right now, and the one where the math is easiest to defend.

What Sponsors Should Track

Operating partners who want to capture this lever can build it into the standard portfolio operating cadence with three measurements.

The first measurement is the median time from lead arrival to first contact attempt, segmented by lead source. This number tells you whether the company has a routing problem, a notification problem, or a response problem. Different segments fail for different reasons.

The second measurement is the contact rate by time bucket. What percentage of leads receive a meaningful contact attempt within five minutes, fifteen minutes, one hour, four hours, and twenty four hours. The shape of this distribution reveals where the cliff is. Most companies have a sharp cliff somewhere between fifteen minutes and four hours. The cliff is the gap between when the company thinks it is responsive and when it actually is.

The third measurement is conversion rate by contact time bucket. This is the metric that proves the economic case to the management team. When the data is plotted, the conversion difference between the five minute bucket and the four hour bucket is usually large enough to make the investment case obvious. Once the team sees the number, the political resistance to changing the process tends to evaporate.

The Compounding Effect

What makes speed to lead a particularly attractive lever in a private equity context is that it compounds. The improvement does not require ongoing capital. Once the routing, notification, and response systems are built, the lift continues for the life of the hold. As lead volume grows, the absolute dollar value of the lift grows with it. As marketing investment scales, the speed to lead efficiency multiplies the return on that investment. By exit, a portfolio company that built speed discipline early has a sustainably better commercial engine than its underwriting case assumed.

There is also an exit multiple effect. Buyers value commercial engines that demonstrably work over commercial engines that historically worked. A business that can show a tight, instrumented sales process with documented speed metrics, conversion data, and rep level performance is more credible at exit than a business that simply has a strong year of bookings. The discipline shows up in diligence. It shows up in the multiple.

The Question to Ask in Your Next Board Meeting

The next time you sit in a portfolio company board meeting and the CEO presents the commercial dashboard, ask one question. What is the median time between lead arrival and first contact attempt across our highest value lead segment in the past thirty days. If the CEO has the number, ask for the trend over the past six months. If the CEO does not have the number, you have just identified a value creation initiative that is almost certainly worth more than whatever else is on the agenda.

Speed to lead is unglamorous. It does not feature in keynote addresses. It is not a transformation initiative anyone will brag about at a conference. It is, however, one of the cleanest, fastest, most defensible EBITDA levers available to any operating partner with the discipline to measure it, the patience to fix the underlying processes, and the political capital to make the management team care about minutes rather than months. Done well, it produces a measurable lift in a single quarter and a structural advantage by exit. Done badly, or more commonly not done at all, it leaves seven figures of EBITDA sitting in the gap between when a customer expressed interest and when the company finally got around to calling them back.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.