The Pre-Close Operating Veto: Underwriting Value Plans You Can Actually Execute

Jun 08, 2026

Most private equity value creation plans are not designed to be executed. They are designed to win an investment committee.

That is not a moral failing. It is a structural feature of how deals get built. The deal team writes the IC memo. The deal team owns the model. The deal team carries the political weight inside the firm to push the deal through. The operating team, where it exists, gets handed the plan after closing and is asked to deliver it. The handoff is the moment most value creation plans begin their slow death.

Operating partners who arrive after close inherit a document built by people who will not be measured against its execution. The synergy assumptions are aggressive because aggressive synergy assumptions help the model clear the hurdle rate. The integration timeline is short because short integration timelines support the IRR. The talent assumptions are optimistic because optimistic talent assumptions reduce the apparent risk of the thesis. None of these things are dishonest. They are simply the predictable result of a process where the people writing the plan and the people executing the plan are different people, with different incentives, on different sides of a closing date.

The fix is to give the operating team a real veto before close. Not a polite sign-off. Not a cameo on slide forty-seven of the IC deck. An actual veto on the value creation plan, supported by independent diligence, staffed with their own resources, with the authority to either stop the deal or rewrite the plan into something they will own.

We call this the pre-close operating veto. Firms that have it find their plans hold up under execution. Firms that do not have it find their plans collapse around month four.

Why Plans Collapse

The collapse pattern is consistent. The first ninety days of ownership go reasonably well because the plan's early actions are usually achievable. The hundred day plan gets executed. The cost reductions get identified. The new CFO gets recruited. Everyone is on schedule.

Around month four, reality starts to push back. The cross sell synergy that depended on integrating two CRM systems turns out to require eighteen months of data migration the diligence missed. The sales productivity uplift that depended on hiring six new account executives runs into a tighter labor market than the plan modeled. The SKU rationalization that was supposed to lift gross margin discovers that two of the candidate SKUs are actually anchor products for a key channel partner. The pricing initiative that was supposed to produce three hundred basis points of margin runs into customer churn the plan did not contemplate.

Each individual setback is recoverable. The cumulative effect is that the plan starts to look optimistic, then unrealistic, then quietly aspirational. By month nine, management is producing parallel internal forecasts that diverge from the plan and apologizing for the divergence. By month twelve, the operating partner is rewriting the plan and explaining to the deal partner why the original numbers were never quite right.

This is the moment when operating partners discover they are the cleanup crew for a document they did not write.

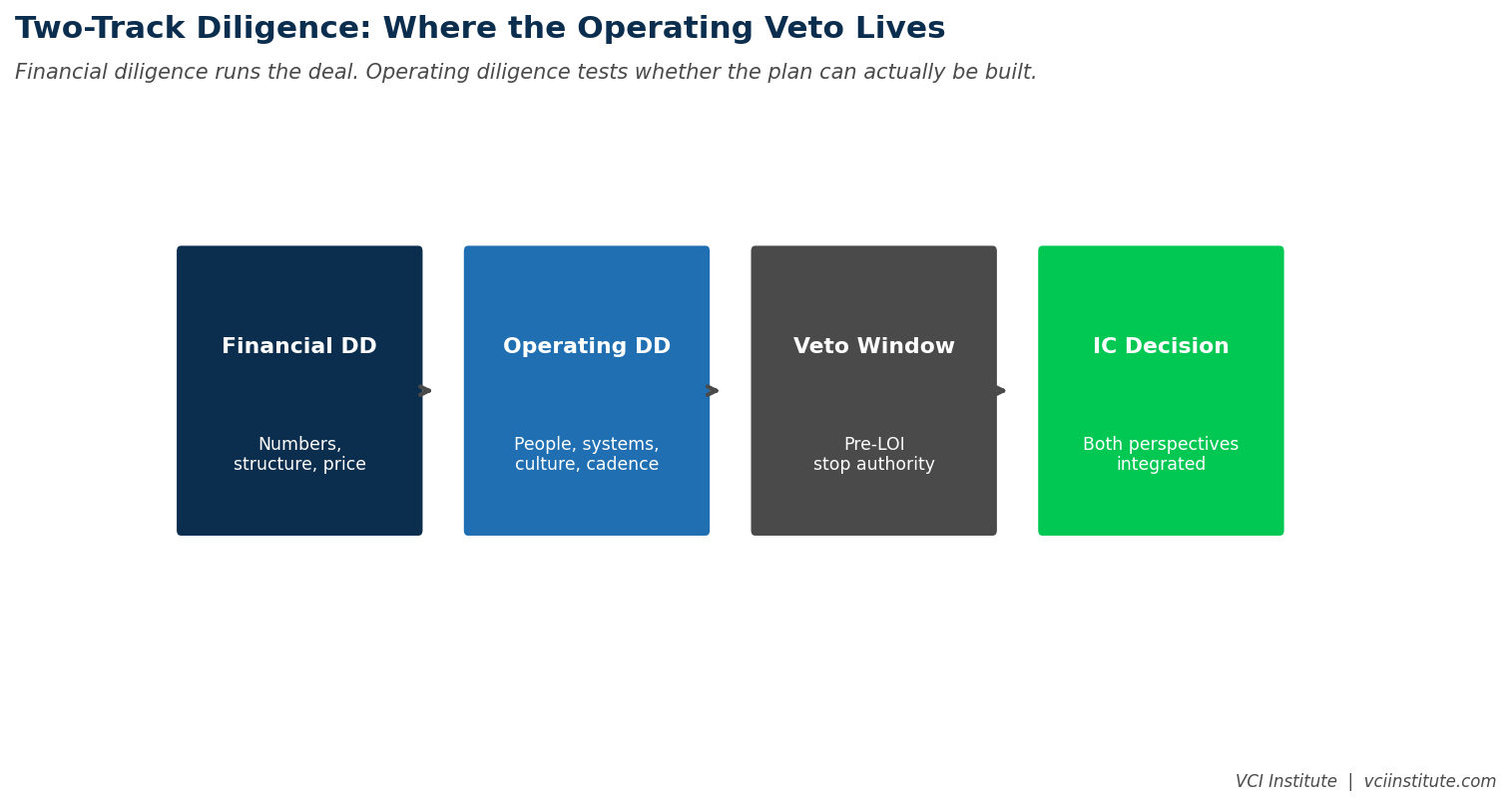

The Two-Track Diligence Model

The structural fix is to run two parallel diligence tracks before close. The first track is the deal team's diligence, focused on validating the thesis, the model, and the price. The second track is the operating team's diligence, focused on whether the value creation plan is actually executable in the form the model assumes.

These are not the same exercise. The deal team's diligence asks whether the business is worth the asking price under a reasonable plan. The operating team's diligence asks whether the specific plan being underwritten can be delivered by a real management team in a real market within the modeled timeline. The first is an investment question. The second is an execution question. Both have to clear before a deal closes.

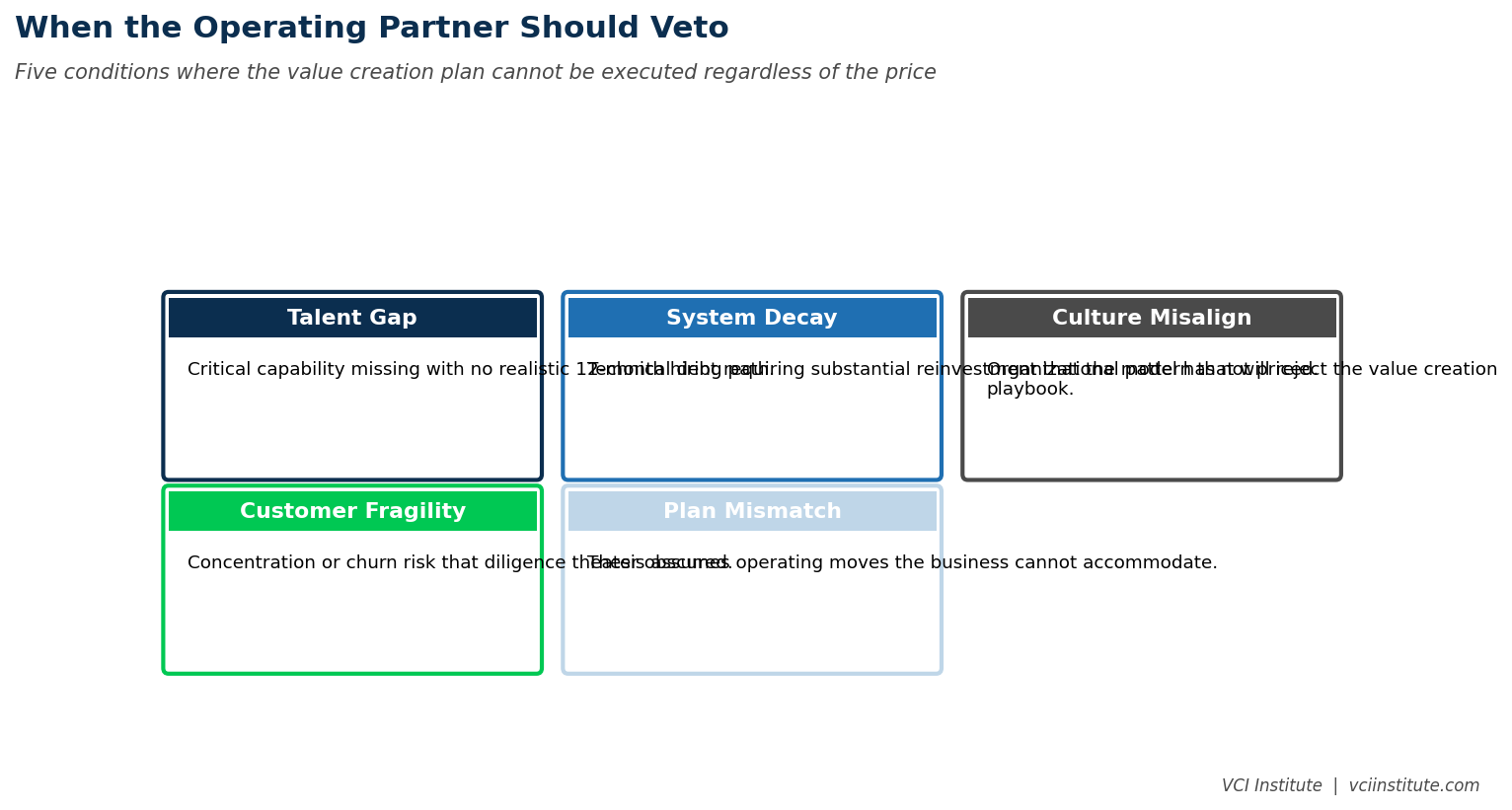

Operating diligence covers terrain that financial diligence routinely misses. Talent depth in the second and third management layer, where the actual work happens. Integration complexity hidden in legacy systems and undocumented processes. Customer concentration risk that hides inside revenue recognition policies. Pricing power assumptions that depend on customer behavior nobody on the deal team has tested. Capital expenditure required to support the growth plan, which models often understate. Cultural compatibility between acquired entities in a buy and build, which models cannot quantify but operating teams can sense.

When operating diligence is done seriously, it produces three outputs. A revised value creation plan, calibrated to what is actually deliverable. A risk register, listing the assumptions that could break the plan and how they will be monitored. A resource plan, listing the people, capital, and systems required to deliver, with honest costs and timelines. These three documents become the baseline against which the operating team is measured for the rest of the hold.

What the Veto Looks Like

The veto operates at three points in the deal process. Each point has a specific decision being made.

The first point is during initial diligence, before significant deal team capital has been committed. The operating team reviews the early thesis and flags any assumption that strikes them as undeliverable based on their experience. This is a low-cost intervention. If the assumption is genuinely undeliverable, the deal can be repriced or abandoned before the firm has invested heavily in pursuit. If the assumption survives challenge, the diligence proceeds with shared understanding of what is being underwritten.

The second point is at the IC stage, when the formal value creation plan is presented. The operating team has authority to either approve the plan as the executable basis for the deal or to require revisions before IC will hear it. This is the most politically charged point in the process. Deal partners do not enjoy being told their plan needs to be rewritten. Firms that handle this badly produce conflict between deal and operating teams. Firms that handle it well produce mutually owned plans that both functions stand behind.

The third point is at signing, when the operating team confirms it has the resources, the people, and the time to deliver the plan as constructed. If any of those three are missing, the deal closes with an explicit recognition of what is uncertain, and capital is committed to filling the gap before day one. This avoids the all too common pattern where a deal closes with an implicit assumption that the operating team will figure something out, and the operating team spends the first six months figuring out what the deal team committed to.

The Cultural Cost

There is a real cultural cost to giving operating teams a pre-close veto. Deal teams used to operating with autonomy do not enjoy a structure where the operating function can stop or reshape their deals. The conflict is most acute in firms that talk about being operationally focused but where the operating team is, in practice, decorative. Adding genuine veto power to a decorative operating team produces immediate friction, because the operating team starts behaving as if it has authority that everyone had quietly assumed it would not exercise.

Firms that get this right invest in the relationship between the deal and operating sides at the partner level. The most senior operating partner is paired with the most senior deal partner. They build a working relationship before any specific deal forces them to disagree under pressure. They develop a shared vocabulary about what executable means, what realistic means, what aggressive but achievable means. By the time a specific deal arrives, the cultural infrastructure is in place to have a productive disagreement without it becoming a power struggle.

Firms that get this wrong create a structure where the operating team is technically allowed to veto but, in practice, cannot do so without political consequences. The veto becomes ceremonial. The plans go through unchallenged. The operating team becomes the cleanup crew. And the firm continues to wonder why so many of its deals underperform their underwritten plans.

The Investor Signal

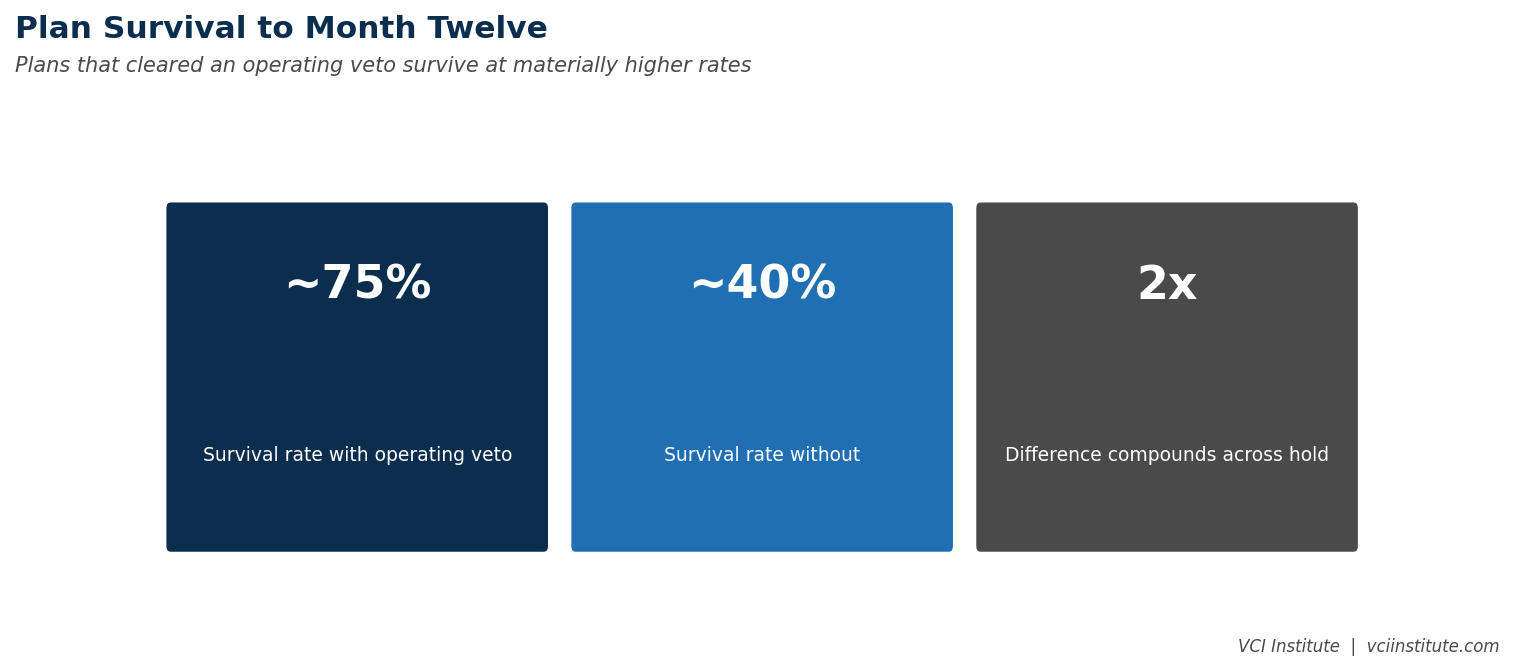

There is a quieter benefit that becomes visible only over a multi-fund track record. Firms with genuine pre-close operating vetoes produce more consistent returns. Their deals do not all hit, but the variance around the mean is tighter. Their plans do not always exceed expectations, but they more rarely collapse below the underwritten case. Over a fund life, this consistency compounds into a track record LPs notice.

LPs are increasingly sophisticated about how to read GP performance. They know that any GP can produce a few standout deals. The question is what happens to the other twenty or twenty-five investments in the fund. Firms whose operating teams have real authority before close tend to have fewer disasters. Firms where the operating function is decorative tend to have a longer tail of underperformers and more frequent need to extend hold periods to recover plans that were never realistic.

This shows up at fundraising time. The GP that can credibly explain how its operating team shapes deals before close has a different conversation with prospective LPs than the GP that talks about operations as a post-close discipline. The veto, properly implemented, becomes part of the firm's institutional advantage.

The Discipline Behind the Discipline

The pre-close operating veto is not really about authority. It is about institutionalizing the question that is too rarely asked at the moment it can still be answered cheaply. Can we actually do this. Not under heroic assumptions. Not in a frictionless market. Not with talent we do not yet have. Can we actually do this, with the team we will inherit, in the time the model assumes, against the resistance the business and the market will produce.

That question costs almost nothing to ask before close. It costs everything to ask after close, because by then the price is paid and the plan is what it is. Firms that give themselves the structural permission to ask it, and to act on the answer, end up with value creation plans that survive contact with reality. Firms that do not, end up with plans that look impressive in IC and disappointing in year two.

The veto is the cheapest insurance product in private equity. It is also the one that most firms still refuse to buy.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.