The Strategic Reframe Lever: How a Better Description of the Business Changes Its Enterprise Value

Jun 04, 2026

A landscaping company in the southeast came up at an investment committee three years ago. Standard mid-market deal. Twelve trucks, a hundred and twenty customers, mostly residential, some light commercial, the founder still showing up on Saturdays to fix a quote. The numbers were fine. The growth rate was unremarkable. The multiple being asked was a touch ambitious for what looked like a service business.

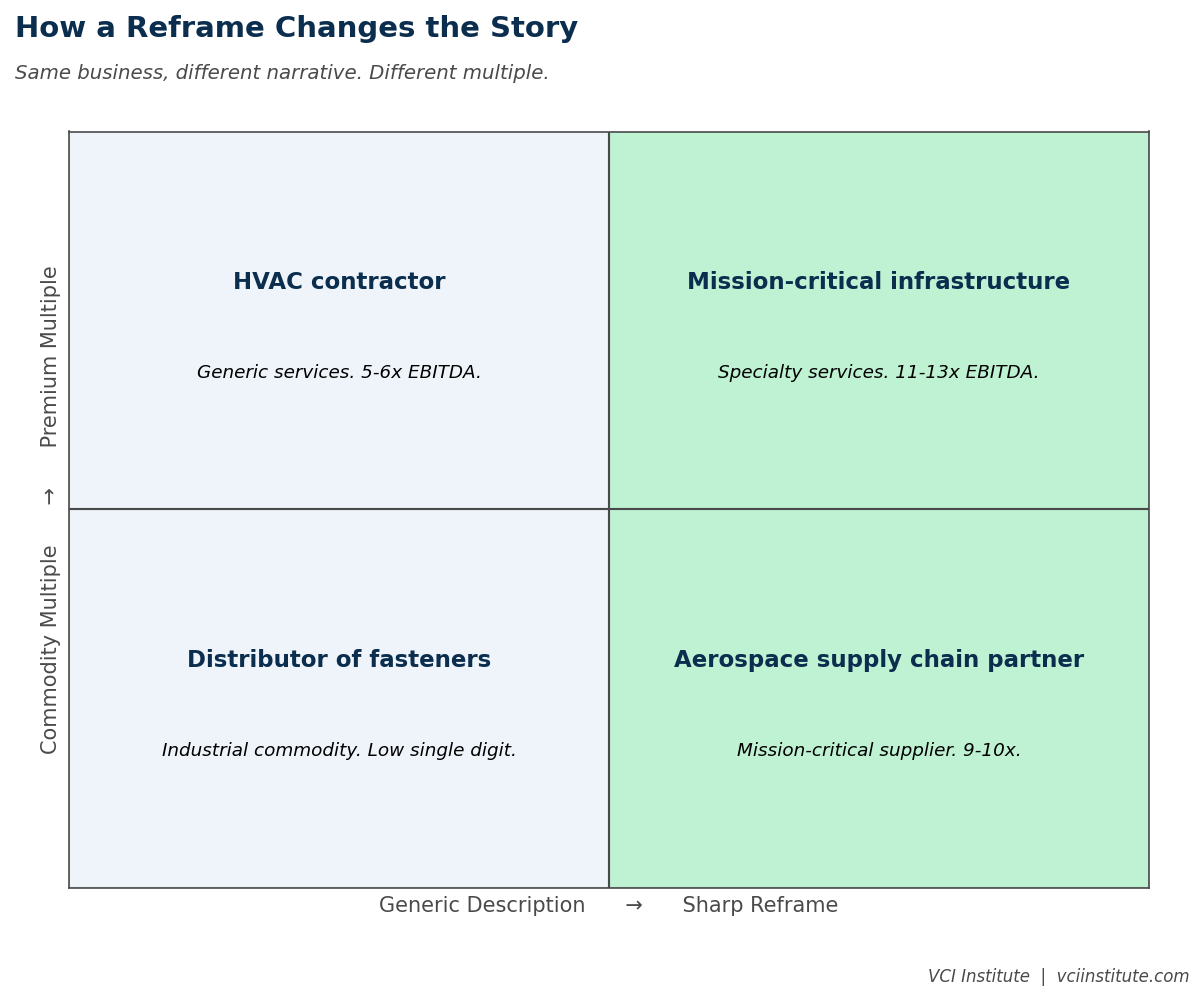

Most of the room called it a landscaping company. One operating partner did not. He called it a recurring revenue, route density optimization business with embedded local market clustering and customer convenience pricing power. Same trucks. Same crews. Same customers. Different lens.

The deal got done. Three years later it sold for a multiple that nobody who described it as a landscaping company would have underwritten.

This is the strategic reframe lever, and it is the most underused tool in private equity value creation. It costs nothing. It requires no capex, no new hires, no software. It changes everything that happens inside the business after it is applied. And it is dismissed as semantics by the same people who later wonder why the company sold for less than it should have.

Language Drives Strategy

The way a company describes itself shapes every important decision that follows. A company that thinks it is in landscaping competes on price for the next quote, treats scheduling as administration, sees routes as an operational detail, and tolerates churn because customers always come and go in service businesses. The same company described as a recurring revenue and route density platform thinks in customer cohorts, lifetime value, retention engineering, and local market clustering. It hires differently. It markets differently. It prices differently. It builds differently.

The companies look identical from the outside on day one. Two years in, the second one is generating thirty percent more EBITDA on the same revenue base. The reframe was not cosmetic. It was operating.

We see this pattern across the mid-market. A pool service business is not a pool service business. It is a recurring revenue, weather-resilient, route density compounder. A regional accounting firm is not an accounting firm. It is a recurring annuity, switching cost protected, advisory upsell platform. A specialty distribution business is not a distribution business. It is a working capital efficient, supplier consolidation engine with embedded customer stickiness.

Every one of those reframes changes how the company is run, what it measures, where it invests, and ultimately how the buyer values it on the way out.

The Reframe Taxonomy

There are five categories of reframe that operating partners use most often. Each one points at a different latent source of value the management team has not yet seen in their own business.

The first is the recurring revenue reframe. A business that thinks of itself as transactional gets repositioned around the predictable cash flow streams hidden inside its customer base. Annual maintenance contracts. Repeat purchase patterns. Subscription-like behavior that nobody had labeled. Once the team starts measuring annual contract value, net revenue retention, and gross retention, the entire commercial motion changes.

The second is the platform reframe. A business that sees itself as a single product company gets repositioned as a customer franchise with cross sell and adjacency potential. The fishing equipment company that becomes a lifestyle brand. The accounting firm that becomes an advisory practice. The HVAC operator that becomes a building services platform. The reframe converts a one-product business into a multi-product business in the management team's own mind, before it does so in the P&L.

The third is the density reframe. A geographically dispersed operation gets repositioned as a clustering business where unit economics improve dramatically with local concentration. This applies to any field service business, any logistics operation, any branch-based model. The route density logic that transforms a landscaping company applies equally to home health, residential cleaning, pest control, mobile vehicle service, and a long list of others.

The fourth is the data reframe. A traditional business that quietly collects unique transactional or behavioral data gets repositioned around that data asset. The specialty distributor that knows what end customers buy. The diagnostics company that aggregates clinical patterns. The fleet operator that holds usage telemetry. The data was always there. Naming it as an asset changes how the company invests around it.

The fifth is the trust reframe. A business in a category where buyers are skeptical, frustrated, or burned gets repositioned as the credible operator in a low-trust market. The contractor who actually shows up. The clinic that actually returns calls. The provider that actually does what was quoted. In categories defined by widespread mediocrity, simple operational reliability becomes a strategic moat that supports premium pricing.

Why the Reframe Lever Is Underused

If reframing is so powerful, why is it not standard practice. Three reasons.

The first reason is that it sounds like marketing language to people who came up through finance. Operating partners with deep modeling backgrounds are trained to be skeptical of narrative. A reframe that does not change the spreadsheet feels suspicious, even when it is the precondition for changing the spreadsheet.

The second reason is that founders often resist it. The CEO who built a landscaping business spent twenty years calling it a landscaping business. The reframe can feel like a denial of the work, a smart-aleck consultant insisting the thing is something else. Operating partners who push reframes badly turn the conversation into a status fight. Operating partners who push reframes well anchor the new language in something the founder already knows is true and just had not labeled.

The third reason is that the payoff is delayed. The reframe does not move EBITDA in the first quarter. It moves the things that move EBITDA over a hold period: hiring decisions, marketing spend, M&A appetite, system investment, KPI selection, the metrics that get reported up to the board. The compounding shows up in year two and year three. By exit, the reframe has rewritten the equity story.

How Operating Partners Run a Reframe Well

A good reframe starts with diagnostic questions, not with answers. What do customers actually buy from you, beyond the surface transaction. Who buys repeatedly, and what does the repeat behavior look like. Where is the cluster of demand densest. What information does the business hold that competitors do not. Which customer segments would pay more if they trusted the offer. The answers reveal the latent business model the founder has been operating without naming.

A good reframe is then anchored in language the management team can use without feeling absurd. It is not a corporate identity exercise. The founder still sells landscaping when she meets a homeowner. Internally, however, the team is now tracking route density, retention by neighborhood, contract value per route mile, and cross-sell penetration. The strategic instruments shift, even when the customer-facing language does not.

A good reframe finally rewires what the business measures. The reporting that used to track jobs completed and quotes won now tracks active recurring contracts, retention by tenure, customer acquisition cost by channel, and route economics by zone. The KPIs are the carrier of the reframe into the operating discipline. Without new KPIs, the reframe stays at the level of slogan. With new KPIs, it becomes the new operating model.

The Exit Mathematics

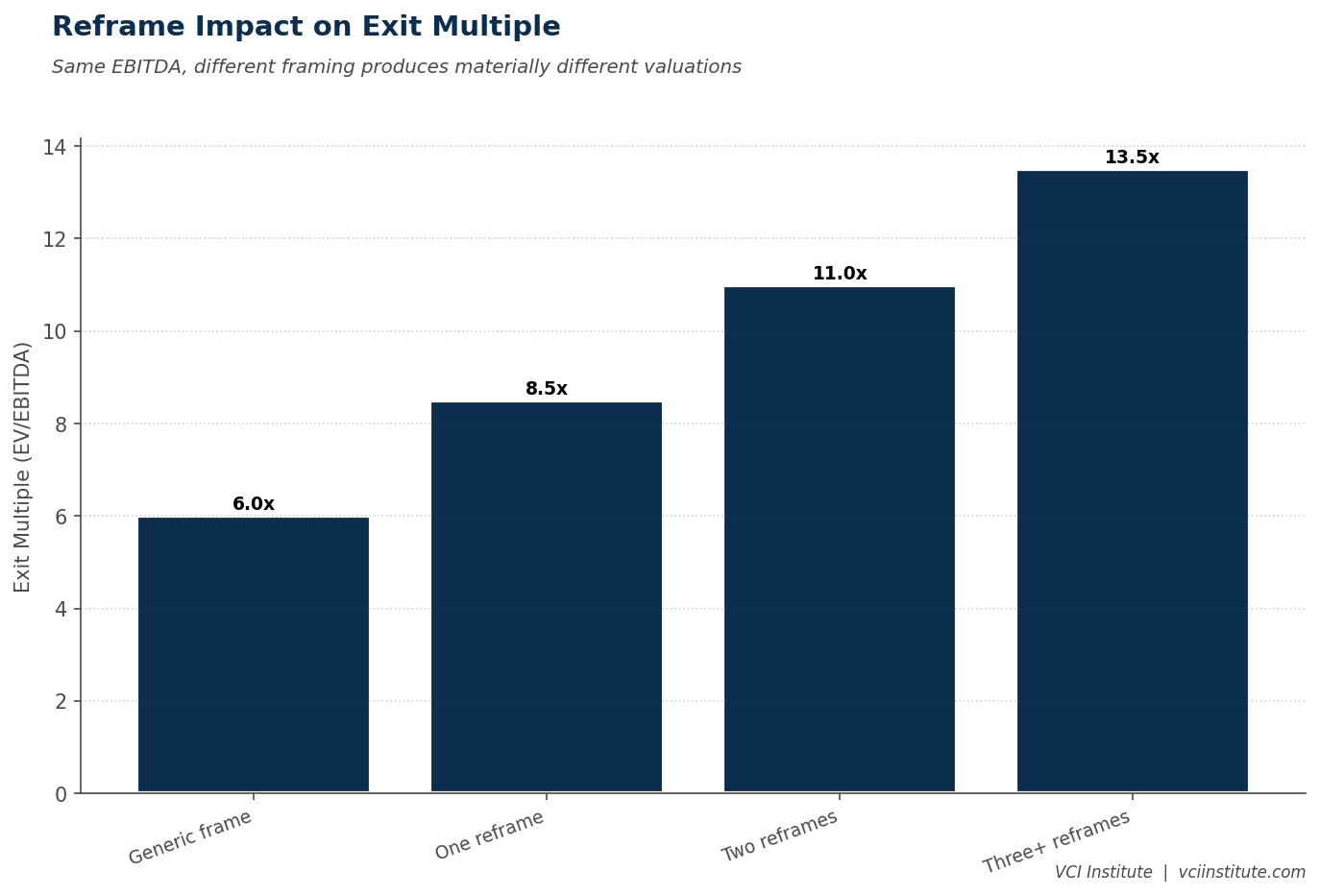

Reframes pay back twice. First during the hold, by changing the operating discipline of the business. Second at exit, by changing the comparable set the business is sold against.

A landscaping company sold as a service business gets compared against other service businesses, with multiples in the high single digits. The same business sold as a recurring revenue compounder with route density advantages gets compared against subscription businesses, route based platforms, and consolidation plays, with multiples in the low to mid teens. The mathematics of exit are partly a function of operating reality. They are also partly a function of which comparable set the business sits inside in the buyer's mental model.

Operating partners who understand this engineer the reframe early in the hold and document the operating discipline that supports it. By the time the company is in the market, the buyer is not trying to be convinced of a story. The buyer is encountering a business that has been built and reported on according to that story for two or three years. The reframe is no longer a positioning argument. It is a P&L argument with a vocabulary attached.

The Cheapest Lever in the Toolkit

Capex programs cost money. M&A programs cost money. Talent upgrades cost money and time. The reframe lever costs neither. What it requires is operating partners who understand that language is not a peripheral concern. Language is the operating system the management team uses to make every decision.

Most companies are trapped inside lazy descriptions of themselves. They have never been forced to articulate what they actually do, who actually buys from them, why those buyers stay, and which assets the business has accumulated without recognizing them. A good operating partner provides that articulation, in language the team can use, anchored in something the founder already knew, supported by metrics that turn the new lens into operating discipline.

Done well, this is the cheapest, fastest, highest-leverage move in the value creation toolkit. Done badly, it sounds like consultants playing word games. The difference is whether the reframe is grounded in something the business actually contains and whether the operating model gets rewired to make it real. Get those two things right and the lever moves enterprise value with no incremental dollars spent. Get them wrong and you have wasted a board meeting describing the same business with fancier nouns.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.