Vertical AI Versus Horizontal AI: A Sponsor's Allocation Decision

Jul 02, 2026

Private equity has spent eighteen months funding AI initiatives across portfolio companies, and a real allocation question is now coming into focus. Not whether to invest in AI. The question is no longer interesting. The actual question is whether to bet on horizontal AI platforms, the broad copilots and general purpose tools that aim to improve productivity across every function, or on vertical AI applications, the domain specific tools that solve a narrow problem in a specific industry deeply.

The choice matters because the two categories have fundamentally different economics, different deployment timelines, different defensibility, and different exit multiples. Sponsors who treat them as interchangeable tend to overspend on horizontal tools that produce diffuse, hard to measure benefits, while underinvesting in vertical applications that compound over the hold period. Sponsors who treat them as a real allocation decision build portfolios that are economically sharper.

The Two Categories Defined

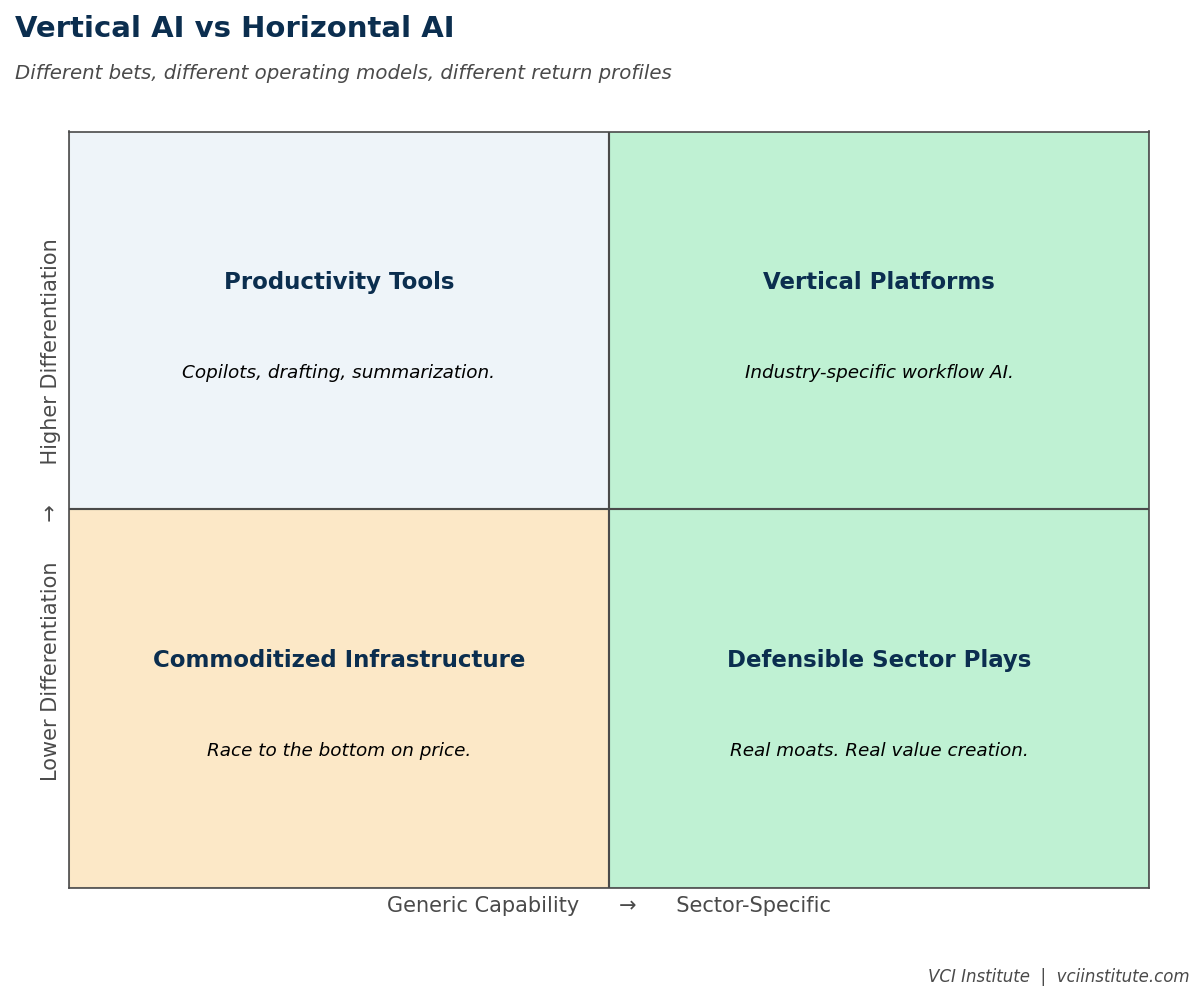

Horizontal AI applies to general purpose work. Drafting emails. Summarizing documents. Generating slide content. Coding assistance. Customer service triage. Meeting transcription and synthesis. The use case is broadly applicable across functions, industries, and roles. The vendors are large platform companies, mostly hyperscalers and major enterprise software providers. The deployment is relatively quick. The benefit, in any single use case, is real but modest, usually fifteen to thirty percent productivity improvement on a defined set of tasks.

Vertical AI applies to specific industry workflows or domain problems. Underwriting risk for specialty insurance. Predicting failure modes in industrial equipment. Optimizing route density for field service operations. Detecting anomalies in healthcare claims. Automating underwriting in commercial lending. The use case is narrow but deep. The vendors are usually domain specialists, often smaller companies with deep industry expertise embedded in their models. The deployment is usually slower, often six to twelve months. The benefit, when realized, is large, often forty to seventy percent improvement on a specific workflow that may represent a meaningful share of the company's cost base or revenue capture.

The two categories also produce different defensibility profiles. Horizontal AI rarely creates lasting competitive advantage at the company level, because every competitor has access to the same tools. The advantage erodes as adoption spreads. Vertical AI creates more durable advantage, because the deployment requires domain integration that competitors cannot replicate quickly, and the data accumulated through use becomes a moat over time.

How Sponsors Tend to Misallocate

The pattern across portfolios in 2026 is consistent. Sponsors are over-funding horizontal AI and under-funding vertical AI.

The over-funding pattern shows up as multiple portfolio companies independently subscribing to enterprise copilot suites, often without measuring the impact. The cost is meaningful, often several hundred thousand dollars per portfolio company at scale, totalling millions across the fund. The benefit is real but diffuse. Productivity improves in pockets. Hard to measure. Hard to attribute. Hard to defend in IC.

The under-funding pattern shows up as vertical AI initiatives that are conceived but not properly resourced. The portfolio company identifies a vertical use case that could materially change its economics. The investment required is significant, often several million dollars over twelve to eighteen months. The internal team does not have the skills to deploy it. The vendor relationship requires careful management. The sponsor allocates partial funding, hopes the team will figure it out, and discovers two years later that the project never quite got off the ground.

The cumulative effect is that sponsors end up with portfolios that have spent meaningfully on AI without producing the kind of step changes in operating economics that would justify the spend in the EBITDA bridge.

When Horizontal AI Earns Its Place

This is not an argument against horizontal AI. There are specific use cases where horizontal tools clear an EBITDA bridge cleanly. Three are worth highlighting.

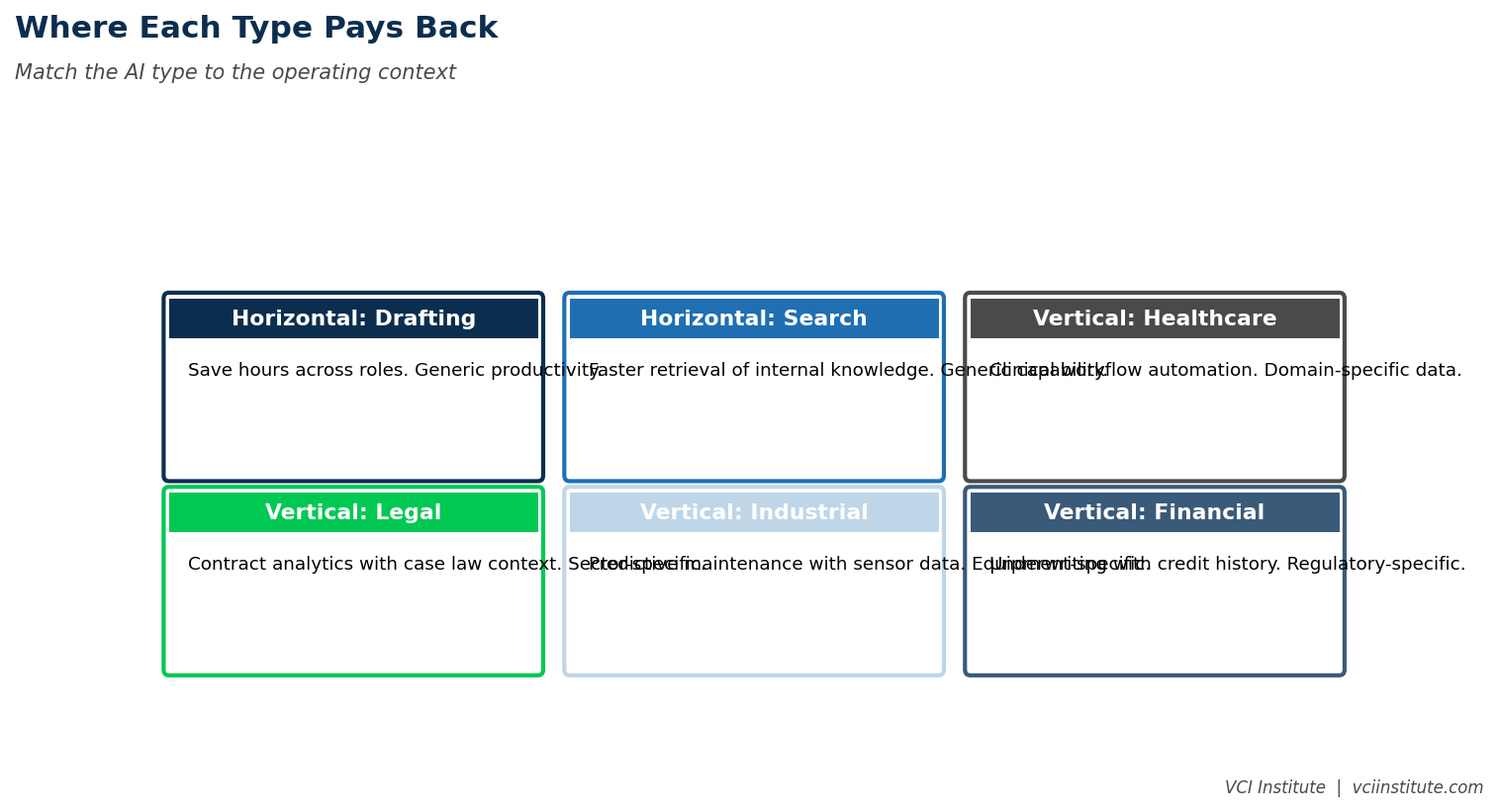

The first is professional services productivity. In professional services businesses, the cost base is concentrated in billable labor. A fifteen to twenty percent productivity improvement on senior associate work, sustained across the firm, translates directly into capacity and margin. The use case is straightforward. The investment is bounded. The bridge is clean. Many private equity owned professional services firms have legitimate horizontal AI cases.

The second is customer service efficiency. Horizontal AI tools that handle first level customer service inquiries, with human escalation for complex issues, can reduce service costs by twenty to forty percent in businesses with high inquiry volumes. The bridge is direct. The deployment is relatively rapid. The math works in customer service heavy businesses such as e-commerce, telecommunications, and certain segments of insurance.

The third is sales operations support. Tools that help sales teams research prospects, draft outreach, and synthesize call notes can produce measurable productivity improvements in commercial functions, particularly in mid-market businesses where sales operations infrastructure is weak. The improvement is incremental rather than transformational, but the cost is also low, and the bridge usually clears at modest effort.

These three use cases share a feature. The cost base they affect is meaningful, the productivity improvement is measurable, and the deployment is fast enough to show up in the operating cadence within a single quarter. Horizontal AI investments in these domains are defensible. Investments outside these domains usually require more imaginative business cases that hold up less well under scrutiny.

When Vertical AI Earns Its Place

Vertical AI investments earn their place when the use case is core to how the business makes money or how it spends money. Three patterns recur.

The first pattern is core underwriting or pricing. In businesses where pricing is a core capability, specialty insurance, commercial lending, freight brokerage, certain segments of healthcare, vertical AI applied to pricing can produce competitive advantage that compounds. The model gets better as it processes more transactions. The data moat grows. The pricing accuracy improves. The competitive position strengthens. Investments here often pay back several times over because they affect a top three line item in the P&L.

The second pattern is core operational optimization. In businesses where a specific operational decision drives a significant share of variable cost, route optimization in logistics, predictive maintenance in industrial equipment, scheduling optimization in services, vertical AI can produce double digit cost improvements that hold over time. The deployment is slow because the integration with operations is complex. The benefit, once stabilized, is durable.

The third pattern is core customer intelligence. In businesses where customer behavior prediction matters, retention sensitive subscription models, complex B2B relationships, healthcare population management, vertical AI can identify churn risk, upsell opportunities, and intervention points with precision that horizontal tools cannot match. The advantage is in the domain specificity of the model and the customer specific data the company has accumulated. The investment compounds over the hold period.

The common thread is that vertical AI investments, when chosen well, affect lines of the income statement that materially move enterprise value at exit. Horizontal AI investments, even when successful, tend to affect a broader but shallower set of cost categories.

The Allocation Heuristic

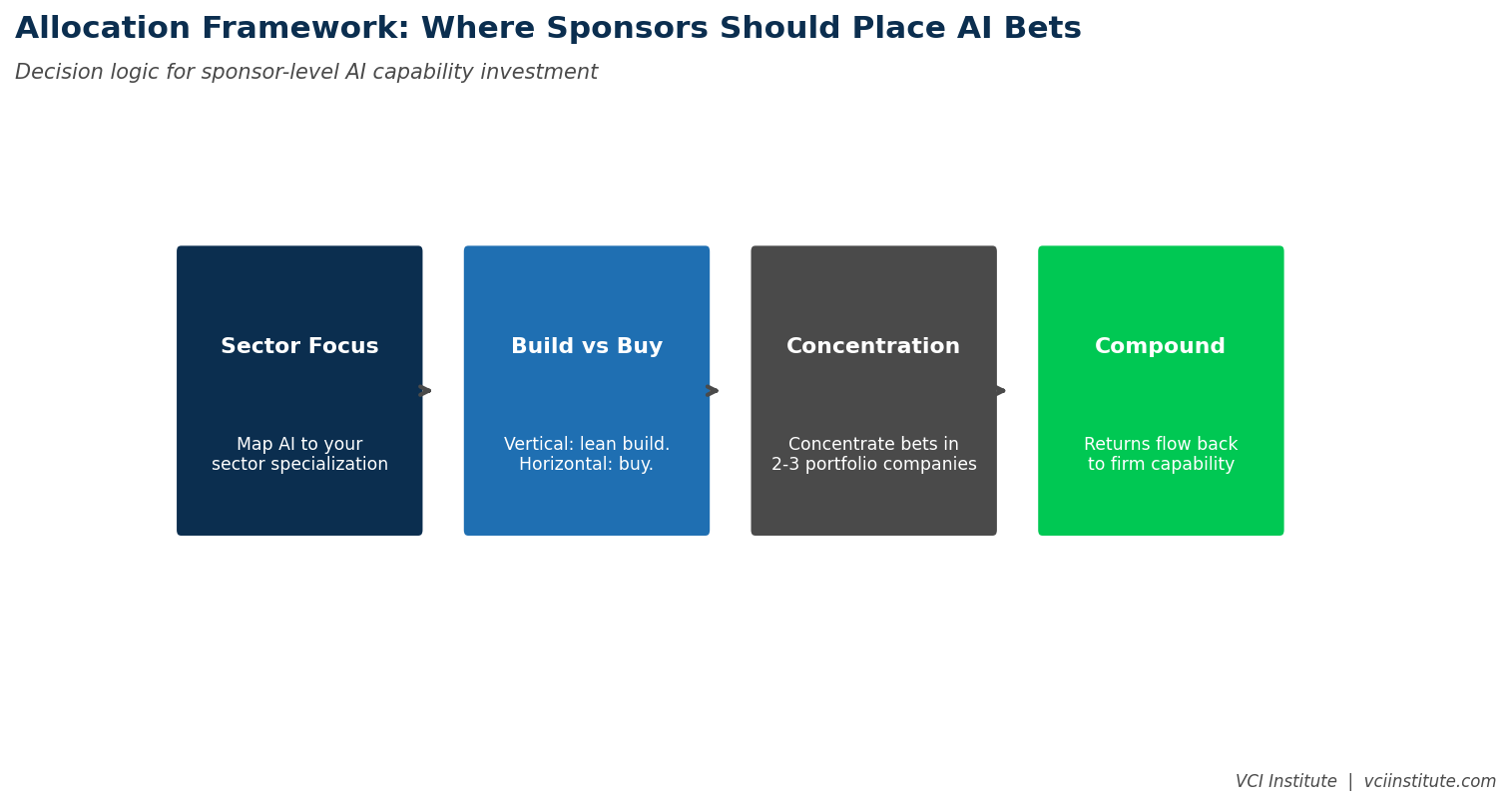

A useful heuristic for sponsors approaching the allocation question is to ask three sorting questions about any AI investment proposal.

What financial line does this affect, and by how much. If the answer is a top three line on the P&L or a top three input on cost, the investment is potentially vertical and worth deeper exploration. If the answer is a diffuse set of small cost reductions across many functions, the investment is horizontal and should be evaluated against the standard productivity hurdle.

How defensible is the benefit over time. If the benefit erodes as competitors deploy similar tools, the investment is horizontal and should be sized accordingly. If the benefit compounds because of domain specificity or data accumulation, the investment is vertical and warrants longer deployment timelines and larger budgets.

What does failure look like. Horizontal AI tools that fail to produce expected productivity gains are usually recoverable. They cost money but rarely break the value creation thesis. Vertical AI investments that fail can be more disruptive, because they often involve operational change in core processes. The risk profile is different and should be evaluated explicitly.

The Portfolio Lens

At the portfolio level, sponsors should aim for a deliberate mix. Most portfolio companies should have horizontal AI investments in the three productivity domains where the bridge clears cleanly. Some portfolio companies, those where the business model has a clear vertical use case in pricing, operations, or customer intelligence, should have vertical AI investments that are properly funded and timeline appropriate.

The portfolios that get this right are the ones where the sponsor team has consciously categorized each AI investment as horizontal or vertical, sized each according to the bridge it can credibly support, and resourced each according to the deployment complexity it involves. The portfolios that get this wrong are the ones where every portfolio company is funding the same horizontal tools to varying degrees of success, and a few portfolio companies that should have been funded for vertical investments are not, because the operating partner did not distinguish between the two.

The Right Question for the IC

The next time the IC discusses an AI investment, the right question is not whether to fund it. The right question is whether it is horizontal or vertical, and whether the size, timeline, and resourcing match what that category requires. Horizontal investments at vertical timelines are usually overengineered. Vertical investments at horizontal budgets are usually underfunded. Both patterns waste capital, in different ways, and both are common.

Sponsors who develop the discipline to make this distinction early will, by exit, have AI portfolios that produced step changes in core economics. Sponsors who treat AI as a single category will have spent comparable amounts and produced more diffuse, less defensible improvements. The difference is not in the technology. The difference is in how the allocation decision was framed at the moment the capital was committed.

About the VCI Institute

The VCI Institute is a nonprofit dedicated to building practical capability and shared standards for value creation in private equity. The Institute publishes operator-grade frameworks, runs training programs for emerging operating partners and CFOs, and operates a value creation simulator at vci.institute/simulator that lets sponsors and management teams stress test their value creation plans before committing capital. To learn more, visit vciinstitute.com.

© 2026 VCI Institute. All rights reserved. No part of this article may be reproduced or transmitted in any form without prior written permission of the VCI Institute.

We have many great affordable courses waiting for you!

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.